Bank Resolution and the Fed’s New Standing Repo Facility

Economic Brief

February 2022, No. 22-06

In July 2021, the Fed put a new lending program in place: the Standing Repo Facility. The program will likely impact the financial system in multiple ways. One specific area of influence is the process of resolution planning at large banking corporations. How the facility interacts with those plans will depend in part on guidance provided by regulators as resolution planning continues evolving.

For decades, the Federal Reserve has used repurchase agreements (or "repos") as a tool to implement monetary policy and, occasionally, to stabilize short-term funding markets. More recently, as perhaps a culmination of a process of incremental involvement, the Fed created two facilities: one to borrow and one to lend as needed in secured overnight money markets.

The implications from the availability of these facilities are far reaching. For example, they are likely to limit volatility in money market interest rates — as noted in Lorie Logan's 2021 speech "Monetary Policy Implementation: Adapting to a New Environment" — and they are a tool for the Fed to manage how the varying size of its balance sheet impacts the financial system.1

In this article, we discuss the impact that the new lending facility — the Standing Repo Facility (SRF) — may have on one aspect of financial stability: large bank resolution planning, or the plans for a rapid and orderly resolution of a global systemically important bank (G-SIB) in the event of failure.2

The introduction of the SRF implies wider availability of (possibly stigma-free) borrowing from the central bank. This can be particularly relevant if the failure of a large bank happens in times of generalized distress in the financial system, when the kind of liquidity needed for the resolution of a large bank is difficult to secure. This availability of credit can have ex ante and ex post implications on banks' and regulators' decisions and resolution plans.

The Fed's New Standing Repo Facility

Stress and volatility in repo markets can sometimes spillover to other short-term funding markets. In both September 2019 and March 2020, U.S. repo markets experienced several days of high volatility.

Partly in response to those events, the Fed put in place a new repo facility in July 2021 that serves as a backstop to the repo market. At the facility, a broad set of counterparties — including primary dealers and banks — can enter repo transactions with the Fed. These repo contracts are a way for the Fed to lend cash to primary dealers and banks overnight, backed by Treasury and agency securities.

The SRF is structured as an auction using a minimum bid rate equal to the top of the range of policy interest rates fixed by the Federal Open Market Committee. There is a maximum bid size for each participant and a total maximum amount that can be borrowed each day. Since these maximum auction amounts (individual and aggregate) are generally large, the expectation is that the facility will create a ceiling on repo market rates and, thus, reduce volatility. The ultimate goal is to smooth the transmission of interest rate policy to repo markets and beyond.3

Use of the Standing Repo Facility

The kind of market imbalances that the facility is meant to prevent are less likely when bank reserves are plentiful. During the pandemic, the amount of bank reserves increased significantly because of the Fed's policies and interventions. Large asset purchases financed with reserves increased the total amount of outstanding reserves to over $4 trillion.

Thus, given the abundance of cash in the market, which is also available to primary dealers, the SRF is not currently being used and it seems unlikely to see much activity soon. Rather, the expectation is that the facility will be more relevant when the Fed starts balance sheet normalization and the level of reserves in the banking system declines.

However, it is possible that the facility — originally intended mainly for interest rate control — could become a backup source of short-term funding for banks and primary dealers experiencing distress, either idiosyncratic or systemic, even before reserves become scarce.

The last time reserves were closer to becoming scarce was in the late summer of 2019. By September of that year, reserves were down to about $1.4 trillion. While survey measures suggested that the minimum "comfortable" level of reserves was still somewhat lower — as noted in the 2019 article "Estimating System Demand for Reserve Balances Using the 2018 Senior Financial Officer Survey" — market and other frictions likely limited the rapid flow of reserves from one group of banks to another. As a case in point, when the rate on repos spiked on Sept. 16-17, 2019, JPMorgan Chase CEO Jamie Dimon identified resolution-related liquidity requirements as one of the reasons why his firm did not use existing cash holdings to lend in the market.

A similar sentiment was reflected in the Fed's Senior Financial Officer Survey at the time. The survey is a largely qualitative and voluntary survey of banking financial executives about liability management practices and other financial markets related topics. The banks included in the survey hold the lion's share of total reserve balances in the banking system and represent a wide range of sizes and business models. In the August 2019 survey (PDF), most respondents indicated that the second-most important driver of demand for reserves (after meeting routine intraday payment flows) was internal liquidity stress metrics.

