Updating Results

Updating Results

Article

Third Quarter 2026

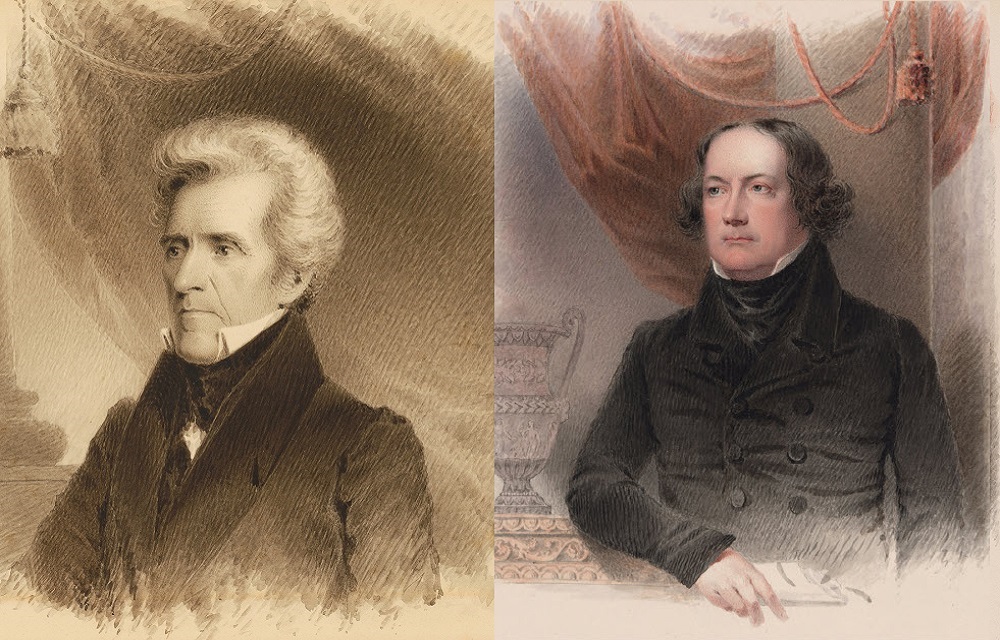

Before the First Bank of the United States, another, less well-known institution helped the fledgling United States find its financial footing.