What Is a Crypto Conglomerate Like FTX? Economics and Regulations

Economic Brief

March 2023, No. 23-09

We explain the economics behind the rise and fall of FTX. We view FTX and its associates as components making up one large entity: a crypto conglomerate. Understanding the economics of crypto conglomerates is crucial for designing effective regulations.

FTX, once among the world's biggest crypto exchanges, shook the world by filing for bankruptcy in November, leaving 1 million customers and other investors facing total losses in the billions. FTX offered its customers a wide range of crypto products to trade, including its own cryptocurrency FTT, and its affiliate Alameda Research traded many of these crypto products directly like a hedge fund. Each of these entities is an important player on its own:

- FTX was valued at $32 billion in 20221 and cleared on average $16 billion worth of customer trades every day.

- The market cap of FTT was about $3.5 billion before FTX's bankruptcy filing.

- The cryptocurrency exchange is said to owe its 50 largest creditors alone nearly $3.1 billion.

While cryptocurrencies and lending schemes have failed before, what makes this time different is that FTX — together with other affiliates under founder and CEO Sam Bankman-Fried (SBF)'s control — is a crypto conglomerate that connects these failures. In this article, we will discuss what a crypto conglomerate is, why they form and what issues are faced in regulating them.

What Is a Crypto Conglomerate?

According to the 2022 report "Regulation, Supervision and Oversight of Crypto-Asset Activities and Market" from the Financial Stability Board, "One prominent feature of the crypto-asset market structure is that service providers often engage in a wide range of functions. Some trading platforms, besides their primary functions as exchanges and intermediaries, also engage in … issuance distribution and promotion. Some trading platforms also conduct proprietary trading or allow proprietary trading on the platform by affiliated entities. By vertically integrating multiple functions, these service providers resemble a financial conglomerate."

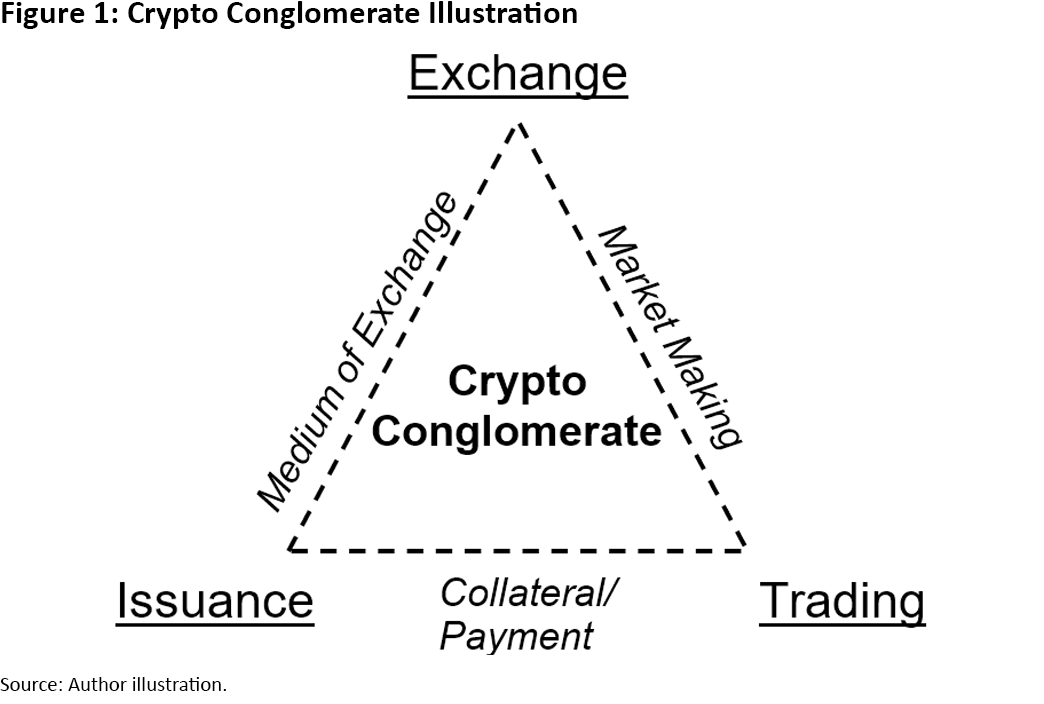

Thus, a crypto conglomerate consists of at least three arms:

- An exchange arm that provides a marketplace for users to buy and sell crypto assets and contracts.

- An issuance arm that maintains the supply of tokens via regular minting and burning.

- A trading arm that actively enters or exits positions on crypto products to maximize its return.

Applying our characterization, FTX is the exchange arm, FTT is the cryptocurrency of the issuance arm, and Alameda is the trading arm.

Some counterexamples could be useful to illustrate the concept of the crypto conglomerate. The New York Stock Exchange is an exchange arm but does not issue tokens or trade against clients. Indeed, traditional financial exchanges seldom issue anything like tokens.

