Portfolios Across the U.S. Wealth Distribution

In this article, we examine how household portfolios vary with wealth, age and race. Households in the middle of the wealth distribution hold most of their wealth as real estate, while wealthier households are more heavily invested in stocks and private business equity. As households age, they repay education loans and other debt and accumulate real estate and (to a lesser extent) financial assets. We find that Black households hold considerably less home equity, stocks and business equity. This can be explained (statistically) by lower levels of total wealth and by differences in age and household composition.

The net worth of a household is the difference between the value of its assets (such as bank accounts and homes) and the value of its debts (such as credit card debt and mortgages). Together, these items make up the household's wealth "portfolio."

The composition of a household's portfolio can matter greatly for wealth accumulation. To see this, consider the following two households:

- Household A holds a portfolio of safe assets (such as bank accounts) that earn a guaranteed return of 2 percent a year.

- Household B holds a portfolio of risky assets (such as stocks) with returns that average 4 percent a year but vary and are even sometimes negative.

If household A begins with $1,000 and reinvests all its returns, it would have $1,811 after 30 years. If Household B earns the average return every year, it would have $3,243 after 30 years, almost 80 percent more. However, the variability in returns means it could end up with considerably less or even more.

In this article, we show that the composition of household portfolios varies widely across the wealth distribution. While households in the middle of the wealth distribution tend to hold most of their wealth in the form of physical assets (such as real estate or vehicles), households at the top are more heavily invested in stocks and, especially at the very top, private businesses.

Household wealth, in turn, varies with several factors, including age and race. Younger households tend to accumulate housing while also holding mortgages and other sorts of loans. As they age, they pay down their debt and accumulate financial wealth. While both the wealth and life-cycle dimensions of household portfolios are well-known,1 the racial dimensions of portfolio allocation are less studied. We find that the tendency of Black households to hold considerably less home equity, stocks and business equity can be explained (statistically) in large part by their lower levels of total wealth and by racial differences in age and household composition.

Portfolio Composition Across Wealth Groups

Table 1 describes the U.S. household wealth distribution in 2022, using data from the Survey of Consumer Finances (SCF).2 At the bottom, the 10th percentile of the wealth distribution is $1 (in 2022 dollars), meaning that one in 10 households had virtually no wealth. In the middle, median household wealth is $162,350. The top 10 percent of households had $1,559,240 or more in wealth, and the top 1 percent had at least $11,640,000.

| Table 1: Household Wealth Distribution US 2022 |

|

|---|---|

| Percentiles | Net Worth (in 2022 Dollars) |

| 10 | $1 |

| 25 | $20,856 |

| 50 | $162,350 |

| 75 | $553,100 |

| 90 | $1,559,240 |

| 99 | $11,640,000 |

| Source: Survey of Consumer Finances. | |

To better understand how household portfolios vary with wealth, we group households into four percentile bins:

- Those between the 25th and 50th percentiles

- Those between the 50th and 75th percentiles

- Those between the 75th and 99th percentiles

- The top 1 percent

We then find portfolio shares for different groups of assets and debts, household by household. These shares are expressed as fractions of net worth, with debts expressed as negative shares.3 Figure 1 shows average portfolio shares for each bin.

Perhaps the most striking feature of household portfolios is the prominence of real estate. Between the 25th and 99th percentiles, housing is by far the largest component of assets, and mortgages are by far the largest component of debt. In the top quarter of the distribution, business equity and stocks become important, but only at the very top do they outweigh real estate.

In contrast, households between the 25th and 50th percentiles are much more heavily invested in vehicles and cash than households in other percentiles are. Much of this real estate is leveraged. Between the 25th and 50th percentiles, the average mortgage share equals over 60 percent of the average real estate share (93 percent/152 percent). As we move to higher wealth bins, this pseudo-loan-to-value ratio falls, in succession, to 35 percent, 23 percent and 12 percent as households deleverage. Richer households also hold smaller proportions of education debt.

