Bank Failures: Solvency and Liquidity

Economic Brief

April 2026, No. 26-12

Key Takeaways

- Bank failures are almost always preceded by weak fundamentals: bad loans, low capital and/or declining earnings. Meanwhile, depositor panics, while dramatic, are rarely the root cause.

- Low recovery rates on failed banks' assets and examiners' postmortem assessments both point to deep insolvency, even in banks that experienced runs before failing.

- Deposit insurance and emergency lending alone cannot prevent crises. Policies that ensure adequate bank capital and sound risk management are essential.

We often recall bank failures by their most salient moments: the runs on the bank that preceded the collapse. The reasons for runs can vary, from the "Twitter-fueled" run that preceded Silicon Valley Bank's failure in 2023 to the Washington Mutual bank run during the 2008 global financial crisis. But each time an episode occurs, it reignites the age-old debate about the role of runs in bank failures: Do banks fail because of the run or because their assets have already gone bad? In this article, we'll examine the causes of bank failures, how they relate to bank runs and what the implications are for policy.

Why Banks Fail

In theory, bank failures can arise from two distinct issues: liquidity and solvency. Under the liquidity view, a sudden wave of withdrawals can force a healthy bank to sell its assets at steep discounts to raise cash. This fire sale destroys value and could force this otherwise solvent bank to fail. In this view, the run itself is the cause of failure, as the bank would have survived absent the run.

Under the solvency view, a bank's loans and investments have gone bad due to increased default, falling security prices, excessive risk-taking by management or a combination of these issues. In this scenario, once bank assets are not worth enough to repay depositors, a run may be the natural and final trigger that forces the closure of the bank, but it is not the root cause of the problem.

This difference matters for policy. If runs are the main problem, deposit insurance and central bank emergency lending should suffice. If insolvency is the main problem, emphasis must shift to capital, supervision and risk management.

What History Shows

The empirical debate on whether bank failures are caused by insolvency or by lack of liquidity goes back at least to the 1963 book A Monetary History of the United States by economists Milton Friedman and Anna Schwartz. They argued in that work and others that many Great Depression-era failures resulted from "self-justifying" runs on solvent banks. For instance, Friedman famously contended in a 1980 program that the failure of the Bank of the United States in December 1930 — the largest bank failure in U.S. history at the time — was caused by a run that brought down a "perfectly good bank."1

Since then, a large body of research has debated this view. In 1976, Peter Temin argued that failures in the Great Depression were largely caused by falling income and asset prices, not by exogenous panics.2 Eugene White showed in 1984 that banks that failed during the 1930 crisis were less well capitalized, held more illiquid assets and relied more on wholesale funding than survivors.3 Elmus Wicker noted in 1996 that runs and failures during the 1932 Chicago banking panic were not spread indiscriminately and instead were concentrated in weak banks.4 And in 1997, Charles Calomiris and Joe Mason found that both solvent and insolvent banks experienced runs during the Chicago banking panic, but only the insolvent ones failed after the runs for the most part.5

These findings extend beyond the Great Depression. Research on the savings and loan crisis in the 1980s, the 2008 global financial crisis and the 2023 bank failures all find the same pattern: Banks that fail are highly leveraged, have low earnings and hold risky asset portfolios. The banks that failed in March 2023 had suffered large unrealized losses on long-term securities, pushing them toward insolvency.

In our 2026 paper "Failing Banks," we extend these findings across 160 years of U.S. banking data, covering over 5,000 bank failures. Failing banks consistently exhibit declining capital, rising asset losses and growing reliance on expensive wholesale funding years before failure. This holds across institutional regimes and with and without deposit insurance or a public lender of last resort. Bank failures are also substantially predictable out of sample using balance-sheet data alone. Banking crises, then, are largely the predictable consequence of poor fundamentals building up over time.

Moreover, we find that a recurring precursor to failure is rapid asset growth, usually via aggressive lending. Most of the largest bank failures in U.S. history — including the Bank of the United States in 1930, Continental Illinois in 1984 and Washington Mutual in 2008 — followed periods of rapid (arguably reckless) expansion. Similarly, Silicon Valley Bank tripled in size between 2019 and 2021.6 At the aggregate level, credit booms are also strong predictors of banking crises internationally.7

Recovery Rates and Examiner Assessments

The evidence above links bank failures to weak fundamentals, but it does not fully settle whether most failures reflect runs on weak-but-solvent banks or on banks that were genuinely insolvent. Two additional sources of evidence bear on this question.

First, recovery rates on failed banks' assets fell well short of creditor claims, as we found in our "Failing Banks" paper. In our data on pre-Federal Deposit Insurance Corp. (FDIC) receiverships — the formal process used to wind down failed national banks — creditors recovered on average only 75 cents on the dollar. Banks that experienced large deposit outflows before failure had even lower recoveries (about 72 cents), consistent with runs occurring at the weakest banks. At the time, receivers were known to liquidate bank assets in an orderly fashion over several years, and the Office of the Comptroller of the Currency (OCC) actively avoided fire sales. Thus, these results suggest that — barring strong assumptions on the value destruction of receiverships — assets at most failed banks were genuinely impaired, and runs on weak-but-solvent banks accounted for only a modest share of national bank failures.

