Islamic Banking, American Regulation

For some American Muslims, Sharia-compliant banks are an important part of the financial landscape

By

Renee Haltom

Econ Focus

Second Quarter 2014

Most Americans don't have to think about whether basic banking services are available. If anything, it feels like the choices in savings accounts, auto loans, mortgages, and investment vehicles are overwhelming.

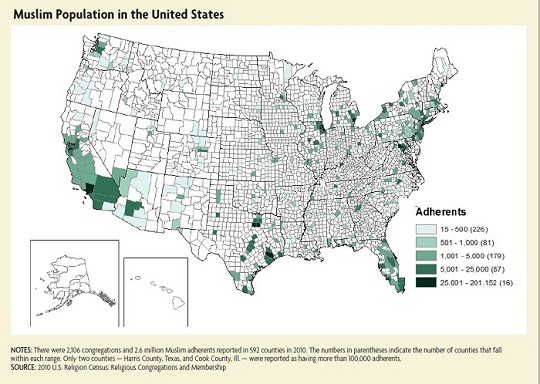

Not so for a certain segment of the U.S. population. There were roughly 2.8 million Muslims in the United States as of 2010, according to the Pew Research Center's Religion and Public Life Project, though estimates vary (see map). The most recent study published by the Association of Statisticians of American Religious Bodies estimates that Islam was the fastest-growing religion in the United States between 2000 and 2010. Yet there are relatively few financial products available here for those followers who require their financial contracts to comply with Islamic laws and moral codes, called Sharia law.

Islamic finance is rooted in the principle that investments should create social value and not merely wealth. The Quran, the 1,400-year-old text that governs followers of Islam, prohibits riba, the charging or receiving of monetary benefit from lending money, interpreted in modern terms as a prohibition against interest. Islamic finance also prohibits excess risk or uncertainty (gharar), gambling (maysir), and sinful activities (haram). Transactions generally must be tied to real, tangible assets.

Globally, the Islamic finance industry is between $1 trillion and $1.5 trillion in size, according to the World Bank, in the vicinity of Australia's or Spain's gross domestic product. It's unsurprising, perhaps, since Muslims are almost a quarter of the world’s population. That's an upper bound on the demand for Islamic finance, since not all Muslims demand Sharia-compliant contracts. But in Muslim-majority countries like Bangladesh, Islamic financial products constitute as much as two-thirds of total financial sector assets. There are more than 400 Islamic financial institutions across 58 countries. Roughly 5 percent of total Islamic financial assets are housed in non-Muslim regions like America, Europe, and Australia.

The United States’ Muslim population is roughly equal to that of the United Kingdom, a country that houses $19 billion in Islamic financial institution assets, more than 20 banks, and six that provide Sharia-compliant products exclusively. Yet our market for Islamic financial products is much smaller. There's no single list of participating firms or aggregate estimate of assets, but one can find roughly a dozen firms that routinely offer Islamic banking and investment products to businesses and consumers, though several don’t even market such products on their websites.

At the same time, this is an industry on the rise. Just 20 years ago, there were few Islamic financial products being offered at all in the United States. The industry is rapidly growing and adapting to American regulation. Should we expect it to be a large presence in our future financial landscape?

How Does it Work?

Islamic finance may be rooted in ancient texts, but as an industry it is relatively young.

The broader field of Islamic economics originated in 1930s India, when the country's Muslim population, then about one-fifth of its total, feared marginalization by British colonialism and the Hindu-led movement for Indian independence. Heavily indebted Muslim farmers throughout the country were at risk of losing their land. Scholars blamed an abandonment of Islamic principles and called for a return to "true" Islam. Economist Timur Kuran of Duke University, author of several books and articles on Islamic economics, has argued that this revival was part of a broader movement to restore Muslims to their faith, carve out an identity for Muslim minorities, and generally protect Muslim interests. The state of Pakistan emerged from the same effort.

Usury discussions in religious texts far predate this movement, of course. Many followers of Islam, along with other religions, loosened usury restrictions over time, until the last century when older notions of usurious interest were revitalized. Still, what constitutes riba has long been controversial. To some scholars, it means excessive interest — which led poor, indebted citizens to slavery in medieval times — while to others, it means any interest at all. Scholars have also disagreed on the virtues of charging interest for business investment versus consumption, allowing for inflation compensation, and a host of other matters.