In sum, Figure 1 shows that richer households are more heavily invested in higher-yielding assets (such as stocks and private equity), are less invested in low-yielding assets (such as cash and vehicles) and are less indebted. This suggests a "rich-get-richer" dynamic, where high-wealth households receive higher returns on their wealth portfolios, making it easier to maintain their relative standing.

The interpretation of this dynamic is less obvious. It may merely be that being wealthy enhances returns, as it allows households to hire better financial advisors or possess the resources needed to participate in certain types of lucrative investments.

On the other hand, selection dynamics may be in play. It may be the case that earning high returns from certain investments (such as entrepreneurship) is what allows some households to become rich.4 Both explanations generate a positive correlation between wealth and rates of return, and distinguishing them is beyond the scope of this article.

Portfolio Composition by Age

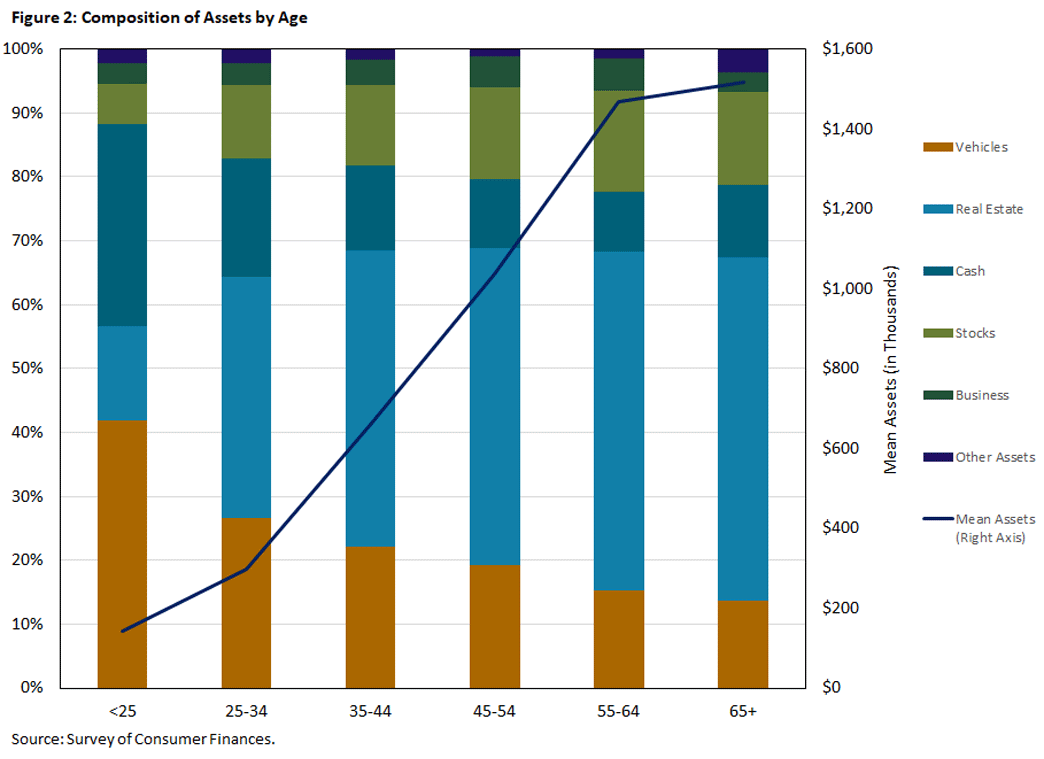

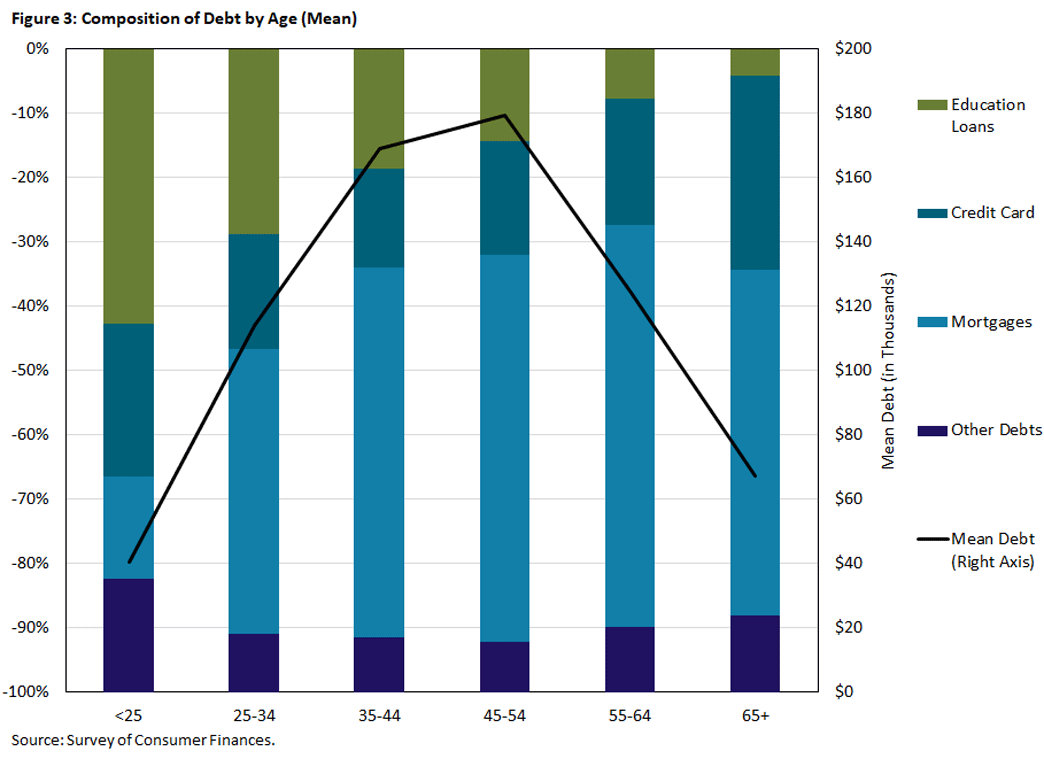

Because people accumulate wealth as they age, wealth-related portfolio variation is at least in part age-related variation. Figures 2 and 3 show how asset and debt portfolios, respectively, evolve over the life cycle. In contrast to Figure 1, asset shares are expressed as fractions of total assets, and debt shares as fractions of total debt. The graphs also plot mean assets and debt as lines; comparing these lines provides a measure of relative indebtedness and net worth.

