When the Mortgage Becomes the Backup Plan: Debt and Disaster Insurance

Economic Brief

July 2026, No. 26-22

Key Takeaways

- Debt crowds out flood insurance, as homeowners with little equity have less to lose from default, making their mortgage an implicit backup plan that substitutes for formal coverage.

- Uninsured exposure is highest in the riskiest areas, precisely where flood damage is most likely.

- After Hurricane Harvey, uninsured homeowners defaulted three times more often than the regular default rate.

Property insurance is critical for managing natural disaster risk, particularly for homeowners whose homes are their biggest asset.1 Yet, for specific perils like flooding — one of the costliest natural hazards in the U.S. — voluntary flood insurance coverage remains strikingly low. Among mortgage holders outside federally designated high-risk zones, only about 0.5 percent carry flood insurance.2 And about 70 percent of residential flood losses each year involve uninsured homes.3

Why do so many homeowners leave their single largest asset — which accounts on average for about two-thirds of household net worth — exposed to such a risk? In my recent working paper "Limited Liability and Disaster Underinsurance" — co-authored with Laura Bakkensen, John Bailey Jones and Russell Wong — we offer an explanation rooted in the structure of the mortgage contract itself.

The Usual Suspects and What They Miss

Researchers have offered a range of explanations for low flood insurance takeup. Some homeowners may be unaware that their houses are at risk of flooding. Others assume the federal government will bail them out after a disaster. Still others face tight budgets and view insurance premiums as an expense they can defer. And behavioral biases — such as the tendency to discount low-probability events — play a role too.

Recent work has also highlighted that rising premiums and regulatory frictions are reshaping insurance availability, with some insurers exiting high-risk markets altogether.4 These explanations capture important parts of the plot, but they all treat the homeowner's mortgage as a minor character. We argue that the mortgage is, in fact, central to the story.

The Mortgage Is Already a Type of Flood Insurance

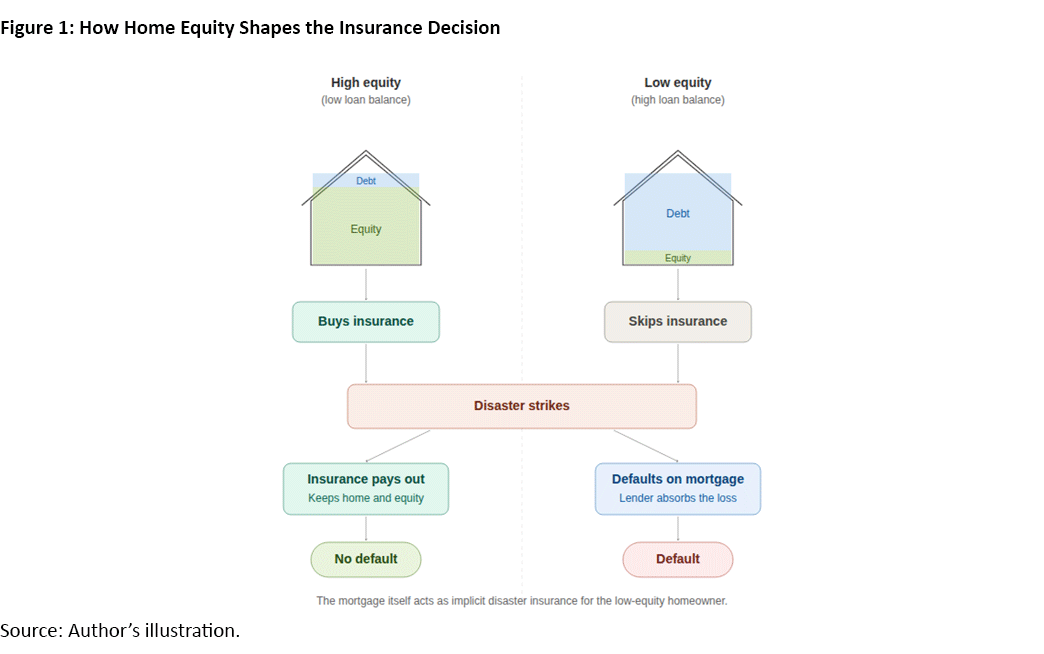

The basic insight is simple, which is that a mortgage is a limited-liability contract: If disaster strikes and homeowners can no longer afford the damaged property, they can default, surrender the home to the lender, walk away and cap their losses. The lender (not the homeowner) absorbs most of the remaining damage. However, how much protection this "implicit insurance" provides depends on how much equity the homeowner has.