To the extent that the SRF allows banks to quickly transform liquid assets such as Treasuries and mortgage-backed securities (MBS) into cash, it could help ease regulatory constraints: As banks strive to comply with regulatory expectations, they accumulate cash ex ante and are often reluctant to use cash ex post.4 This could be particularly relevant when planning and executing the resolution of systemic financial institutions, as we discuss next.

The Role of Liquidity in the Resolution of Large Banking Firms

There are two primary processes associated with resolution planning in the U.S.:

- Title I of the Dodd-Frank Act requires that larger banking organizations in the U.S. develop resolution plans (sometimes known as living wills), preparing them to file under the U.S. Bankruptcy Code.

- Title II of the Dodd-Frank Act establishes a regulated wind-down process overseen by the Federal Deposit Insurance Corp. as receiver of the bank holding company.

The Bankruptcy Code provides for a court-administered process — rather than one guided by regulatory agencies — and makes Title I procedures the generally preferred approach from an ex ante perspective. However, in a systemic crisis when credit can be scarce, Title II resolution is considered to have an important advantage relative to Title I bankruptcy: It allows the use of a line of credit from the U.S. Treasury to stabilize the firm. It should be noted, though, that this credit is supposed to be paid back in full by the end of the resolution process. Furthermore, Title II requires official authorization, which triggers a "key turning" event that involves the dismissal of top officials at the failed bank.

Title I is nominally the preferred option for a G-SIB resolution because it limits taxpayer burden and helps curb moral hazard coming from bailouts, as explained in the 2015 article "Understanding Living Wills." The main intent of resolution planning, then, is to minimize the need to invoke an assisted (Title II) resolution and, more generally, the potential for a government bailout.

With that overarching objective, the planning is aimed at limiting any significant negative spillovers from an idiosyncratic bank failure to the rest of the financial system and the aggregate economy in general. In the context of Title I resolution, all U.S. G-SIBs have converged on adopting the single point of entry (SPOE) strategy. Its logic is to self-identify, self-fund and self-capitalize its critical subsidiaries (that is, material entities) during the bankruptcy process at the expense of the parent company's shareholders and external creditors.

A key factor for the success of an unassisted (Title I) resolution is to guarantee that large institutions hold enough liquidity to sustain them through not only the deep stress period preceding possible failure but also the post-bankruptcy process with its predictable funding needs. If the planning does not credibly address those funding needs, Title II is likely to be the preferred option as it includes access to the government credit line.5

The supervisory guidance associated with Title I has pushed firms to develop their own internal models of liquidity provisioning. This liquidity planning makes the failure of systemic banks easier to deal with in bankruptcy, as it allows the failing firm to more gradually sell or wind down its critical subsidiaries or sell other assets. However, it can also give banks an incentive to hoard liquidity, especially in times of uncertainty. This emphasis on the availability of liquid assets has also been driven by more standard liquidity regulations, such as the liquidity coverage ratio (LCR). It should be noted, though, that the requirements for resolution purposes are possibly more stringent given that they are intended to address the complete wind-down of the firm, not just a 30-day stress period like the LCR does.

In the context of SPOE, the Resolution Liquidity Execution Need (RLEN) is the model used by firms to estimate the level of liquidity needed in the event of failure and possible reorganization. This estimate not only informs when the bank holding company should file for bankruptcy and how much liquidity is needed for the resolution process, but also possibly the real-time support provided by the parent to its material entities in the runway to filing for bankruptcy.

Furthermore, embedded in RLEN is an estimate of the intraday reserves and other liquidity necessary to maintain continuity of access to payments, clearing and settlement arrangements. This would include the need for funding same-day settlement if financial market utilities, agent banks and central banks cut off the firm's material entities from intraday credit. Under current guidance — which does not contemplate any borrowing from the discount window or the SRF — this intraday liquidity is largely provisioned for with cash reserves held at the central bank of the relevant jurisdiction and with other liquidity held for guaranteeing access to clearing and settlement services from correspondent banks, exchanges, clearinghouses, etc.6

