Proponents of the UI extensions argue that they provide valuable assistance to individuals struggling to find work in a weakened labor market. This allows the unemployed to maintain their consumption, supporters say, which also helps boost the economy. But critics of the large extensions argue that UI provides a disincentive to look for work until the benefits expire, prolonging unemployment spells.

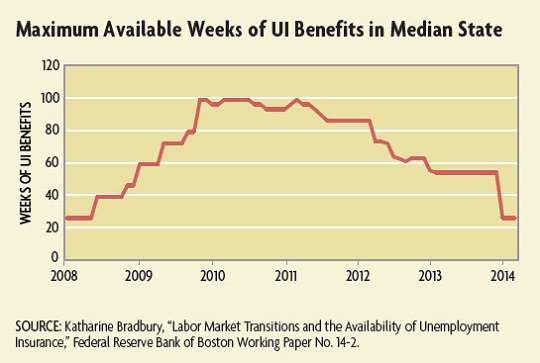

The emergency benefits expired on Dec. 28, 2013, returning the maximum duration for benefits to 26 weeks in most states. (North Carolina cut its benefits six months earlier; see "Moral Hazard and Measurement Hazard.") Lawmakers who favored the expiration say that labor market conditions have improved five years after the official end of the recession and that eliminating emergency benefits will improve conditions further by prompting more job seekers to find work. They point to the drop in unemployment from 6.7 percent to 6.1 percent in the seven months since the program expired as evidence of this improvement. But others in Congress want to reinstate the emergency benefits, arguing that labor market conditions are still weak and the falling unemployment rate reflects job seekers giving up rather than finding work; job seekers still need the additional help, they say.

Most economists agree that UI extensions contribute to longer unemployment spells, but the magnitude and importance of that effect are debated. Empirical evidence from the Great Recession suggests that the extended UI benefits had a small impact on unemployment duration, but there are other factors to consider as well when evaluating the program.

Insurance and Incentives

Searching for a job while unemployed is costly. Without access to income, job searchers must rely on accumulated savings or borrow to cover expenses while they find a new job. Research has shown that the average household in the United States does not have enough saved to weather prolonged joblessness. This means that laid-off workers might be forced to drastically reduce consumption, increase debt, or take the first job for which they qualify — even if they are overqualified. The latter is inefficient, resulting in lost productivity. UI benefits ease these constraints, allowing recipients to search longer and find a better-fitting replacement job. Labor economists call this the "liquidity effect," and to the extent it drives the longer unemployment spells associated with UI, it's not a bad thing.

"If what we see is just the liquidity effect, it means that we’ve helped job seekers better optimize their own welfare and society's welfare," says Jesse Rothstein, an economist at the University of California, Berkeley.

Like all insurance programs, however, UI runs the risk of encouraging the thing it is insuring against: unemployment. Because UI protects recipients from a portion of their wage losses, they may have less incentive to search for a replacement job until those benefits expire. Under this "moral hazard" interpretation, UI extends the duration of unemployment spells not because recipients are benefiting from reduced liquidity constraints to find a better job match, but because they are essentially "milking the system" before beginning their job search in earnest.

How do economists distinguish between these two effects? One way is to survey how UI recipients actually spend their time. In a 2010 Journal of Public Economics article, Princeton University economist Alan Krueger and Columbia University economist Andreas Mueller looked at data from the American Time Use Survey, which asks participants to keep a journal of how they spend their time each day. Krueger and Mueller found that UI recipients significantly increased job search efforts as their benefits approached expiration, while job seekers who were ineligible for UI benefits exhibited no such spike.

While such evidence points to moral hazard, there is also evidence that supports the liquidity effect as a driving factor of extended unemployment duration. Economists have compared UI to unemployment programs that do not suffer from moral hazard risk, such as lump-sum severance payments. Since severance payments provide cash up front, there is no incentive for recipients to extend their unemployment duration. In a 2007 Quarterly Journal of Economics article, David Card of the University of California, Berkeley, Raj Chetty of Harvard University, and Andrea Weber of the University of Mannheim found that UI and severance payments in Austria extended unemployment duration by similar amounts. This suggests most UI recipients are not motivated to abuse the system.

"From that evidence, one can conclude that it's generally beneficial to provide relatively generous unemployment insurance," says Mueller.

It's possible that different effects dominate depending on economic conditions, however. During recessions, when the labor market is weak, UI recipients may not have the ability to pick and choose among job offers, and the moral hazard effect may consequently be much less pronounced. In a 2011 paper, Johannes Schmieder of Boston University, Till von Wachter of the University of California, Los Angeles, and Stefan Bender of the Institute for Employment Research looked at data from Germany over a 20-year period to see if the effects of UI varied across the business cycle. They found very little difference in UI's effect on unemployment duration across the cycle, though disincentive effects were slightly smaller during downturns.

But even if the effects of UI on unemployment duration were entirely driven by moral hazard, the overall effect may not be very large. Rothstein looked at data from the Great Recession and found that UI extensions raised the unemployment rate by at most half a percentage point in early 2011. Several other studies have found similar or smaller effects.

"Even if none of what we observe is driven by the liquidity effect, the moral hazard is still much smaller than what we previously thought," says Rothstein.