Figure 2 shows that the youngest households (younger than 25) have relatively small amounts of assets, with nearly three-quarters invested in cash and vehicles. As they age, households accumulate real estate and (to a lesser extent) stocks, increasing both total assets and the shares held as real estate and stocks. The share of assets held as business equity also increases with age. Nonetheless, the stock share rarely exceeds 15 percent, and the business share never exceeds 5 percent, both lower than the corresponding shares for the top wealth quartile (as seen in Figure 1).

Figure 3 shows that among the youngest households — many of whom were recently in college — education loans make up the largest share of their debt. As they proceed from their 20s through their 40s, households take on mortgage debt as they become homeowners. Indebtedness rises sharply, from around $41,000 to over $179,000. Even as households pay down their debts later in life, mortgages remain their principal liability. They also carry significant credit card debt throughout the life cycle: Among retirees, nearly a third of debt consists of credit card balances.

Taken together, Figures 2 and 3 document that households begin the life cycle with cash and vehicles as their primary assets and education loans as their largest liability. They quickly switch to accumulating real estate, taking on mortgage debt to do so. These items will dominate their wealth portfolios for the remainder of their lives. As they age, households will continue to accumulate wealth, acquiring real and financial assets and paying down their debt. Although older portfolios contain substantial quantities of stocks and business equity, real estate still dominates. Only the richest households (on average) invest more heavily in other sorts of assets.

