Do Net Interest Margins and Interest Rates Move Together?

Economic Brief

May 2016, No. 16-05

Many market participants assume that, as the Federal Reserve tightens monetary policy, and market rates increase in response, banks will be better off because their net interest margins will also increase. As a way to understand the origins of this expectation, in this Economic Brief we look at the relationship between the federal funds rate and the average net interest margin for U.S. banks since the mid-1980s. We find that the relationship is not as clear-cut as one might suspect.

As economists debate whether and how far the Federal Reserve should continue to raise interest rates off of their record-low levels, there seems to be at least one widely accepted premise about the impact of monetary policy normalization: as interest rates go up, so too will banks' net interest margins — an indicator of the difference between what banks bring in and what they pay out in interest. As one headline in the Financial Times declared last September, higher rates are "great news" for the banking sector and could offer "redemption." Martin Gruenberg, chairman of the Federal Deposit Insurance Corp., predicted last November that higher rates will "create opportunities for banks to increase margins and generate greater returns." According to one estimate highlighted in the International Business Times, released last September before the Fed's first 25-basis-point increase, the top five banks could reap a $10 billion windfall in one year if the federal funds rate increased by 1 percentage point.

Given how broad these claims are, one would expect that a simple plot of the average net interest margin and the fed funds rate over time would show signs of the presumed strong relationship. This Economic Brief will investigate this link based on data for the United States in the last 31 years.1 Rather than exhibiting a clear relationship, a first pass at the data suggests that the statements above miss a more complicated picture. There are, in fact, cases of rate hikes that did not see a corresponding increase in the average net interest margin, and sometimes higher rates have produced shrinking net interest margins for banks. These preliminary findings suggest that more research is needed to understand the effect of monetary tightening on system-wide bank profitability and in particular net interest margins.

The Importance of Maturity Mismatch

Due to frequent confusion between bank profits and net interest margins, it is important to review the meaning of the terms. Net interest margins are the spreads between what banks receive on their interest-earning assets and what they pay on interest-paying liabilities, divided by total interest-earning assets. Profits, by contrast, are adjusted to account for noninterest income, operational and personnel costs, as well as for effects such as losses on loans. Profits can be seen as a broader measure of a bank's financial performance, while net interest margins measure a narrower relationship describing earnings and costs based on interest rate differentials.

The pronouncements noted above reflect a widespread view that net interest margins will rise in tandem with interest rates. Historical data aside, however, there are reasons to think that this may actually not be the case. In the more traditional approach to banking, liabilities are likely to be more interest rate sensitive than assets. One main reason has to do with the difference between typical maturities of assets and liabilities, often referred to as "maturity mismatch." Some examples of bank liabilities are consumer and business deposits, which tend to have relatively short-term maturities. By contrast, bank assets — for example, business loans or consumer loans such as mortgages — often have longer-term maturities. Short-term rates track the fed funds rate more closely and are more volatile, so one would expect these yields to be the most affected by policy-driven increases in interest rates. If the policy rate increases, banks would pay out more in interest on their liabilities while the rates on their long-term loans would remain stable — effectively narrowing net interest margins.

In the 1970s and 1980s, this maturity mismatch was one important factor behind the struggles of the savings and loan (S&L) industry. A core business of S&Ls was fixed-rate mortgage loans, which have returns that do not change when short-term rates move. As interest rates increased rapidly in the early 1980s during the Fed's anti-inflation campaign, the interest rates S&Ls paid to their depositors increased fairly quickly while rates S&Ls earned on their portfolios of mortgages changed little. Instead of widening, net interest margins collapsed. This episode provides an admittedly extreme example of the fact that for the traditional banking business of maturity transformation — with its interest-sensitive liabilities and relatively interest-insensitive assets — rising interest rates can lead to declines, rather than increases, in net interest margins.

That said, modern banking organizations are a lot more complicated than the traditional view of banking suggests. Some banks have a mix of assets and liabilities that are not as easily broken down by maturities — for example, they may offer short-term consumer loans and immediately sell any mortgage loans they make; on the liability side, they may offer longer-term consumer deposits. The critical point to understand is that the maturities of assets versus liabilities is one of the main drivers of net interest margins.

The Question of Market Power

What if banks can exert some control over their net interest margins? One argument for assuming a positive relationship between rising interest rates and growing net interest margins is that banks have enough market power to affect the interest rate spread. According to this view, in an environment of rising interest rates, banks would try to hold down the returns that they offer to deposit customers (thereby keeping their own costs down) while adjusting loan rates upward to reflect market rates more closely (thereby reaping a higher yield). To the extent that banks’ depositors are fairly price insensitive, such an adjustment would not drive most of them away.

There are good reasons to think that many depositors are indeed price insensitive. In general, it takes time and effort to change banks and to research various options on banking products. Transaction costs ought to be taken into account as well. Therefore, many depositors might be inclined to reject switching and stick with a particular bank even if they could do better elsewhere. This would support the view that as the Fed raises rates, net interest margins will widen because banks will use depositors' price insensitivity to adjust the interest rate differential in their favor.