Bank Resolution Planning and the Standing Repo Facility's Impact

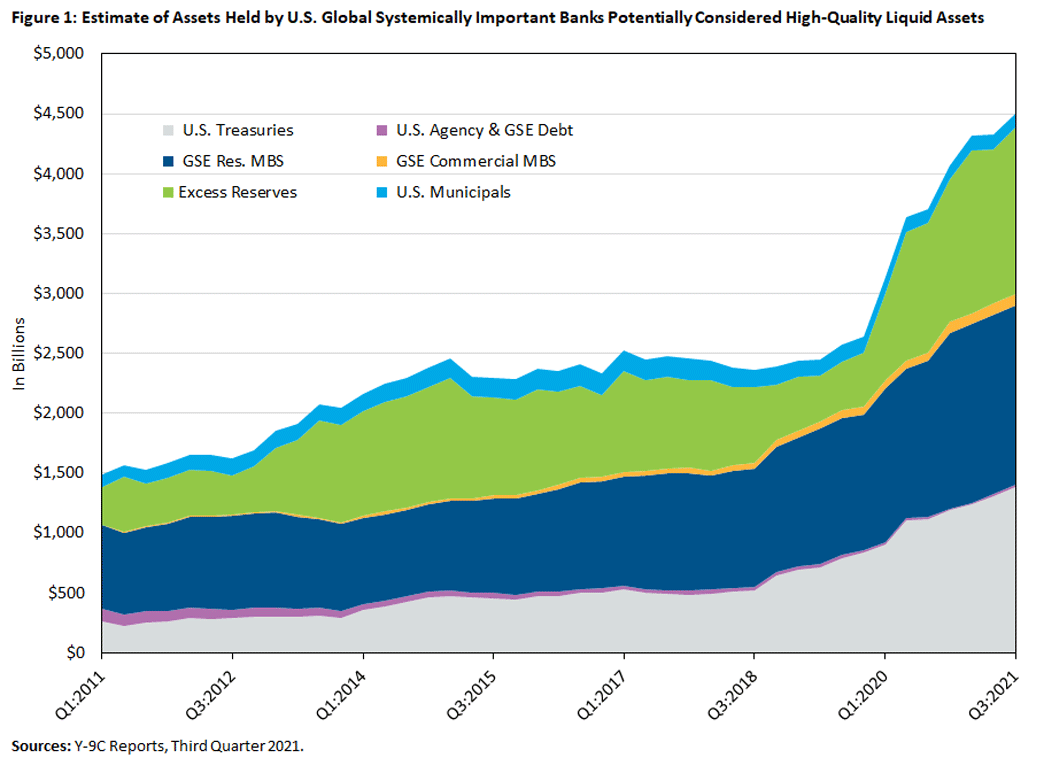

With the creation of the SRF, the Fed stands ready to lend cash through repo contracts that use open-market-operations eligible assets as collateral. These assets constitute the lion's share of the total high-quality liquid assets (HQLAs) held by G-SIBs, as seen in Figure 1.7

The figure shows the time series for HQLAs and, in particular, the three main categories of assets that are eligible as collateral at the SRF:

- U.S. Treasuries

- Agency and government-sponsored enterprise debt

- Residential MBS securities

While excess reserves have fluctuated significantly since 2011, eligible collateral holdings increased steadily from about $1 trillion to just under $3 trillion in the third quarter of 2021. As a percentage of the combined assets of U.S. G-SIBs, holdings of SRF-eligible collateral went from about 10 percent to 20 percent in the last decade.

While so far it is not clear whether banks could include access to the SRF in their resolution planning, any eventual guidance from regulators favoring that possibility may induce systemic firms to rebalance their cash and other liquidity provisioning toward HQLAs accepted at the facility, which can yield a higher return than cash. This is because, in all likelihood, assets accepted by the facility as collateral will be less exposed to trading discounts at times of financial distress.

Current public resolution plans do not contemplate firms' access to public facilities, and while recognizing the need for quick monetization of HQLA, the plans assume little difficulty for doing so in the market. A few firms reference access to the Federal Home Loan Banks — which take broader collateral than the SRF — as a potential contingent source of liquidity in resolution. If banks were able to use the SRF, it would constitute a new source of liquidity provided by the central bank. Although this increased support may dampen market discipline, the benefits on the functioning of repo and other short-term funding markets might be substantial and worth the risks.

