This article is an early release from the upcoming Third Quarter issue of 2026.

Want to be notified when the magazine goes live? Subscribe to receive email alerts for Econ Focus.

This article is an early release from the upcoming Third Quarter issue of 2026.

Want to be notified when the magazine goes live? Subscribe to receive email alerts for Econ Focus.

Before the First Bank of the United States, another, less well-known institution helped the fledgling United States find its financial footing.

John Trumbull's "Surrender of Lord Cornwallis" is one of eight paintings depicting significant moments in American history hanging in the Capitol rotunda in Washington, D.C. It portrays the Oct. 19, 1781, surrender of British troops at Yorktown, Va., after the final battle of the Revolutionary War. While the foreground holds the action, the background is dominated by billowing black smoke from the charred, war-ravaged landscape. It's hard to know if Trumbull intended any deeper meaning, but there's no denying that the war's destruction clouded the future of the newly independent United States.

The nascent country's financial situation was a major source of uncertainty. The weak and decentralized federal government created under the 1777 Articles of Confederation, along with the states, carried a debt burden of at least $70 million, owed to domestic lenders, as well as Dutch banks and the French and Spanish governments. To put the debt in context, the colonial GDP prior to the war was about $170 million. After five years of war, that number was undoubtedly much lower, possibly making the new country's cumulative debt equal to a significant portion of its annual economic output.

To make matters more complex, the U.S. currency was all but worthless thanks to the Second Continental Congress' decision to finance the war by just printing money without the necessary gold or silver specie to back it (giving rise to the expression that items of little or no value were "not worth a Continental"). The Continental dollar, which originally was issued with an exact redemption date, had evolved into nothing more than an unfulfilled IOU — a zero-interest bearer bond with a promise that it could eventually be redeemed for specie at some point in the future. This created the thorny question of whether debts owed in paper money should be repaid at their depreciated market value or at face value. The matter wouldn't be resolved until much later in 1790 in a delicate compromise among Alexander Hamilton, Thomas Jefferson, and James Madison that resulted in the establishment of Washington, D.C. (See "A Capital Compromise," Econ Focus, First Quarter 2019.)

Hamilton was far from the first to recognize the value of credit in wartime, as the Roman statesman Cicero famously declared more than two millennia ago that "the sinews of war [are] unlimited money." Given the ceiling on taxation (no one would have incentive to produce anything if they were taxed at 100 percent) and the calamitous inflation that can accompany the overprinting of money relative to the specie backing it, governments had long turned to debt to finance these efforts.

"After 1500, as the means of successful warfare became more and more expensive, the rulers of most European states spent much of their time raising money," noted political scientist, sociologist, and historian Charles Tilly in his book Coercion, Capital, and European States, A.D. 990-1992. "[Since] few large states have ever been able to pay for their military expenditures out of current revenues ... they have coped with the shortfall by one form of borrowing or another."

A national bank facilitated a government's ability to borrow cheaply by acting as the sole purchaser of its debt, which it could then sell through a centralized bond market. This meant the bank could apply pressure on the government to honor its debts by refusing to lend further money should it default. The Bank of England, the second-oldest central bank after Sweden's Riksbank, functioned according to this logic. Barry Weingast, an economist and political scientist at Stanford University, argued in a 1997 book chapter, "By centralizing the loan decisions in a single intermediary rather than among a large, diffuse community of agents, the bank's charter allowed it to enforce a community credit boycott."

Governments without such banks were usually still able to borrow, but they were often viewed as riskier investments, presumably because they lacked the commitment mechanism described above. There is empirical evidence to support the value of a national bank when it comes to borrowing: Paul Poast, a political scientist at the University of Chicago, found in a 2015 International Organization article that during the 19th and early 20th centuries, countries with national or central banks had lower wartime borrowing costs than those that did not.

Hamilton was committed to the idea of a national bank well before the end of the war. The 1781 letter to Morris was one in a series of essays in which he called for the United States to adopt such an institution to act as the country's fiscal agent, supplying funding to the government, handling its accounts, and managing its debt. (These were common functions for central banks during the period before World War I; since then, central banks have focused more on monetary policy rather than managing a state's fiscal affairs.)

The national bank would also put forward a new, stable currency, as the Continental dollar had fallen to below one-eighth of its original value by the end of 1779 and would fall further still. Through prudent financial administration, Hamilton believed it would be able to pay off any war debt in just a few decades, making it "a national blessing ... [a] powerfull [sic] cement of our union."