High Equity/Low Loan Balance

Homeowners who have paid down most of their mortgages have significant wealth in their houses. If a flood destroys part of that value, they bear the loss directly. And defaulting would mean giving up a large amount of home equity. For these homeowners, buying flood insurance makes clear financial sense, as it protects a large stake.

Low Equity/High Loan Balance

Homeowners who have barely paid down the loan have little personal wealth at risk in the house, as most of the home's value belongs, in effect, to the lender. If a flood hits, they can default and walk away at relatively low cost. Thus, the mortgage itself cushions the blow, and paying for a separate flood insurance policy on top of that is, from their perspective, redundant.

Incentives and Insurance

This logic flips a familiar intuition on its head. We usually think that people facing greater risk should save more and insure more. But under a limited liability contract, homeowners who are deeply in debt actually have less incentive to insure, because the debt contract is already doing part of the job.

The figure below summarizes the mechanism. Two homeowners face the same flood. In the absence of insurance, they would lose their home equity (green shading) but pass on the value of the mortgage (blue shading) to the mortgage lender. Facing higher losses, homeowners with high equity buy insurance and keep their homes. Ones with low equity skip insurance and, if disaster strikes, default instead.

What the Data Show: Leverage Crowds Out Flood Insurance

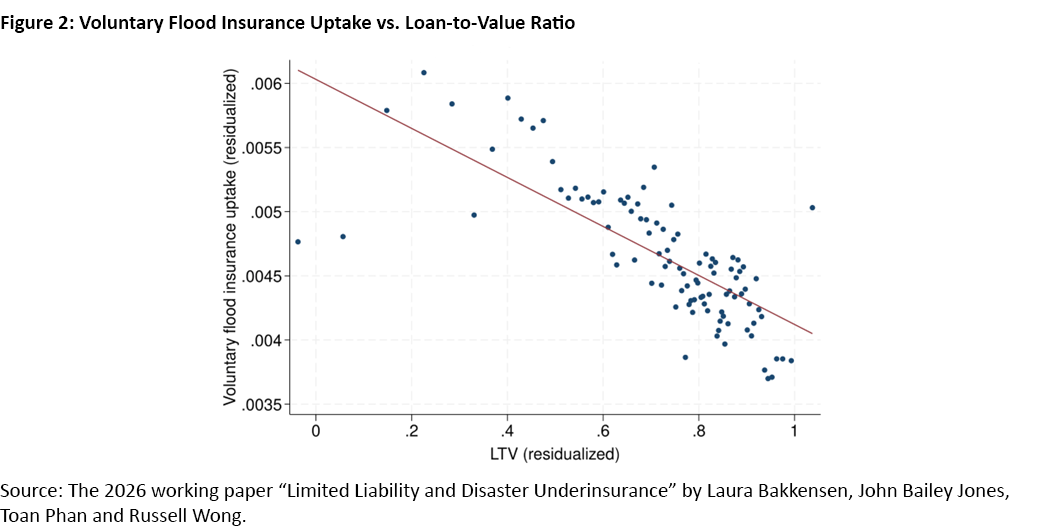

We test this prediction using a proprietary dataset from International Exchange (ICE) McDash, which tracks the servicing portfolios of the largest U.S. residential mortgage servicers. The dataset links tens of millions of loan-month observations to property-level insurance records, allowing us to observe whether each borrower holds flood coverage alongside variables such as loan balance, home value and credit score. We restrict the sample to areas where flood insurance is voluntary (thus, outside the Federal Emergency Management Agency's Special Flood Hazard Areas) and where flood risk is nontrivial (as measured by the First Street Flood Factor).5

Figure 2 plots the relationship between voluntary flood insurance uptake and homeowners' loan-to-value (LTV) ratios after controlling for borrower credit scores, home values and local conditions. The relationship is clear: As the LTV ratio rises — meaning the borrower has less equity — the probability of carrying voluntary flood insurance falls. Going from a fully paid-off home to a loan equal to the full property value roughly halves insurance take-up, which is already relatively low, as noted earlier.