Beyond decreasing the costs of resolution planning, the SRF could also impact outcomes ex post in the event of an actual G-SIB failure. There are two main forces that would make choosing Title I bankruptcy over Title II resolution more likely with the SRF:

- Having the failing firm be able to more predictably self-fund (and time) its bankruptcy decision

- Reducing asset liquidation's impact on market functioning, which would then also dampen the ripple effects to other firms holding those assets

The availability of funding through the SRF could help during a Title II procedure as well, and in doing so, it would make government-provided funding less critical. This is key, as it would erode some of the advantage of choosing a Title II liquidation. Then, by making the ex post choice of assisted bankruptcy a less advantageous option, the SRF could increase market discipline ex ante.

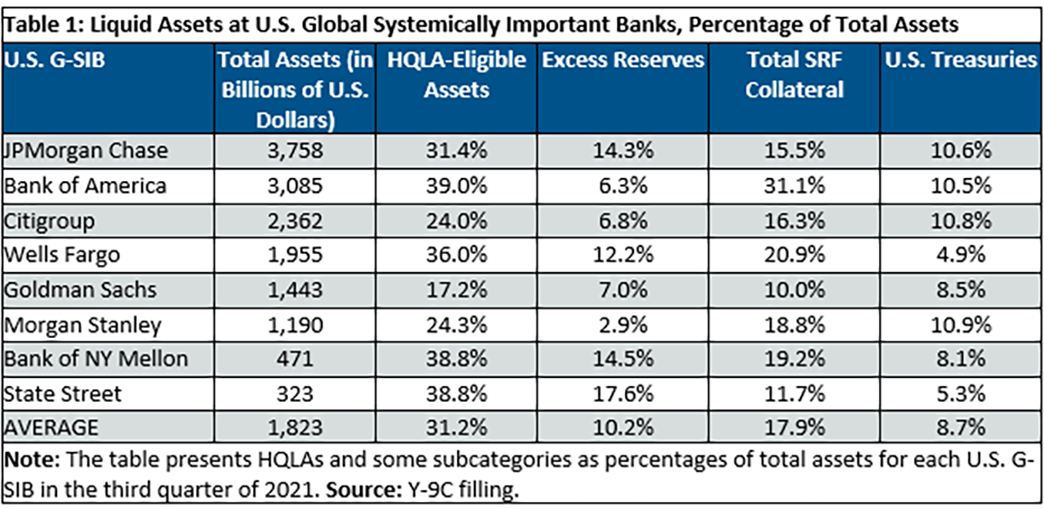

Table 1 presents the relative importance of different liquid assets for the current U.S. G-SIBs.

On average, at the level of the corporations, these firms hold about 30 percent of total assets in HQLAs, of which excess reserves represent about a third. Of the other two-thirds, most of it is eligible as collateral at the SRF (Treasuries, agency securities and certain residential MBS, which represent 17.9 percent of total assets).

Of course, using the SRF for resolution planning purposes, if approved, could drive changes to this split. The table shows, however, significant heterogeneity in the portfolio of liquid assets across entities, suggesting that the changes could be idiosyncratic to the business needs of each bank and, hence, hard to predict.

Standing Repo Facility and Timing of Bankruptcy Filings

In an actual resolution, the SRF could also be beneficial in reducing uncertainty around the timing of an SPOE bankruptcy filing (Title I). Appropriate timing is important for the success of the SPOE strategy. In particular, filing late could leave the firm without sufficient liquidity and capital to stabilize material entities.

The public resolution plans do account for uncertainty over the triggers considered for bankruptcy. Yet, the SRF could help to reduce volatility in repo markets and around HQLA valuations, which is critical in better assessing how liquidity holdings compare with the needs estimated in RLEN. If firms can have a clearer notion of their available liquidity for self-funding their resolution, they can more reliably judge the timing of the bankruptcy filing and the entire SPOE strategy. Firms may, however, adapt to this enhancement by partially reducing buffers around the calculated triggers.

In principle, the reduction in the need for cash holdings intended for resolution planning could also ease occasional pressures on Treasuries and MBS markets. The SRF is likely to reduce the precautionary demand for cash by financial institutions. In effect, entities can draw down their cash holdings by investing more in SRF-eligible collateral, which would also count for fulfilling intraday liquidity targets, given that they can be quickly and safely swapped for cash if needed. However, the infrastructure details associated with the SRF — like the timing of its once-a-day auction — may limit the role that it can play in the allocation of intraday liquidity.