All this meant Morris was under tremendous pressure when he was elected superintendent of finance by the Congress in February 1781. George Washington summarized the difficulties that lay ahead: "I have great expectations from the appointment of Mr. Morris; but they are not unreasonable ones, for I do not suppose that by any magic art he can do more than recover us by degrees from the labyrinth into which our finances are plunged."

Lawrence Lewis, the 19th century historian, echoed many of Morris' contemporaries, who saw him as the natural choice to take on the responsibilities of the office: "Full of energy and self-reliance, he was, perhaps, by his business talents and mercantile experience, better qualified than any man in America to control and direct its financial affairs."

Hamilton urged Morris to move quickly in establishing a national bank, which he believed should have at least $3 million in capital to get started. Morris agreed a bank was needed but believed such a sum was too large.

Morris submitted his plan to Congress on May 17, 1781. He called for the bank to raise $400,000 with shares costing $400 each, payable in gold or silver specie. Subscribers with at least five shares would pay half of what they owed at the time of purchase and the rest within three months. The bank would have 12 directors who were not paid unless authorized by the shareholders, and the bank's president would be chosen from among those directors. Morris, as superintendent, would get daily reports, except for Sundays, on the accounts. Bank notes, issued as government wages or paid out to merchants who brought promissory notes or bills of exchange to the bank, could be redeemed for specie on demand. To facilitate their nationwide use, they could be used to pay all taxes in every state.

The plan was quickly, but not unanimously, approved by Congress, with James Madison arguing that creating such an institution exceeded Congress' authority. He was outnumbered, however, and the plan was approved in late May.

The bank began organizing itself shortly after. It would take some time to get a meaningful number of domestic subscriptions, as many potential lenders doubted the bank would succeed and feared losing their fortunes. But by the fall of that year, the list began to grow, and by 1782, it was gathering the necessary capital. William Bingham, thought to be the richest man in America after the Revolutionary War, bought 9.5 percent of the available shares.

Morris also used around $470,000 in silver invested from France to fund the bank, which then lent that money to Congress. It is unclear whether Morris had the authority to make that transaction, as the money may have been intended for Congress directly. Also unclear is whether some of that amount went toward Morris' rumored purchase of 63.3 percent of the bank's shares — about $254,000 — on behalf of the government, as several sources suggest the transaction was made possible by French and Dutch loans.

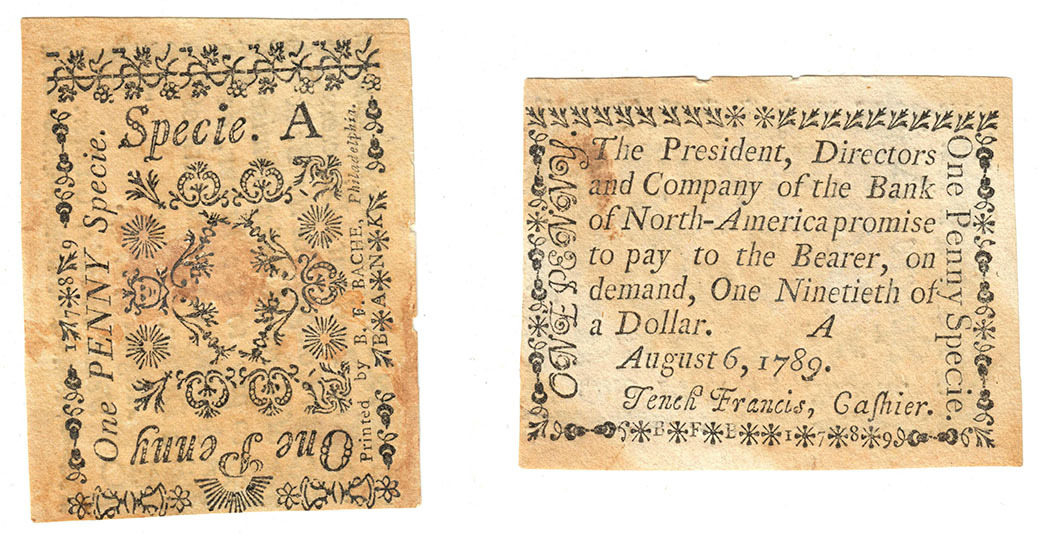

By the end of the year, the shareholders felt they had sufficient capital to begin operations, and Congress granted the Bank of North America its charter on Dec. 31, 1781. The shareholders elected Morris' business partner, Thomas Willing, as president of the bank. (Willing would also serve as the first president of the First Bank of the United States a decade later.) The bank opened its doors on Jan. 7, 1782, at 307 Chestnut Street in Philadelphia.