A natural concern is that this pattern could reflect something other than leverage itself. Perhaps households that are more careful or forward-looking both pay down mortgages faster and buy more insurance. To isolate the effect of leverage alone, we use the remaining maturity of the loan as an instrumental variable.6 Remaining maturity captures variation in leverage that comes purely from the ticking of the clock, not from unobserved differences in how cautious or wealthy the borrower is. When we use this approach, the negative relationship between leverage and insurance gets stronger (not weaker), roughly doubling in magnitude.

Where the Pattern Is Strongest

Our model predicts that the crowd-out effect should be amplified or dampened by features of the environment that change the cost of default relative to the cost of going uninsured. The data support this in two ways.

Higher Flood Risk, More Insurance

In ZIP codes with higher flood-risk scores, insurance uptake is greater, holding leverage constant. Homeowners do respond to risk, but the crowd-out from debt is still present and, if anything, stronger in riskier areas. This means that insurance is being forgone precisely where flood damage is most likely.

Recourse States, More Insurance

In some states, lenders can pursue borrowers' nonhousing assets — such as savings and wages — after a foreclosure if the sale of the home does not cover the outstanding debt. In these "recourse" states, the costs homeowners bear when they default are not capped by the value of the house. This reduces the implicit insurance embedded in their mortgages, making the households more likely to buy formal coverage. Consistent with this prediction, we find significantly higher flood insurance uptake in recourse states.

Hurricane Harvey: the Default Channel in Action

If uninsured, highly leveraged borrowers really are relying on default as their backup plan, we should see that plan activated when disaster strikes. Hurricane Harvey provides a powerful test.

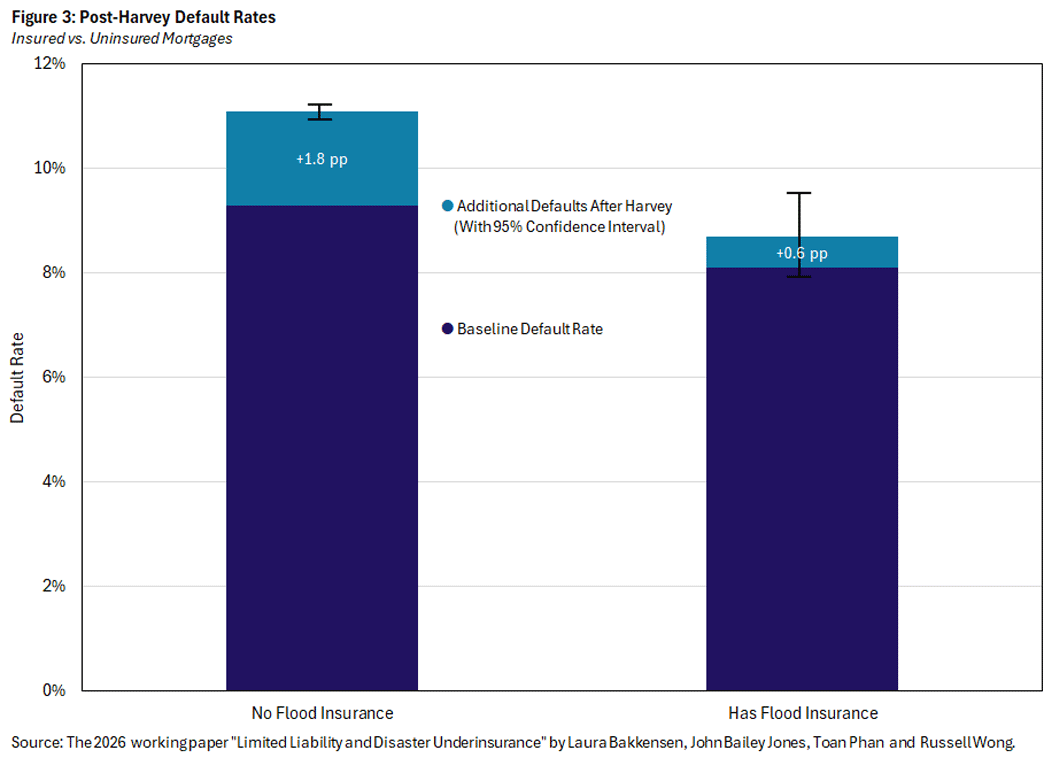

Harvey made landfall in Texas in August 2017, stalled over the Houston metro area for several days and produced some of the heaviest rainfall from a tropical cyclone in U.S. history. Total damages reached an estimated $125 billion, driven overwhelmingly by flooding. Yet, flood insurance penetration in Houston was just 7 percent.7

Using over 21.5 million loan-month observations across Texas from 2015 to 2019, we compare default rates before and after Harvey in heavily affected ZIP codes versus the rest of the state. We also separate borrowers with and without flood insurance. Figure 3 below summarizes the results.