Modern Islamic finance takes the narrower interpretation that no interest is permissible. Three alternative products are available in the United States. One of the most common contracts is musharaka, in which the lender and customer own an asset together, with the borrower's share of the property increasing gradually with his payments until he assumes ownership entirely, with profits and losses shared. In a murabaha contract, the lender purchases an asset — a home or even commercial equipment — on behalf of a borrower, who gradually pays back the principal plus an agreed-upon markup and assumes ownership at the end. Ijara contracts resemble a lease-to-own arrangement that includes both repayment of principal and a rental fee for exclusive use of the asset.

The first bank following Islamic law opened in Egypt in 1963. Following the global oil boom, the industry developed in earnest in the Middle East in the mid-1970s. In the 1990s, the first international accounting standards were developed for Islamic finance, and the first market emerged for Islamic bonds. Those bonds, called sukuk, tie investments to tangible assets that issue payment streams based on their revenues, much like securitized equity financing.

Islamic finance came to the United States in the 1980s when two institutions opened on the West Coast. Their investment and home finance services were available only regionally. The market broadened considerably in the late 1990s, paralleling the Muslim population growth in the United States: 50 percent in the 1990s, and two-thirds in the 2000s.

The institutions operational today provide services in several states, most prevalently where the Muslim population is concentrated. University Islamic Financial (a subsidiary of University Bank) based in Ann Arbor, Mich., serving the large Muslim population of metropolitan Detroit and surrounding states, is the first and only exclusively Sharia-compliant bank in the United States — it offers no other products. Devon Bank in Chicago is the only other bank regularly offering Islamic financing products. Reston, Va.- based Guidance Residential is the largest nonbank financial institution offering Islamic finance services, having provided more than $3 billion — which it claims is nearly 80 percent of the total — in musharaka mortgage financing in 22 states since its doors opened in 2002. California-based LARIBA is another large Islamic mortgage lender, and it also provides business financing.

Is it Really Islamic?

To critics, Islamic finance is a distinction without a difference. According to research by Feisal Khan, an economics professor at Hobart and William Smith Colleges in upstate New York, most Islamic finance transactions are economically indistinguishable from traditional, debt- and interest-based finance. Where there is principal and a payment plan, there is an implied interest rate, Khan argued in a 2010 article. He is not the first economist to make such a claim. Many Islamic scholars argue that murabaha contracts don't share risk and thus are not Sharia compliant — and experts estimate that such contracts constitute up to 80 percent of the global Islamic finance volume.

Other economists have noted that the terms of Islamic financial contracts often move with market interest rates. In the United States, Islamic financial products are frequently marketed with information about implied interest rates to allow customers to compare prices or simply to comply with American regulation. A study of Malaysia, the world's largest Islamic finance market, found that Islamic deposit rates fluctuate in step with market interest rates.

To economists, it would not be surprising if Islamic and traditional finance tended to converge. A tenet of banking theory is that debt contracts with collateral minimize risk better than equity contracts when it is costly for banks to identify borrower-specific risks. Equity contracts, by comparison, entail greater monitoring costs or more risk. If equity contracts are less efficient, then one would expect banking institutions to gravitate away from them.

But to Islamic finance advocates, equivalent pricing does not create an equivalent product. Stephen Ranzini, president and CEO of University Bancorp, the holding company of the Islamic bank, acknowledges that there are firms that market themselves as Sharia compliant but that are taking standard loan documents and replacing the word "interest" with "lease." But he says this does not describe the majority of Islamic financial service providers, who are concerned with the intent behind Islamic law. "True Islamic finance is absolutely not the same as traditional finance. The contracts are different; the risks are different."

Ranzini also notes that Islamic lending is designed to protect borrowers who fall on hard times: Recourse if a borrower is unable to pay is rare, and firms generally cannot profit from a borrower’s financial distress since late fees in most cases can only cover the cost of collection. Most Islamic financial institutions have a supervisory board of Sharia scholars to review and approve the details of contracts.

Islamic investment firms have some more obvious differences from traditional finance. Their holdings must not involve alcohol, gambling, pork-based food — and according to some Islamic scholars, defense and weaponry, tobacco, or entertainment. Perhaps surprisingly, the United States is the fourth-largest domicile of Islamic investment funds, due almost entirely to the Amana Mutual Funds Trust based in Bellingham, Wash., whose income and growth funds hold almost $3.5 billion in assets. As a group, Islamic investment funds hold primarily equities. Many employ a third party to screen the investments for Sharia compliance, or halal, often as defined by the Accounting and Auditing Organization for Islamic Financial Institutions, a body that sets global finance standards. Eligible investments typically must not derive more than 5 percent of income from activities considered unethical.