A closer example of an issuance arm in non-financial sectors could be found in casinos. Casinos have an issuance arm (the cage) for selling and buying its chips. Suppose we interpret a casino as a marketplace that facilitates players to bet against each other, analog to a crypto exchange serving traders by allowing them to trade against each other. In that case, casinos might have an exchange arm in a loose sense. However, casinos do not bet as, say, a poker player against others (the trading arm).2 Bundling the three arms becomes plausible in the crypto world and is essential for a crypto conglomerate.

A crypto conglomerate can also spin out other arms. For example, the crypto conglomerate DCG has a lending arm via the subsidiary Genesis in addition to its exchange arm and its trading arm via the subsidiary Grayscale Investment. Other notable arms of crypto conglomerates include the custody and settlement of crypto assets.

Crypto Conglomerate's Economy of Scope

Not all crypto exchanges issue their own tokens, so why do some exchanges issue them, like FTX did with FTT? In other words, what is the exchange token's economy of scope?3

To explain the economics behind the bundling, our 2022 paper "Payments on Digital Platforms: Resiliency, Interoperability and Welfare" considers a situation where an exchange platform can issue tokens, charge commission fees for using the off-platform medium of exchange (e.g. credit card or cash), or both. We show that token issuance:

- Generates seigniorage revenue for the platform by selling tokens and collecting interest income of the associated reserve (for backed stablecoins)

- Serves as a medium of exchange (on its own or combined with USD fiat) that facilitates exchanges on the platform by relaxing users' liquidity constraints via trading fee discounts and rewards like airdrop and token buybacks (as we see in the design of FTT)

Serving as a medium of exchange also boosts the demand for tokens and, hence, the seigniorage revenue. In practice, part of the liquidity constraints relates to the fact that standard payment methods are not readily accessible in the crypto space due to regulatory and technical issues.4 Our paper also characterizes some essential features of the exchange's token schemes as floating coins and as stablecoins.

Additionally, the 2022 working paper "Platforms, Tokens and Interoperability" points out that an incumbent platform can generate a "lock-in" effect after issuing tokens: By increasing the redemption fee (the charge to users who convert tokens back to fiats), a platform can deter customer outflow and raise the costs (via higher rewards or lower fees) to competing platforms of stealing current users. These theories help explain why a crypto conglomerate wants to bundle the exchange and issuance arms.

What is the economy of scope behind bundling the exchange and trading arms? A compelling reason is that the trading arm would bring a lot of trading activities (and thus the associated fee revenue) to the exchange. But to attract traders to the exchange arm, market liquidity should be adequately maintained by the market makers so that traders can quickly and easily enter or exit positions without facing huge bid-ask spreads. The trading arm can fulfill the market-making role. These explain some economic benefits of bundling the exchange and trading arms.

What about bundling the trading and issuance arms? Unlike typical cryptocurrencies such as bitcoin or ether, the supply of exchange tokens is not limited exogenously by the protocol since the exchange mints these tokens.5 One might thus think the benefit of bundling the trading arm with the issuance arm is like giving a hedge fund a money-printing machine: It gives the trading arm an unlimited budget to pursue any trading strategy. While having this "elastic supply of money" may not hurt in nominal terms (especially to finance big transactions), issuing extra tokens will dilute the value of existing tokens in real terms.6

An alternative arrangement that doesn't dilute the token value is to pledge the exchange tokens as collateral for secured borrowing, as we have seen in some of Alameda's leverage strategies.7 On the other hand, the trading power of the trading arm can help boost and stabilize the value of the tokens. Indeed, this role of Alameda is made explicit in FTX's white paper. These help explain the economic benefit of bundling the trading and issuance arms.

Problems of Un(der)regulated Crypto Conglomerates

Traditional financial institutions also have incentives to expand and combine multiple functions. However, existing regulation segregates particular arms. For example, the New York Stock Exchange is not permitted to have any significant stake in broker-dealers (and vice versa) and cannot perform any proprietary trading against its clients.

However, applying existing regulations to crypto conglomerates is challenging and requires further updates and clarification. For example, regulatory oversight is made difficult as FTX was based in the Bahamas. (In fact, its competitor Binance does not even have any fixed physical presence.) Whether crypto assets are commodities or securities — which have different regulation perimeters — is still up for debate.8 On top of these generic issues about regulating crypto players, there are problems and risks associated with crypto conglomerates.

Excessive Leverage

In retrospect, Alameda was critical to FTX's eventual collapse. Without supervision, bundling with the exchange arm (in this case, FTX) and the issuance arm (FTX) facilitates excessive leverage of the trading arm (Alameda) via three main avenues:

- The exchange arm allows a negative balance of the trading arms without posting an appropriate level of collateral.9

- Tokens are injected into the trading arm for pledging as collateral.

- The trading arm manipulates the price of tokens — which is also the collateral posted by the trading arm — and allows further borrowing.

When the trading arm builds up excessive leverage, the risk of bankruptcy also increases (especially when the trading arm lacks risk management). Since the customers maintaining balances at the exchange are typically unsecured creditors, they are only repaid in case of bankruptcy after secured creditors and more senior credits. As a result, excessive leverage exposes the customers to the risk of hidden losses.