Second, our research found that contemporary bank examiners reached the same conclusion. OCC examiners assessed bank assets at failure, and, on average, only 36 percent of those were classified as "good," with 47 percent considered "doubtful" and 18 percent deemed "worthless." Moreover, in the OCC's bank-specific cause-of-failure reports through 1928, runs and liquidity issues were cited in fewer than 20 out of over 2,000 cases. The most common causes were poor local economic conditions, asset losses and fraud.8 As a 1936 Federal Reserve report put it plainly, "In our long, failure-studded history of banking most of the institutions which suspended business were subsequently proved to be insolvent."9

Why Strong Banks Usually Survive Runs

If runs can hit both weak and strong banks, why don't they always cause solvent banks to fail? The evidence points to several mechanisms that allow healthy banks to survive.

Interbank lending is one. Other banks — possibly better informed about a peer's true condition — could lend to solvent institutions facing withdrawal pressure. Further, during the National Banking Era, clearinghouses acted as quasi-central banks, issuing loan certificates to provide liquidity. Evidence from the German Crisis of 1931 and the 2008 U.S. federal funds market confirms that interbank participants can often distinguish weak from strong banks and lend accordingly.10

Capital injections — as well as large deposits into the bank made by shareholders — were also common ways for bank insiders to credibly show confidence in their bank. Temporary suspensions were also used, both to cool panics and to allow examiners to audit the books. Partial suspensions were also frequent during runs. These relied on clauses in time deposits that allowed banks to suspend withdrawals for up to 60 days in case of a run.

Depositor behavior also matters. Evidence from the Great Depression, India and the 2023 U.S. banking crisis consistently shows that informed depositors can distinguish between distressed and healthy banks.11

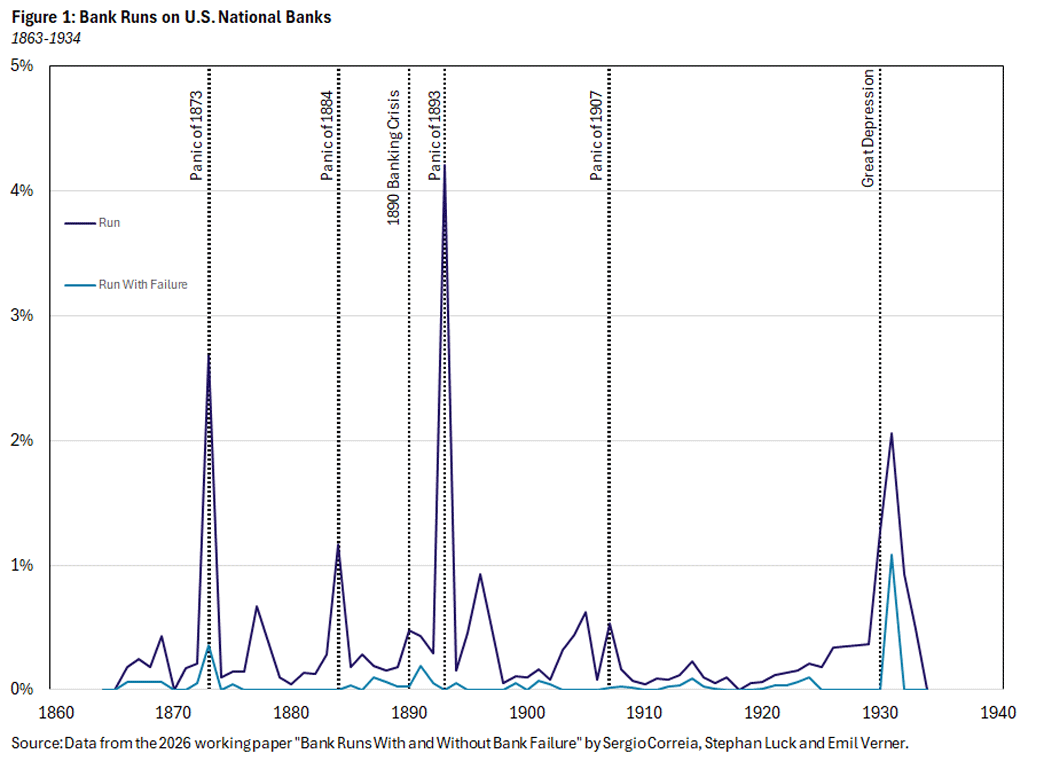

Still, more work is warranted. Empirical evidence on the causes and consequences of runs is limited to a few bank run episodes or to aggregate analysis. In our 2026 working paper "Bank Runs With and Without Bank Failure," we use narrative evidence from historical newspapers to collect a systematic dataset of thousands of U.S. bank runs. As shown in Figure 1, most runs do not lead to failure, particularly of strong, well-capitalized banks.