In the first half of 1782, Morris' complex role as both the government's superintendent of finance and the manager of the government's investment in the bank caused some unease. Because Morris bought over 63 percent of the original shares on behalf of the government and the bank charged interest on its loans to the government, Lewis noted that "what [Morris] thus paid in with one hand he may be said to have drawn out with the other," meaning that the government would make money from money it had lent itself. Bank officers were unsurprisingly uncomfortable with this arrangement, and Morris sold the government's stock throughout 1783, most of it directly to the bank as well as to Dutch financiers. At this point, it became a strictly private institution, as the government no longer held any shares. (This granting of access to bank assets by international actors, but not necessarily domestic ones, would also be a source of grievance when Pennsylvania revoked its charter in 1785.)

During this time, the bank performed its key operations, allowing the nation to begin finding its financial footing. Most importantly, it extended short-term loans to the federal government (as well as to Pennsylvania's) for payroll, supply contracts, and debt servicing. It even loaned Philadelphia money to light the city's streets and feed its citizens who could not afford food. These governments could then repay the bank whenever they received revenue, which allowed them greater flexibility and the chance to avoid default. Morris believed that the bank's lending practices to the government were worthwhile, as it meant "the army was in every point on a much more respectable footing than formerly."

The circulation of a stable national currency also brought confidence to the new country's financial system. The national government and the states could all conduct transactions, including taxation, without the frictions that came with the different actors having to determine the value of competing and overlapping currencies.

Despite its successes, the Bank of North America remained dogged by critics. The bank kept bank notes mostly stable relative to specie, but in Pennsylvania, its tight control over lending and the money supply led to accusations of malicious intent. Britain also flooded the market with its goods at the war's end, which led much of the specie that had accumulated to leave the country. This meant money was scarce, and lenders charged a premium.

These realities only gave further fodder to the bank's organized opposition, comprised mostly of those with a negative view of a strong central government and banking system. Characterizing the bank as the root of most economic problems, they accused it of favoritism, extortion, and undue commercial and political influence. They also argued it engaged in systematic usury, leading many borrowers to financial ruin, while high dividends of 14 percent only further separated its wealthy stockholders from the general population. Those opponents petitioned Pennsylvania to revoke its charter in March 1785, with the assembly ultimately revoking the charter that September.

Despite these criticisms, the bank's Pennsylvania charter was reissued in 1787, but it was much narrower: The bank would need to be rechartered after 14 years, it could no longer hold property (except in a very narrow set of circumstances necessary for conducting its business), and its capital was capped at $2 million. Its national charter, on the other hand, would become void when the body that issued it — the Confederation Congress — was replaced by the new U.S. Congress in 1789. Along with the First Bank of the United States and the Bank of New York (founded in 1784), the Bank of North America's shares would be the first traded on the New York Stock Exchange.

The bank would keep its Pennsylvania charter until 1864 and remain in existence under its original name in some form until 1929, when, operating as the Bank of North America and Trust Company, it merged with the Pennsylvania Company for Insurances on Lives and Granting Annuities. That company was bought and sold several times, most recently by Wells Fargo in 2008.

Morris, however, would struggle. He became heavily involved in land speculation, but it was a boom-and-bust industry, and he racked up significant debt, eventually losing everything. He spent three and a half years in a debtors' prison and was destitute when he died in May 1806.

While Hamilton would ultimately receive much of the credit for righting the nation's finances, he viewed Morris' brainchild, the Bank of North America, as a pivotal step along that journey. It funded the fledgling Philadelphia-based government, serving as a credible agent of the government's finances while giving domestic and foreign investors the confidence to lend. And it provided the stable, specie-backed currency that the country needed. Perhaps it wasn't hyperbole when, in the same letter arguing that credit was a key to victory, he let Morris know just how crucial his project would be: "You may render America and the world no less a service than the establishment of American independence!"

Lewis, Jr., Lawrence. A History of the Bank of North America. Philadephia, P.A.: J.B. Lippincott & Co., 1882.

Moulton, R.K. Legislative and Documentary History of the Banks of the United States. New York, N.Y., 1834.

Poast, Paul. "Central Banks at War." International Organization, Winter 2015, vol. 69, no. 1, pp. 63-95.

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

This department of Econ Focus recounts milestones in history that have shaped the economy of the Fifth District and the nation.