Relatedly, this effect on banks' demand for reserves was identified early on as one important benefit of the SRF in the process of monetary policy implementation. In particular, a lower demand for reserves would allow the Fed to conduct monetary policy using a (so called) floor system with a minimal necessary size of its balance sheet, as discussed in the 2019 article "Why the Fed Should Create a Standing Repo Facility." The benefits of a smaller Fed balance sheet are multiple, important among them being political economy considerations.

Conclusion

Guidance regarding the use of the new SRF has the potential to shape its impact both on monetary policy and on the health of the banking system, including the important aspect of planning for resolution of large financial institutions in distress.

If regulators allow banks to incorporate the use of the SRF in their resolution plans, their response may be to shift liquidity towards Treasuries and agency debt and away from cash. The facility will also reduce uncertainty in the value of high-quality collateral. These effects have the potential to reduce the cost of planning for resolution.

When considering the impact of the SRF on resolution planning, it is important to recognize that the existence of a facility that allows borrowing at favorable terms may erode some of the market discipline that helps curb moral hazard. However, given the critical nature of the collateral accepted by the SRF, the potential market stress associated with seeking market discipline through this channel cannot be ignored. In fact, the SRF is likely to contribute to the smooth transmission of monetary policy during a crisis, which is particularly relevant since the failure of a global systemic bank can create generalized financial-markets distress.

One way to deal more directly with the moral hazard problems associated with potential bailouts is to make bankruptcy resolution more credible, as noted in the 2015 articles "Understanding Living Wills" and "Living Wills for Systemically Important Financial Institutions: Some Expected Benefits and Challenges." Contingent on specific guidance by regulators, the SRF could indeed make unassisted bankruptcy a more attractive option. By providing affordable and predictable short-term liquidity — not only to a bank in distress but also to a wide range of market participants — the SRF could ease contagion concerns that often arise in these situations. As a result, the presence of the SRF could actually tilt the balance for regulators in favor of unassisted bankruptcy, as it diminishes the advantage of pursuing an assisted (Title II) resolution process that explicitly contemplates access to temporary funding from the government.

The authors would like to thank Kyler Kirk for excellent research assistance, and Jeff Gerlach, Mark House, and Mason Laird for comments and suggestions. All remaining imprecisions are our own.

Huberto M. Ennis and Arantxa Jarque are economists in the Research Department at the Federal Reserve Bank of Richmond. Hoossam Malek is in the Recovery and Resolution Group at the Federal Reserve Board of Governors.

1

The Fed conducts open market operations in the repo market through the New York Fed trading desk, which goes to the market as needed and offers to enter repo transactions for a given total amount. Standing facilities, instead, are open every day, and financial institutions decide how much to demand (within certain limits).

2

G-SIBs are large banking corporations so designated annually by the Financial Stability Board due to the extent of their complexity, cross jurisdictional activity, interconnectedness, size and substitutability. These institutions are subject to higher requirements of capital buffers, total loss absorbing capacity, resolvability and supervisory expectations.

3

For a more detailed discussion of the role and configuration of the SRF, see the 2021 article "The Fed's Evolving Involvement in the Repo Markets."

4

Recent proposals by the Fed to modify its payment systems risk policy are aimed at mitigating some of the pressures firms feel about holding intraday cash. The objective is to expand access to collateralized intraday credit and to clarify the eligibility standards for accessing uncollateralized intraday credit. These measures, however, seem less relevant for G-SIBs, which already had in place ample collateralized intraday credit options with the Fed.

5

More generally, resolution planning is a valuable avenue for scaling back perceived government backstops of the financial system. See the 2015 article "Living Wills for Systemically Important Financial Institutions: Some Expected Benefits and Challenges" for a detailed discussion of the idea.

6

Aside from RLEN, there are other processes — such as the internal liquidity stress test (ILST) — which may also be contributing to firms' intraday liquidity provisioning. Large banking organizations are required to conduct ILSTs, which regulators oversee. To the extent that these ILSTs include intraday buffering, the firm will prioritize holding cash at the expense of other money market investments.

7

Assets that qualify as HQLAs should be easily and immediately convertible into cash with little or no expected loss of value during a period of liquidity stress, as explained in the Federal Register: Liquidity Coverage Ratio: Liquidity Risk Measurement Standards.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond, the Board of Governors or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us