Regulatory Challenges

Regardless of whether Islamic finance is truly distinct, its economic similarities to traditional finance have opened doors in the United States.

Banks here are normally prohibited from taking on partnership or equity stakes in real estate, a provision meant to limit speculation. But in Islamic finance, the bank assumes formal ownership. Regulators in the United States have held, however, that Islamic finance is compatible with the prohibition on real estate investments in some cases. In 1997, the United Bank of Kuwait (UBK), which then had a branch in New York, requested interpretive letters from its regulator, the Office of the Comptroller of the Currency (OCC), on ijara and murabaha mortgage products. The OCC approved them on the very grounds that they were economically equivalent to traditional products.

In the OCC's view, because the purchase and sale transactions are executed simultaneously, the bank's ownership is merely for "a moment in time," and therefore the Islamic contracts avoid the type of risk that real estate restrictions were intended to limit. (The joint ownership that defines musharaka contracts, on the other hand, is not currently approved for use by banks and is used in the United States only by nonbank mortgage lenders.) From an accounting standpoint, the transaction appears as a loan (an asset) on the bank's balance sheet. The borrower is responsible for maintaining the property and paying all expenses, and in the event of default, the bank may sell it to recover what is owed, as in a mortgage. UBK left the U.S. market in 2000 after financing the purchase of 60 homes, but regulators have since applied the OCC's guidance to other institutions.

In other ways, however, Sharia requirements have made proliferation of Islamic finance difficult. Possibly because the products are unfamiliar to many investors, there is a smaller secondary market for Islamic financial products, so it has been harder for Islamic mortgage lenders to remain liquid, hindering the market's growth. In the United States, housing agencies Freddie Mac and Fannie Mae started buying Islamic mortgage products in 2001 and 2003, respectively, to provide liquidity, and they are now the primary investors in Islamic mortgages. By 2007, one firm, Guidance Residential, was relying on more than $1 billion in financing from Freddie Mac.

Overall, there are few opportunities to take advantage of economies of scale with Islamic finance. "There's not a big enough market now for large, national banks to offer Islamic products, and only in states with the largest Muslim concentrations is it worthwhile for the smaller banks to expand into that market," says Blake Goud, Islamic finance expert with the Thomson Reuters Islamic Finance Gateway.

Moreover, traditional deposit insurance — which banks rely on for stability — is at odds with Sharia law. In 2002, Virginia-based SHAPE Financial Corp. sought FDIC deposit insurance for an Islamic deposit-like product for which returns would fluctuate with the bank’s profits and losses. The FDIC refused because the deposit could decline in value, so SHAPE had to alter the product to be based solely on profit — not loss — sharing. This is now the United States' only Islamic deposit product, currently being offered by one institution, University Bank. Muslim depositors have been known to donate undesired proceeds to Islamic charities, a way to offset, or perhaps make peace with, a degree of Sharia noncompliance.

Prospects in the United States

Though the growth rate of the American Muslim population may have peaked due to demographics, it'll remain high in the near term. Globally, the Muslim population is forecast to grow twice as fast as the non-Muslim population through 2030. They'll continue to be small minorities here but will still more than double in that timeframe.

Some factors seem to suggest there is large latent demand for Islamic financial products in the United States. On average, Muslims in the United States are relatively high income and highly educated. They are also significantly younger than the average population — the median Muslim in North America is just 26, but the average American is 37 — and thus still approaching peak earning years.

But there are little data on what fraction of the U.S. Muslim population actually demands Sharia-compliant financial services. "There are not even consistent estimates of the size of the Muslim population," Goud notes. A 1998 study from LARIBA contended that at most 2 percent of American Muslims will use only Islamic financing. The alternative is to not use financial services, to use conventional Western financial products, or to rely on informal avenues, such as borrowing and investing among family and friends.

