So what happened? Why were the doomsayers so wrong? Did government policies go too far in averting an overpopulation crisis? Research shows that there never really was an overpopulation crisis in the sense that many feared. The demographic movements of the last two centuries were largely natural responses to advances in science and medicine, and population growth seems to have been a positive force for many countries.

False Prophets

Concerns about food and resource scarcities due to overpopulation were certainly not new to the 1970s. In fact, the predictions of Ehrlich and others in some ways echoed the writings of 18th century economist Thomas Malthus. In his 1798 Essay on the Principle of Population, Malthus observed that the Earth's supply of arable land was largely fixed. He believed that improvements to existing land could increase the yield of subsistence, but only gradually. On the other hand, population, when unbounded from any constraints, would double roughly every 25 years, quickly outpacing food supply.

"By that law of our nature which makes food necessary to the life of man, the effects of these two unequal powers must be kept equal," Malthus wrote. "This implies a strong and constantly operating check on population from the difficulty of subsistence." Malthus saw two possible types of checks: voluntary (choosing to marry later, have fewer children) or involuntary (famine, war). Malthus believed involuntary checks were typically not necessary because people took into account their ability to provide for children when deciding to have a family. But he saw little means for near-term improvement. Malthus thought that population would increase when food became more available and economic conditions were good and contract during lean times, resulting in a populace that always hovered around subsistence levels.

His view largely fit the pattern of human history to that point, but it failed to predict the two centuries that followed. Population and productivity of arable land increased dramatically, while the quantity of land used for agriculture remained largely the same. In fact, economic research suggests that gains in agricultural productivity may have occurred because of rapid population growth. In a 1999 survey of more than 70 studies of the impact of population growth on the land quality of developing nations, Scott Templeton of Clemson University and Sara Scherr, president of Ecoagriculture Partners (a nonprofit that supports sustainable agricultural development), found a "U-shaped" relationship between population density and land productivity. All else being equal, increases in local population density make existing land more expensive and labor cheaper.

Initially, this can lead to some resource degradation in the form of deforestation as farmers use land more frequently or convert land to agricultural production. But as labor becomes comparatively cheaper, people begin to invest in techniques that economize on land, like soil fertilization or land improvements like terraces.

Similar economic processes can work to extend other natural resources as well. The late University of Maryland economist Julian Simon wrote in his 1981 book The Ultimate Resource that most natural resources were actually becoming more abundant in the 20th century despite rapidly growing populations. Simon argued that as long as markets were functioning, resource scarcity from higher populations would be reflected in higher prices, which in turn would prompt people to seek new ways to extract previously unprofitable resources or develop new ways to conserve and economize existing resources.

Simon famously wagered Ehrlich and his colleagues in 1980 that any raw materials of their choosing would be cheaper in 10 years after correcting for inflation, indicating that they had in fact become less scarce. Ehrlich selected $1,000 worth of five different metals, agreeing that the loser of the bet would pay the other the difference in value 10 years later. In 1990, all five metals were significantly cheaper, and Ehrlich sent Simon a check for $576.07. In some ways, Simon was lucky. Some of the metals Ehrlich chose were at cyclical highs. Had the bet been conducted during each decade of the 20th century, Simon would have come out ahead only about half of the time. And despite his overall optimism about the positive effects of population growth, Simon readily acknowledged that they were contingent on many other factors, like government institutions and functioning markets.

"A lot depends on the context," says John Pender, a senior economist at the U.S. Department of Agriculture who studied the impact of population growth in developing countries like Honduras and Ethiopia. In a contribution to the 2001 book Population Matters, Pender found that increased population was negatively associated with crop yields and land sustainability in Honduras. But the effects were minor compared with more important factors like underdeveloped infrastructure and inefficient government policies.

Population can also impact resource sustainability through its interaction with economic development. "In a densely populated, resource-dependent economy, the real problem is poverty," says Pender. "When you're depending on a very small number of assets, you may sometimes be led to degrade your resources."

Indeed, economists over the last 50 years have tried to pinpoint how population growth affects the economy.

Demography and Economic Growth

Does having more people help or hinder economic growth? As the typical economist refrain goes: It depends. Initially, there was little evidence that the rate of population growth played much role in economic development. But by looking at both sources of population growth — rising fertility and falling mortality — economists have found that population does indeed influence economic potential in important ways.