Policy Implications

The finding that most bank failures stem from insolvency has implications for how we think about financial stability policy.

Deposit insurance — introduced with the creation of the FDIC in 1933 — sharply reduced run-driven failures. It also changed how banks fail: Under deposit insurance, insured deposits can flow toward weak banks, enabling risk-taking and delaying closures. As we document in our 2025 working paper "Supervising Failing Banks," modern bank failures are typically not so much market-driven events but supervisory decisions, with regulators having discretion on when to close troubled banks.

Lender-of-last-resort policies can also help solvent banks survive panics. A natural experiment during the Great Depression — comparing the Atlanta Fed's generous lending with the St. Louis Fed's restrictive approach12 — shows that liquidity support can reduce suspensions.

But liquidity provision cannot fix insolvency. International evidence shows that "quiet crises," or banking distress without panics, can produce severe contractions in credit and output.13 Studies of targeted liquidity interventions find that they never resolved firm distress on their own, as balance-sheet restructuring was always required.14

If bank failures are ultimately about solvency, then a key safeguard is adequate capitalization. More equity means a larger cushion to absorb losses before insolvency, reducing both the likelihood of failure and the scope for runs to cause damage.

This does not mean, however, that deposit insurance and discount window lending are not essential for the modern banking sector. Bank runs can still be very damaging after all (particularly for weaker banks), and the possibility of runs might even lead banks to curtail credit preemptively, which in turn could limit economic growth. Neither policy, however, can work without adequate bank capitalization, well-structured supervision and the provision of timely and transparent information to the market.

Conclusion

Although many questions remain about how losses, funding stress and depositor behavior interact over time, the historical evidence clearly points in one direction: Bank failures usually begin with bad assets, weak earnings and not enough capital. Runs can speed up failures and could sometimes worsen the damage, but by the time depositors head for the exit, the deeper problem is usually already on the bank's balance sheet. Ensuring that banks hold adequate capital and that supervisors act on early signs of deterioration remains the most reliable way to prevent failures from occurring.

Sergio Correia is a senior economist in the Research Department at the Federal Reserve Bank of Richmond. Stephan Luck is a financial research advisor at the Federal Reserve Bank of New York. Emil Verner is the Lemelson Professor of Management and Financial Economics and professor of finance at MIT Sloan School of Management.

1

See the episode "Anatomy of a Crisis" from the 1980 TV series Free to Choose.

2

See Temin's 1973 paper "Did Monetary Forces Cause the Depression? (PDF)."

3

See White's 1984 paper "A Reinterpretation of the Banking Crisis of 1930."

4

See Wicker's 1996 book The Banking Panics of the Great Depression.

5

See Calomiris and Mason's 1997 paper "Contagion and Bank Failures During the Great Depression: The June 1932 Chicago Banking Panic."

6

See the April 2023 "Review of the Federal Reserve's Supervision and Regulation of Silicon Valley Bank" from the Federal Reserve Board of Governors.

7

See the 2012 paper "Credit Booms Gone Bust: Monetary Policy, Leverage Cycles and Financial Crises, 1870-2008" by Moritz Schularick and Alan Taylor.

8

The Great Depression may be a partial exception. Federal Reserve Board classifications of Depression-era suspensions suggest that liquidity issues played a larger role than in other periods. But even then, examiner assessments and recovery rates remained pessimistic about asset quality.

9

See the 1936 report "Bank Suspensions, 1892-1935" by the Federal Reserve Board of Governors.

10

See the 2024 paper "Who Can Tell Which Banks Will Fail?" by Kristian Blickle, Markus Brunnermeier and Stephan Luck and the 2011 paper "Stressed, Not Frozen: The Federal Funds Market in the Financial Crisis" by Gara Afonso, Anna Kovner and Antoinette Schoar.

11

See the 1996 paper "Contagious Bank Runs: Evidence From the 1929-1933 Period" by Anthony Saunders and Berry Wilson, the 2016 paper "A Tale of Two Runs: Depositor Responses to Bank Solvency Risk" by Rajkamal Iyer, Manju Puri and Nicholas Ryan, and the 2024 report "Tracing Bank Runs in Real Time" by Marco Ciprani, Thomas Eisenback and Anna Kovner.

12

See the 2009 paper "Monetary Intervention Mitigated Banking Panics During the Great Depression: Quasi-Experimental Evidence From a Federal Reserve District Border, 1929-1933" by Gary Richardson and William Troost.

13

See the 2020 paper "Banking Crises Without Panics" by Matthew Baron, Emil Verner and Wei Xiong.

14

See the 2025 paper "Ad Hoc Emergency Liquidity Programs in the 21st Century" by Steven Kelly, Vincient Arnold, Greg Feldberg and Andrew Metrick.

To cite this Economic Brief, please use the following format: Correia, Sergio; Luck, Stephan; and Verner, Emil. (April 2026) "Bank Failures: Solvency and Liquidity." Federal Reserve Bank of Richmond Economic Brief, No. 26-12.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us