There are limited data from countries with larger Muslim populations. A 2013 World Bank study of 64 such countries found that Muslims were significantly less likely than non-Muslims to have formal banking accounts, but they were no less likely to use financial services overall. It's not clear whether that suggests simply a preference for informal financial services, or rather that customers could be drawn in if the right compliant products were available. Four percent of unbanked people in non-Muslim countries cite religious reasons, according to the World Bank, but the number is 7 percent in Organization of Islamic Cooperation countries, suggesting that Muslims may be somewhat more likely to have religious reasons for avoiding formal financial services. There are no data on whether U.S. Muslims are relatively unbanked. Only one-third of U.S. Muslims own their homes, compared with 58 percent of the general public, although that discrepancy could be partly explained by the relatively young age of the U.S. Muslim population (the average first-time American homebuyer is 34 years old).

At the same time, there's no reason Islamic financial products must be restricted to Muslims, Ranzini says. For example, there is considerable overlap between Islamic finance and so-called "socially responsible" investing, such as mutual funds that buy equities of environmentally friendly or tobacco-free companies. A 2013 survey commissioned by Abu Dhabi Islamic Bank found that between 12 percent and 20 percent of customers in Turkey, Egypt, the United Arab Emirates, and Indonesia said they would bank only with Sharia-compliant institutions. But up to half said they preferred ethical investing, whether or not it was Islamic. If anything, Goud argues, Islamic standards are more restrictive because "socially responsible" investment products generally do not exclude leverage.

Because of restrictions on leverage, proponents argue that Islamic finance could be good for financial stability. "Islamic investors sold their stock in Worldcom and Enron as those companies' leverage levels rose. Some potentially bad behaviors — excessive leverage and excessive financial engineering — wouldn't even be possible in Islamic finance," Ranzini says. Globally, Islamic finance assets have grown by more than 20 percent annually since the financial crisis, according to the Islamic Financial Services Board (IFSB), a multinational assembly that sets international standards for the industry.

It's not that Islamic banks are better performers as a rule, since what they gain in safety, they may lose in efficiency. Where the differences seem to matter is during crises. A study by international economists Thorsten Beck, Asli Demirguc-Kunt, and Ouarda Merrouche of several hundred institutions in 22 countries found that while Islamic banks tend to be less efficient, they are less prone to disintermediation during financial crises, when they remain better capitalized with lower loan losses. Separate studies by the International Monetary Fund and the IFSB also found superior performance following the 2007-2008 crisis.

Another factor is that non-Muslim governments are moving toward issuing sukuk to draw the investment of oil-rich Muslim countries. In June, the United Kingdom issued more than $330 million in sukuk — compared with more than $100 billion in global sukuk offerings in 2013 — becoming the first country outside the Islamic world to do so. Prime Minister David Cameron said he wanted to make London "one of the great capitals of Islamic finance anywhere in the world." Luxembourg, Hong Kong, and South Africa have announced plans for their own offerings. Sukuk may also provide liquid assets to help domestic Islamic banks manage their balance sheets.

Whether Islamic finance continues to grow in the United States, the market is a small but significant segment of the American financial system.

Readings

Ahmed, Jaseem. "Keynote Address by the Secretary-General of the IFSB." Speech at the 2014 London Sukuk Summit, June 18, 2014.

Baxter Jr., Thomas C. "Regulation of Islamic Financial Services in the United States." Speech before the Seminar on Legal Issues in the Islamic Financial Services Industry, March 2, 2005.

Beck, Thorsten, Asil Demirguc-Kunt, and Ouarda Merrouche. "Islamic vs. Conventional Banking: Business Model, Efficiency, and Stability." Journal of Banking and Finance, vol. 37, no. 2, February 2013, pp. 433-447. (Paper available online by subscription.)

Chong, Beng Soon, and Ming-Hua Liu. "Islamic Banking: Interest-Free or Interest-Based?" Pacific-Basin Finance Journal, vol. 17, no. 1, January 2009, pp. 125-144. (Paper available online by subscription.)

Khan, Feisal. "How 'Islamic' is Islamic Banking?" Journal of Economic Behavior & Organization, vol. 76, no. 3, December 2010, pp. 805-820. (Paper available online by subscription.)

Kuran, Timur. "The Genesis of Islamic Economics: A Chapter in the Politics of Muslim Identity." Social Research, vol. 64, no. 2, Summer 1997, pp. 301-338.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Thank you for signing up!

As a new subscriber, you will need to confirm your request to receive email notifications from the Richmond Fed. Please click the confirm subscription link in the email to activate your request.

If you do not receive a confirmation email, check your junk or spam folder as the email may have been diverted.

Thank you for signing up!

You can unsubscribe at any time using the Unsubscribe link at the bottom of every email.

Contact Us