Macroeconomic and Long-Term Effects

Proponents of expanding UI benefits during economic downturns also argue that it helps the broader economy, not just individual recipients. To the extent that recipients are liquidity-constrained, increasing benefits allows them to smooth consumption. In addition to making recipients better off, proponents argue this elevates consumption levels for the overall economy. In a key study from 1994, MIT economist Jonathan Gruber found that UI benefits helped recipients in the United States maintain consumption close to their pre-unemployed level. Without the benefits, recipients' consumption would have fallen by 22 percent, three times more than it did.

But just as UI affects individual incentives, it can also shape the incentives of employers to create jobs, which can have a negative effect on the broader economy. UI eases the liquidity constraints of job seekers and allows them greater ability to hold out for higher-paying jobs. All else equal, that pushes up the average threshold wage that would persuade a worker to take a job. Since the marginal profit from hiring is reduced, employers may post fewer vacancies.

Mueller says that macro effects like these are very difficult to assess empirically, but it is important to keep them in mind when determining how much — and for how long — to expand UI benefits. "The disincentive effects from UI are not that large," he says. "But it is important to scale benefits down at some point because of the possibility that providing high benefits for a very long time changes cultural norms such that people begin to rely more on the program. If that were to happen, the disincentive effects might become larger than what we measure now."

Indeed, there is some evidence that keeping expanded benefits in place for too long can change job seeker behavior over time. Thomas Lemieux of the University of British Columbia and W. Bentley MacLeod of the University of Southern California, Los Angeles, studied the effects of a major expansion in UI generosity implemented in Canada in 1971. The Canadian government reduced the duration of previous work required to qualify for the program from 30 weeks in a two-year period to eight weeks in a single year, and it increased the benefit duration and generosity sharply. Lemieux and MacLeod hypothesized that workers would gradually become aware of the more generous benefits as they were exposed to the program through involuntary unemployment, and over time this would change their incentives to supply labor. From 1972 to 1992, unemployment and UI use trended upward, and the authors found evidence that first-time UI recipients were more likely to use the system again throughout their lifetime.

Evaluating UI

Determining the desirability of UI as a social insurance program involves a number of considerations. As with any insurance program, the possibility of misuse is real. But many labor economists argue that UI does a reasonable job of minimizing moral hazard.

"In order to be eligible for UI, you must have an established job history," says San Francisco Fed labor economist Robert Valletta. In most states, eligibility for UI is determined based on employment and wages during a 12-month period preceding unemployment. "So, these are people coming from a career who are just trying to stay afloat during a difficult period of dislocation."

Valletta and Rothstein also argue that UI serves a unique welfare function. In a 2014 working paper, they explored whether households are able to supplement their income from UI using other safety net programs once their eligibility for UI benefits expire. They found that in both the 2001 and the 2007-2009 recessions, once UI benefits were exhausted, family incomes fell significantly and the share of families below the poverty line nearly doubled.

In the end, evaluating UI may depend on how one views its intended purpose. If UI is seen more as a program of social insurance designed to keep middle-class families out of poverty, then it seems to be largely a success. As a program of economic stabilization, the evidence is mixed, especially when one considers the potential long-run costs of expanding benefits for extended periods. It's also not clear that UI is the best program to deal with every unemployment spell. Ultimately, societies must weigh the negative effects of UI against the benefits when considering changes to the program.

Readings

Bradbury, Katharine. "Labor Market Transitions and the Availability of Unemployment Insurance." Federal Reserve Bank of Boston Working Paper No. 14-2, July 9, 2014.

Card, David, Raj Chetty, and Andrea Weber. "Cash-on-Hand and Competing Models of Intertemporal Behavior: New Evidence from the Labor Market." Quarterly Journal of Economics, November 2007, vol. 122, no. 4, pp. 1511-1560.

Fujita, Shigeru. "Economic Effects of the Unemployment Insurance Benefit." Federal Reserve Bank of Philadelphia Business Review, Fourth Quarter 2010.

Gruber, Jonathan. "The Consumption Smoothing Benefits of Unemployment Insurance." National Bureau of Economic Research Working Paper No. 4750, May 1994.

Krueger, Alan B., and Andreas Mueller. "Job Search and Unemployment Insurance: New Evidence from Time Use Data." Journal of Public Economics, vol. 94, no. 3-4, April 2010, pp. 298-307. (Working paper version available online.)

Lemieux, Thomas, and W. Bentley MacLeod. "Supply Side Hysteresis: The Case of the Canadian Unemployment Insurance System." Journal of Public Economics, October 2000, vol. 78, no. 1-2, pp. 139-170.

Rothstein, Jesse. "Unemployment Insurance and Job Search in the Great Recession." Brookings Papers on Economic Activity, Fall 2011.

Rothstein, Jesse, and Robert G. Valletta. "Scraping By: Income and Program Participation After the Loss of Extended Unemployment Benefits." Federal Reserve Bank of San Francisco Working Paper No. 2014-06, February 2014.

Schmieder, Johannes F., Till von Wachter, and Stefan Bender. “The Effects of Extended Unemployment Insurance Over the Business Cycle: Evidence from Regression Discontinuity Estimates Over 20 Years.” Quarterly Journal of Economics, vol. 127, no. 2, April 2012, pp. 701-752. (Working paper version available online.)

Stone, Chad and William Chen. “Introduction to Unemployment Insurance.” Center on Budget and Policy Priorities Report, July 30, 2014.

Whittaker, Julie M., and Katelin P. Isaacs. “Unemployment Insurance: Programs and Benefits.” Congressional Research Service Report, Feb. 12, 2014.