Some research supports the view of deposit "stickiness." In a 2013 paper, Federal Reserve Board of Governors economists John C. Driscoll and Ruth A. Judson analyzed ten years of bank deposit rates and customer behavior (covering two full Fed easing and tightening cycles) to see, among other things, whether and how consumers responded to rate changes. They found that the response to shifts in deposit rates differed depending on the types of accounts, but broadly speaking, depositors were generally slow to change their banking behavior following a rate increase — implying a certain degree of insensitivity to rates.2

Yet another argument supports the view that rising rates may induce higher net interest margins, this time in the context of the zero lower bound on nominal interest rates. Under normal circumstances, when rates are above the zero lower bound, banks typically target a spread between rates on assets and liabilities. If the fed funds rate approaches zero, however, banks may see this differential between loan and deposit rates become compressed, because they generally cannot pay negative interest rates on deposits. (Customers might well prefer to keep their funds in the form of cash rather than pay a bank to hold them.) In the United States, near-zero rates have been in effect since 2008, which suggests that net interest margins may well have been narrower than usual during this time because banks have not been able to push the rates they pay on deposits and other liabilities below zero. This means that as their rates on deposits effectively stay around zero, those rates are relatively closer than usual to the (higher) rates on loans. However, as the Fed pushes interest rates upward, banks may be able to return their spreads to their target levels, perhaps raising deposit rates more slowly than loan rates. Accordingly, net interest margins might widen.3

Rate Changes Across Time

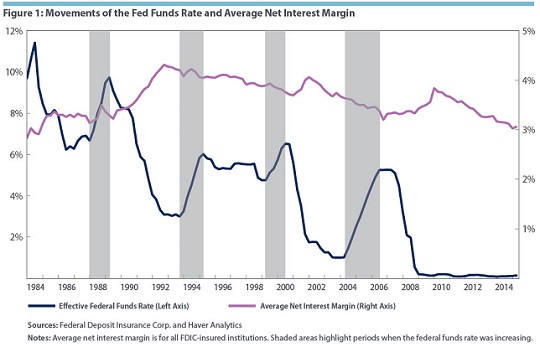

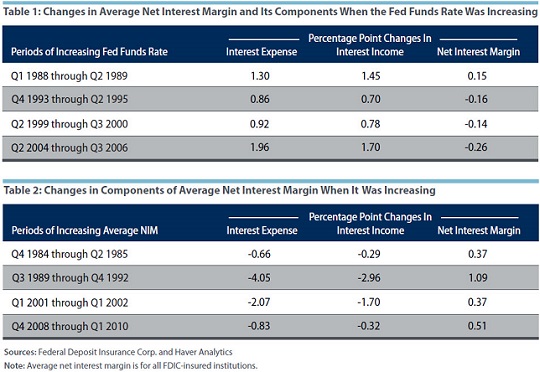

So how does the course of the fed funds rate actually compare to net interest margins over time? Figure 1 plots the effective fed funds rate and the average net interest margin for all banks from 1984, around the start of the Great Moderation, until 2015. Contrary to the quotes noted earlier, a rise in the net interest margins has generally not coincided with rate hikes (which are indicated in the chart by shading). In Table 1, the four major cases of tightening are contrasted with the concurrent change in the net interest margins. It shows that there is only one instance — the first quarter of 1988 through the second quarter of 1989 — of an increase in the fed funds rate coinciding with an increase in the average net interest margin. In that example, the rise in interest income (1.45 percentage points) exceeded the change in interest expense (1.30 percentage points).

1

The data cover all FDIC-insured U.S. depository institutions (commercial banks and savings institutions). This article uses the simpler term "banks" rather than "FDIC-insured U.S. depository institutions."

2

See John C. Driscoll and Ruth A. Judson, "Sticky Deposit Rates," Federal Reserve Board of Governors Finance and Economics Discussion Series, October 1, 2013, pp. 7, 12.

3

See Stijn Claessens, Nicholas Coleman, and Michael Donnelly, "'Low-for-Long' Interest Rates and Net Interest Margins of Banks in Advanced Foreign Economies," Federal Reserve Board of Governors International Finance Discussion Papers Notes, April 11, 2016. The authors study the behavior of net interest margins during periods of persistently low interest rates in a sample of advanced economies in the recent past. Their findings support the view that "low-for-long" interest rates tend to compress margins.

4

See Roger Aliaga-Díaz and María Pía Olivero, "The Cyclicality of Price-Cost Margins in Banking: An Empirical Analysis of its Determinants," Economic Inquiry, January 2011, vol. 49, no. 1, pp. 26–46. Another example is the IFDP paper by Claessens et al, cited above. They use a cross-section of banks located in many different countries and try to control for other changes in conditions that may influence banks’ net interest margins.

5

See also Francisco B. Covas, Marcelo Rezende, and Cindy M. Vojtech, "Why Are Net Interest Margins of Large Banks So Compressed?" Federal Reserve Board of Governors Finance and Economics Discussion Series Notes, October 5, 2015.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the following statement. Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us