Does Race Play a Role?

It is well known that Black households hold much less wealth than White households.5 It is also well known that Black households are less likely to own their own homes or to hold stocks and private business equity, leading them to earn lower returns on their wealth.6

| Table 2: Mean Portfolio Shares by Percentile Bin and Race | ||||||||

|---|---|---|---|---|---|---|---|---|

| Net Worth Percentile Bin | 25th-50th | 50th-75th | 75th-99th | Top 1% | ||||

| Race | White | Black | White | Black | White | Black | White | Black |

| Assets | ||||||||

| Real Estate | 155% | 151% | 100% | 103% | 59% | 72% | 23% | 36% |

| Vehicles | 29% | 27% | 9% | 9% | 4% | 6% | 1% | 2% |

| Stocks | 13% | 17% | 16% | 9% | 31% | 19% | 31% | 31% |

| Cash | 15% | 11% | 8% | 5% | 6% | 6% | 2% | 2% |

| Business | 2% | 3% | 3% | 8% | 9% | 14% | 41% | 28% |

| Other Assets | 2% | 1% | 3% | 3% | 5% | 2% | 5% | 6% |

| Debts | ||||||||

| Mortgages | -96% | -80% | -35% | -30% | -13% | -15% | -3% | -2% |

| Credit Cards | -4% | -5% | -1% | -1% | 0% | -1% | 0% | 0% |

| Education Loans | -12% | -17% | -2% | -5% | -1% | -3% | 0% | 0% |

| Other Debt | -4% | -8% | -1% | -1% | 0% | 0% | -1% | -3% |

| Mean Net Worth (in Thousands) | $86 | $82 | $326 | $318 | $2,070 | $1,210 | $33,600 | $34,100 |

| Source: Survey of Consumer Finances. | ||||||||

How might these facts relate to each other? Table 2 contrasts the portfolio allocations of Black and White households within each net worth percentile bin. To confirm that both groups of households are holding similar amounts of assets, the bottom row of Table 2 shows mean wealth. Within each bin, except the top 1 percent, Black households hold fewer assets. The differences are relatively modest except for the top quartile. Within any given wealth bin, Black and White households hold relatively similar portfolios. The most notable difference lies in the top 1 percent, where the total portfolio shares of business equity and real estate are 13 percentage points higher and 13 percentage points lower, respectively, for White households.

In Table 2, we sort households solely by race and wealth, with no other controls. To measure the effect of race after accounting for covariates such as age or household composition, we estimate a series of regressions (using pooled data from all waves of the SCF between 1989 and 2019) where we express portfolio shares as a function of all these variables and an indicator of whether the household head is White. Table 3 shows the coefficient on the race (White) indicator for each portfolio item.

