Spotting Cyber Risk Before It Strikes

Cyber incidents — once seen as a bank's IT problem — are now a threat to financial stability. A major cyber incident can knock out payment systems, disrupt lending, and shake confidence in the broader financial system. Yet bank supervisors and the industry still lack a standard measure of how vulnerable a bank is to a future incident.

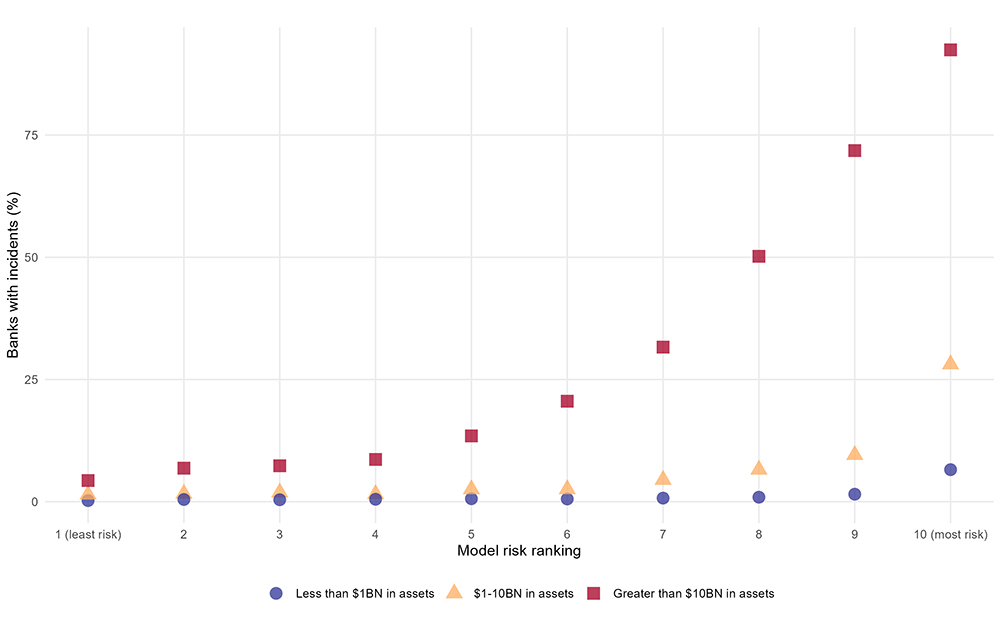

Our research aims to fill this gap to help both bank regulators and the industry. In our working paper, Cyber Risk in Banking: Measuring and Predicting Vulnerability, we develop the first cyber-risk forecasting framework that covers nearly all U.S. banks. The model combines cybersecurity signals, actual cyber incidents, and regulatory data to predict whether a bank will suffer a cyber incident in the next year. It works well for small, mid-sized, and large banks alike. The results can be used to improve supervisory oversight and internal risk management.

Three data sources, one bank-level picture

We analyze quarterly data from 2015 through 2024 that links three sources:

- BitSight derives cybersecurity ratings from the internet — from a wide range of technical data related to network security, configuration practices, and evidence of compromise;

- Zywave records realized cyber incidents, including malicious data breaches, phishing, fraudulent account access, and network disruptions; and

- FFIEC Call Reports have quarterly balance-sheet, income, and structural data for every regulated U.S. bank.

Our model addresses the question: Given a bank's size, balance sheet, and cybersecurity hygiene (its "security posture"), how likely is it to suffer a cyber incident in the next year?

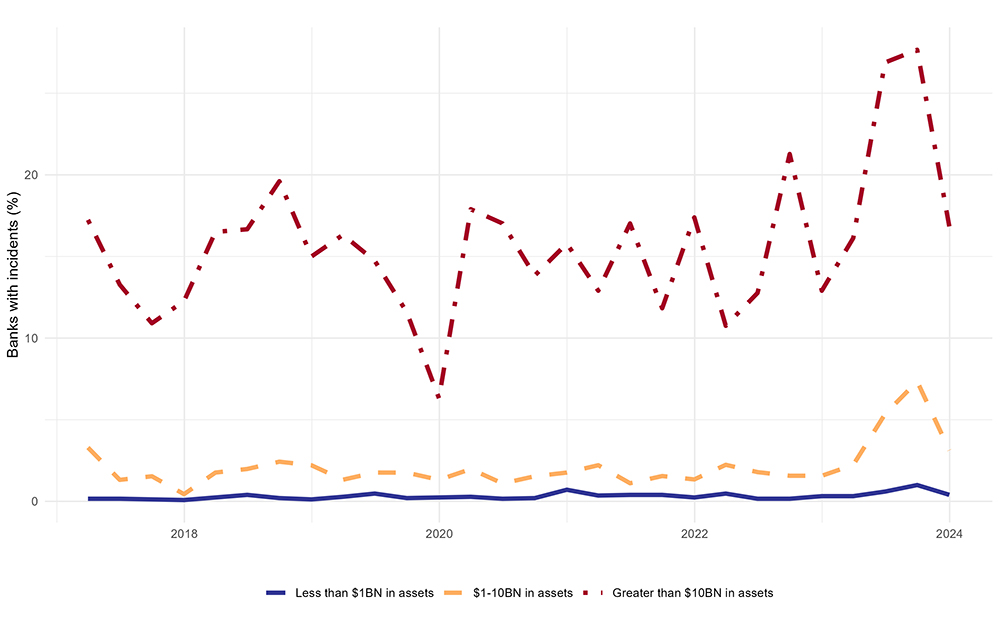

Cyber incidents are concentrated at the largest banks

How likely a bank is to experience a cyber incident depends on its size. Typically, 10-15% of large banks (with over $10 billion in assets) report at least one incident. In contrast, only around 2% of small banks (under $1 billion) report incidents. Mid-sized banks ($1–10 billion) report incidents at rates between those levels, but that fluctuate substantially across quarters. We can see these trends in Figure 1.

Contact Us