The majority of the extraordinary population increase over the last century has been due to reductions in infant mortality and gains in overall life expectancy. In 1900, average life expectancy was 30 years, but by 2005, it had more than doubled to 66 years worldwide, and most demographers expect it to continue to rise. In addition to improving the quality of life of individuals around the world, such gains in lifespan have fostered economic growth. As people live longer, it becomes more profitable for them to invest in training and education. This means workers are better skilled when they enter the workforce and they live longer, healthier, more productive lives. And these gains have been widespread. According to research by Harvard University School of Public Health economists David Bloom and David Canning, infant mortality in poor countries is one-tenth to one-thirtieth as much as it was in countries with comparable levels of income in the 19th century.

On the other hand, population growth driven by high fertility rates seems to be correlated with lower income, as measured by GDP per capita. The data seem to suggest that many countries fall into one of two "clubs": low income and high fertility, or high income and low fertility. Just as higher life expectancy increases incentives to develop human capital, higher fertility rates make it more difficult to do so.

"If families are very large, then households have less money to invest in their children’s education," says Abdo Yazbeck, lead economist at the World Bank's Africa division. Having many children back-to-back also limits the opportunities for women to enter the workforce.

But the correlation between income and fertility runs in the opposite direction as well. The late University of Chicago economist and Nobel laureate Gary Becker showed that economic conditions influence family size decisions. In wealthier, developed nations where education and labor market opportunities for women are higher, the cost of forgoing wages to have children is greater, leading couples to have fewer children. Conversely, in nations with poor economic or education opportunities, women often marry younger and have more children at a younger age. This means the strong correlation in the data may reflect the tendency for countries to be pushed into one club or the other through positive or negative feedback effects. That is, good labor market and education opportunities reinforce lower fertility rates and vice versa.

The good news for developing nations is that mortality rates have been declining worldwide due to the spread of modern medicine, and there are also strong feedback effects between mortality and fertility rates. When mortality rates are high, families tend to "overshoot" their desired family size to insure against the possibility that some of their children may not survive. But as mortality rates fall, families adjust and fertility rates decline. Depending on the speed of adjustment, this process can create a "demographic transition," which creates the potential for significant economic gains.

"As both mortality and fertility decline, it changes the age structure of the population, impacting what is known as the dependency ratio," explains Yazbeck. The dependency ratio refers to the number of young people (up to age 14) and old people (age 65 and over) in an economy compared to the number of working-age individuals.

High fertility rates imply a higher dependency ratio, as there are a larger number of nonworking children per family. This can act as a drag on economic growth as more resources are required for education and childcare, potentially diverting them from more productive areas of the economy. But if fertility rates change quickly in response to declining mortality, then the dependency ratio can decline as a "baby boom" generation enters the workforce with fewer dependents to care for.

"The key is the speed at which this process takes place. If both legs of the transition move fast, we now have very good evidence to suggest the impacts on the economy are huge," says Yazbeck.

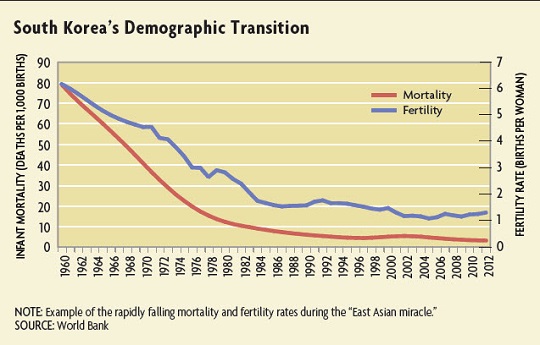

According to research by Bloom and fellow Harvard economist Jeffrey Williamson, this "demographic dividend" accounted for as much as a third of the economic growth enjoyed by a number of East Asian countries like Japan and South Korea between 1965 and 1990. During that time, the dependency ratio in East Asia fell from 0.77 to 0.48 as mortality and fertility rates both fell rapidly (see example in chart 3). Williamson estimated that a 1 percent increase in the growth rate of the working-age population is associated with a 1.46 percent increase in the growth rate of GDP per capita. Similarly, a 1 percent decrease in the growth rate of the dependent population is associated with a 1 percent increase in the growth rate of GDP per capita.