Among uninsured mortgages in affected areas, the default rate rose from a 9.3 percent baseline to 11.1 percent. For insured mortgages, the increase was just 0.6 percentage points. Put differently, borrowers without flood insurance experienced roughly three times the increase in default after the storm.

This supports the model's central prediction: When formal coverage is absent, leveraged homeowners turn to default as a substitute form of disaster protection. The losses do not vanish but instead shift from the homeowner to the lender.

Why It Matters

These findings reframe the puzzle of low flood insurance take-up. It is not just a story of behavioral biases, risk misperception or tight household budgets. There is a structural, strategic dimension: The type of the mortgage contract itself shapes whether homeowners choose to insure. This observation connects to broader concerns about the resilience of insurance markets in a changing environment.

If default is functioning as de facto disaster insurance, then the mortgage market absorbs flood losses that formal insurance was designed to cover. Those losses show up on lender balance sheets, in the portfolios of government-sponsored enterprises like Fannie Mae and Freddie Mac,8 and ultimately in the risk profile of the broader financial system. Understanding this channel is essential for anyone thinking about how disaster risk flows through housing and financial markets.

As flood risk intensifies, a substantial share of the U.S. housing stock may remain both highly leveraged and uninsured. This combination concentrates disaster losses in the mortgage market rather than spreading them through the insurance system. The structure of debt contracts, disaster relief and insurance programs will jointly determine where these risks ultimately reside: households, insurers, lenders or taxpayers.

Toan Phan is a senior economist and research advisor in the Research Department at the Federal Reserve Bank of Richmond.

1

The 2025 working paper "Perspectives on Insurance and Climate Risk" by Parinitha Sastry and Ishita Sen provides a comprehensive review of the property insurance literature and its connections to household finance and mortgage markets.

2

According to the calculations in my recent working paper "Limited Liability and Disaster Underinsurance," co-authored with Laura Bakkensen, John Bailey Jones and Russell Wong. Flood insurance is mandatory only for properties with federally regulated mortgages in the Federal Emergency Management Agency's Special Flood Hazard Areas, which amounts to less than 5 percent of all residential properties. The 2021 paper "Voluntary Purchases and Adverse Selection in the Market for Flood Insurance" by Jacob Bradt, Carolyn Kousky and Oliver Wing estimates that only about 2 percent of households outside of FEMA's Special Flood Hazard Areas purchase flood coverage. Among mortgage holders in our sample, the rate is about 0.5 percent.

3

The 2025 paper "Measuring Flood Underinsurance in the USA" by Natee Amornsiripanitch, Siddhartha Biswas, John Orellana-Li and David Zink estimates that 70 percent of total annual flood losses across single-family residences are uninsured.

4

See the review in the previously cited working paper "Perspectives on Insurance and Climate Risk."

5

The First Street Flood Factor is a projection of cumulative flooding probability from 2020 to 2050, scored from 1 (minimal) to 10 (extreme). Nontrivial here means a flood factor of at least 2.

6

Remaining maturity is the number of months left until the loan matures. For a fixed-rate fully amortizing mortgage, the remaining balance at any point is a deterministic function of the original loan terms and the remaining maturity.

7

CoreLogic estimated that roughly 70 percent of residential flood damage from Hurricane Harvey was uninsured, with flood insurance take-up of just 7 percent in Houston. See the 2017 article "Visualizing Hurricane Harvey's Impact on Houston's Neighborhoods" by Sarah Strochak and Bhargavi Ganesh.

8

Government-sponsored enterprise loans typically qualify for federal disaster forbearance, which allows borrowers to pause payments after a declared disaster.

To cite this Economic Brief, please use the following format: Phan, Toan. (July 2026) "When the Mortgage Becomes the Backup Plan: Debt and Disaster Insurance." Federal Reserve Bank of Richmond Economic Brief, No. 26-22.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us