Interconnectedness Without Transparency

Crypto conglomerates are structured to operate mostly offshore and possibly in non-compliance with existing requirements on disclosure and auditing. Some institutional investors (like Sequoia Capital) have since said they were blindsided by FTX's implosion, partly because the interconnectedness between FTX and Alameda was not clearly disclosed. The lack of transparency on corporate structure and financial position, thus, can be a major factor.

Furthermore, the trading arm could take advantage of the insider information or other special treatment shared by the exchange arm to front-run its customers on the exchange platform.10 Specific to this episode, the nature of Alameda and FTX's relationship presented a potential conflict of interest. Isolating the risks of the trading arm to protect customers and investors is impossible without transparency on the crypto conglomerate.

Abuse of Rehypothecation

Rehypothecation happens when customer assets are used for trading. Federal regulators at the CFTC say FTX was leveraging customer assets — specifically, customers' cryptocurrency deposits — to lend to Alameda without informing the customers. In traditional finance, custody is required to have client assets available on demand. However, the crypto conglomerate often suspends withdrawals if customer assets are rehypothecated.

Fragility Due to Reliance on Self-Issued, Unbacked Tokens

FTX accepted its own unbacked tokens as collateral for margin loans made to clients on its platform, as well as loans made outside of its platform. Such practice creates extreme wrong-way risks. When the price of the exchange token falls, its collateral value also falls. It triggers margin calls, engenders liquidation of the trading arm's position, puts the crypto conglomerate under liquidity pressure and decreases the token price further. Indeed, a similar dynamic played out in May/June when crypto-asset lender Celsius held a considerable amount of its own unbacked token CEL, which subsequently crashed.

Other Issues

In addition to those above, a crypto conglomerate can create or amplify other problems. Examples include:

- Engaging in wash trading activities to manipulate the crypto market

- Misappropriation of client funds in the provision of custodial services

- Anti-competitive behavior increasing concentration risks

Conclusion

In this article, we revisit the economics behind crypto conglomerates and highlight the associated risks. One prevailing principle of financial regulation is "same activity, same regulation." However, such a principle tends to identify regulation by activities on their own and, hence, might ignore the amplification of risks that occurs when activities are bundled in a crypto conglomerate.

In addition, the interconnected between crypto conglomerates and the traditional financial sector — as seen in the fall of Silvergate Capital — may spread these amplified risks of crypto conglomerates on the macro level. Distinguishing these risks would be crucial in thinking about crypto regulations in the future.

Jonathan Chiu is a senior research advisor at the Bank of Canada, and Russell Wong is a senior economist in the Research Department at the Federal Reserve Bank of Richmond.

1

To compare with the traditional exchange, the market cap of the ICE group — which owns the New York Stock Exchange and other major exchanges — is about $57 billion. To compared with the traditional hedge fund, the assets under management of Citadel — the best performing hedge fund last year — is about $56 billion.

2

The house does play as the dealer, but it is more like serving players rather than playing against them.

3

Besides FTT, examples of bundling the exchange and issuance arms include Binance's BNB and Huobi's HT. We focus on centralized exchanges (CEX) that issue tokens. There are also tokens issued by decentralized exchanges like Uniswap and SushiSwap, which are not prone to the moral hazard issues of CEX we discuss here.

4

For example, Bankman-Fried defended against the allegation that FTX asked its customers to wire money to Alameda by saying that, early in its history, FTX had trouble opening bank accounts, but Alameda had such access.

5

Of course, the exchange can opt to burn tokens as well, as in the case of Binance's BNB.

6

For example, a $2.1 billion mix of FTT and BUSD had been deployed to buy back FTX's stake from Binance, which triggered a 10 percent fall in FTT's price within 24 hours after Binance had liquidated these FTT.

7

For example, Alameda Research secured its loans from Voyager and BlockFi with FTT tokens, as shown in its bankruptcy filings.

8

An asset is security if it is: (1) an investment of money, (2) in a common enterprise, (3) with the expectation of profit and (4) to be derived from the efforts of others. For example, bitcoin does not pass this test (called the Howey test) because Bitcoin is not an enterprise and is not reliant on others to increase its return. Recently, SEC Chair Gary Gensler expressed his view that, except for bitcoin, "at the core, these tokens are securities because there's a group in the middle and the public is anticipating profits based on that group."

9

The SEC alleges that an exception was programed into FTX's code that "allowed Alameda to maintain a negative balance in its account, untethered from any collateral requirements. No other customer account at FTX was permitted to maintain a negative balance."

10

If Alameda did not need to maintain positive balances at FTX as the SEC has alleged, it could see "several milliseconds" shaved off its trade execution times from the routine balance checking to shunt past other users, according to the CFTC.

To cite this Economic Brief, please use the following format: Chiu, Jonathan; and Wong, Russell. (March 2023) "What Is a Crypto Conglomerate Like FTX? Economics and Regulations" Federal Reserve Bank of Richmond Economic Brief, No. 23-09.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Bank of Canada, the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us