| Table 3: Estimated Race Coefficients from Portfolio Share Regressions | ||||

|---|---|---|---|---|

| Race (White) Indicator | Regression R2 | |||

| Standard | No Race | Race | ||

| Portfolio Item | Coefficient | Error | Indicators | Indicator |

| Vehicles | 0.272 | 0.035 | 0.5628 | 0.5696 |

| Real Estate | 0.238 | 0.042 | 0.2254 | 0.2285 |

| Cash | 0.007 | 0.029 | 0.9999 | 0.9999 |

| Stocks | 0.138 | 0.036 | 0.9999 | 0.9999 |

| Business | 0.082 | 0.093 | 0.1829 | 0.1829 |

| Bonds | 0.403 | 0.196 | 0.0476 | 0.0485 |

| Other Safe Assets | 0.261 | 0.082 | 0.0389 | 0.0396 |

| Education Loans | -0.088 | 0.038 | 0.4824 | 0.4830 |

| Credit Cards | 0.379 | 0.054 | 0.3577 | 0.3651 |

| Mortgages | 0.332 | 0.059 | 0.2247 | 0.2289 |

| Vehicle Debt | 0.163 | 0.056 | 0.3021 | 0.3034 |

| Other Debts | 0.401 | 0.066 | 0.9999 | 0.9999 |

| Source: Survey of Consumer Finances. | ||||

With one exception, White households hold more assets and less debt than Black households with the same covariates. (Because we express debt shares as negative values, a positive coefficient implies less debt.) The exception is education loans, where White households are more indebted.7 However, race explains very little of the variation in portfolio shares. The last two columns of Table 3 report the R2 (a measure of predictive power lying between 0 and 1) for portfolio regressions with and without the race indicator. Once other variables are controlled for, race provides relatively little additional predictive power. This suggests that although race does play a role in portfolio allocation, its direct effects are small.

Tables 2 and 3 suggest that much of the variation in portfolio shares can be attributed to factors such as total wealth. Because Black households earn less and inherit less, even if all households held identical portfolios, historical differences in wealth will be slow to disappear.8

If it is also the case that, by virtue of portfolio composition, lower wealth implies lower rates of return, wealth inequality will be even more persistent.9 As Table 3 shows, Black households may well have more restricted access to the high-return investments that would allow them to become rich. It may also be the case that Black households earn lower returns than White households with the same portfolios.10 Tables 2 and 3 do suggest, however, that even if these forces were absent, other mechanisms would work to sustain the racial wealth gap.

Footnote 7 was later updated to reflect how the report's findings contrast with the authors' findings.

John Bailey Jones is a vice president and economist and Urvi Neelakantan is a senior policy economist in the Research Department of the Federal Reserve Bank of Richmond.

Useful references include the 2006 article "Household Finance" and the 2019 book chapter "Trends in Household Portfolio Composition."

The Federal Reserve Board maintains the SCF.

This is why we exclude households below the 25th percentile. Small values of net worth often reflect large offsetting asset and debt positions. When net worth is the denominator, small changes in either assets or debt can change net worth in ways that substantially alter portfolio shares, leaving these shares largely uninterpretable.

Papers studying how entrepreneurship drives the distribution of wealth include "The Importance of Entrepreneurship for Wealth Concentration and Mobility" and "Entrepreneurship, Frictions, and Wealth."

Descriptive reviews of the racial wealth gap that use the SCF include "Updating the Racial Wealth Gap (PDF)" and "A New Look at Racial Disparities Using a More Comprehensive Wealth Measure." In our article "A More Comprehensive Measure of the Black-White Wealth Gap," we note that fully characterizing the Black-White wealth gap is more difficult than it might appear and offer one approach to doing so.

See, for example, the 2022 working paper "Wealth of Two Nations: The U.S. Racial Wealth Gap, 1860-2020."

Our results are from a sample that includes both graduates and non-graduates. Among college graduates alone, the report "Black-White Disparity in Student Loan Debt More Than Triples After Graduation" finds that Black individuals are more indebted.

This result implicitly assumes that poorer households do not save at higher rates than richer ones. There are several reasons why this should be the case. For example, because Social Security benefits decline in lifetime earnings, higher-earning households will need to save more to maintain their standard of living when retired. The papers "The Decline of African-American and Hispanic Wealth Since the Great Recession" and "A New Look at Racial Disparities Using a More Comprehensive Wealth Measure" both show that Black households rely more heavily on Social Security. Another example is bequests, which tend to behave as luxury goods, suggesting that richer households save more to leave them. (See, for example, "Wealth Inequality and Intergenerational Links.")

Papers making these points include "Wealth of Two Nations: The U.S. Racial Wealth Gap, 1860-2020" and "The Dynamics of the Racial Wealth Gap."

In "Racial Disparities in Housing Returns (PDF)," the authors find that Black homeowners earn lower returns, primarily because they run a higher risk of capital losses due to distressed sales.

To cite this Economic Brief, please use the following format: Jones, John Bailey; and Neelakantan, Urvi. (November 2023) "Portfolios Across the U.S. Wealth Distribution." Federal Reserve Bank of Richmond Economic Brief, No. 23-39.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.