Al Broaddus, Productivity Growth and Monetary Policy in the 1990s

Economic Brief

May 2026, No. 26-15

Key Takeaways

- Former Richmond Fed President Al Broaddus made important contributions to FOMC discussions in the late 1990s.

- Broaddus argued that a sustained increase in productivity growth required an increase in real interest rates.

- With the possibility that artificial intelligence may raise trend productivity growth, this history from the late 1990s has renewed relevance today.

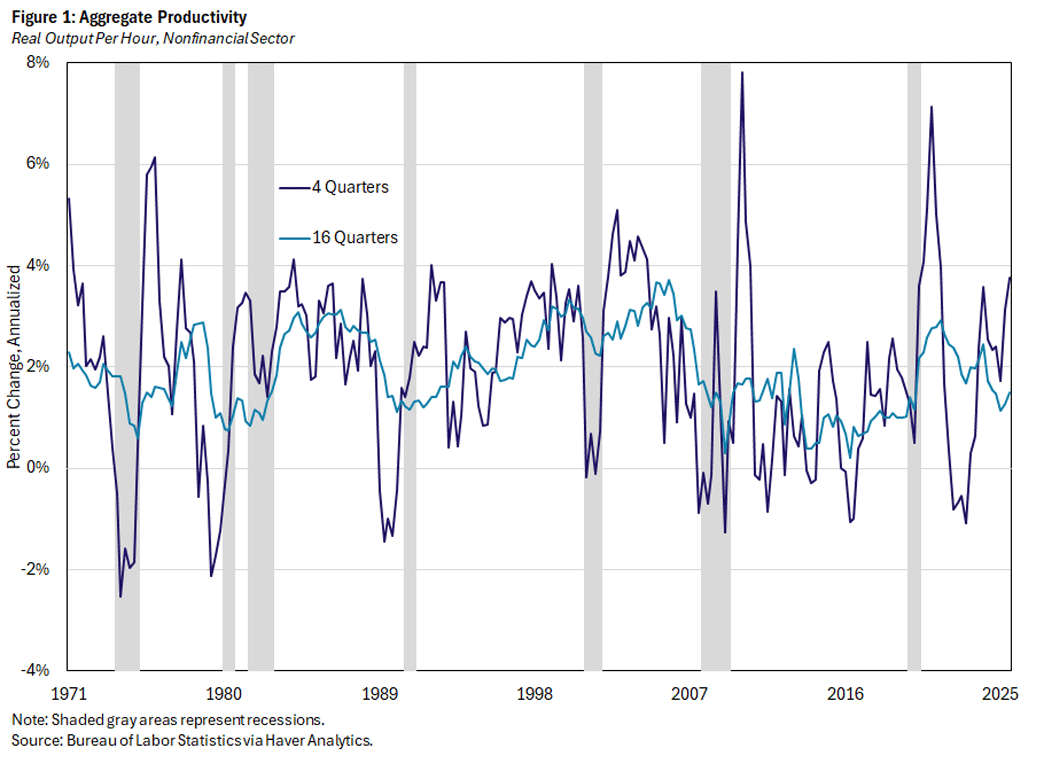

Over the last two years, there has been a notable increase in U.S. productivity growth. For example, in the third quarter of 2025 (the most recent quarter for which data is available), the four-quarter growth rate of real output per hour in the nonfinancial corporate sector was 3.8 percent. That is more than twice the 1.8 percent average rate at which output per hour grew over the last 25 years. Many analysts have linked this increase in productivity growth to advances in artificial intelligence (AI), and there is an active debate about whether this higher productivity growth will continue.

The high productivity growth of the late 1990s often comes up in this debate. Then-Federal Reserve Chair Alan Greenspan's views about the implications of productivity growth for monetary policy were widely publicized during that time. Less well known are the contributions that the late Al Broaddus — then-president of the Richmond Fed — made to Federal Open Market Committee (FOMC) discussions about these issues. Broaddus' recent passing makes this an especially appropriate time to advertise those contributions to a wider audience. I'll begin by giving an overview, then provide a chronological tour through his contributions.

Setting the Stage

What are the implications for monetary policy of a sustained increase in productivity growth? This question took center stage in the late '90s, as evidence accumulated that the rate of productivity growth had increased. At that time, the higher observed productivity growth coincided with a period of unusually rapid technological advancement related to the internet and the telecommunications industry more broadly.1

Figure 1 shows the growth in real output per hour in the nonfinancial corporate sector, which serves as a measure of aggregate productivity. From 1971 through 1995, the annualized growth rate was 1.9 percent, but that growth rate rose to 3.1 percent in the following four years.

While there had been other years of similarly high productivity growth since 1971, they had occurred in the wake of recessions, when productivity growth is often at a cyclical peak. The 1996-99 period was late in an expansion, when productivity growth often tails off.

Economic theory suggests at least two ways in which higher productivity growth may be relevant for monetary policy. First, suppose the higher productivity growth happens unexpectedly and is reflected quickly in higher output growth (and importantly, in higher levels of output than had been expected). This scenario can be relevant for policy in two related ways:

- If a central bank is basing policy partly on estimates of the output gap, it runs a risk of short-term policy that is too tight. The level of output is observed, but potential output must be estimated. If the policymakers do not incorporate higher productivity growth into their estimates of potential output, they will mistakenly attribute high growth to overheating and pursue excessively tight monetary policy.

- Turning to inflation, higher productivity growth can lead to lower inflation rates in the short run: Firms see their costs rising more slowly and respond by raising prices more slowly.

Second, an increase in the trend productivity growth rate would be expected to carry with it higher trend growth rates of output and consumption. It is a robust prediction of economic theory that higher trend consumption growth would in turn be associated with higher real interest rates. Assuming that monetary policy has an unchanged inflation target, higher real interest rates would then require higher nominal interest rates. That is, monetary policy would eventually need to respond to higher productivity growth with higher nominal interest rates.

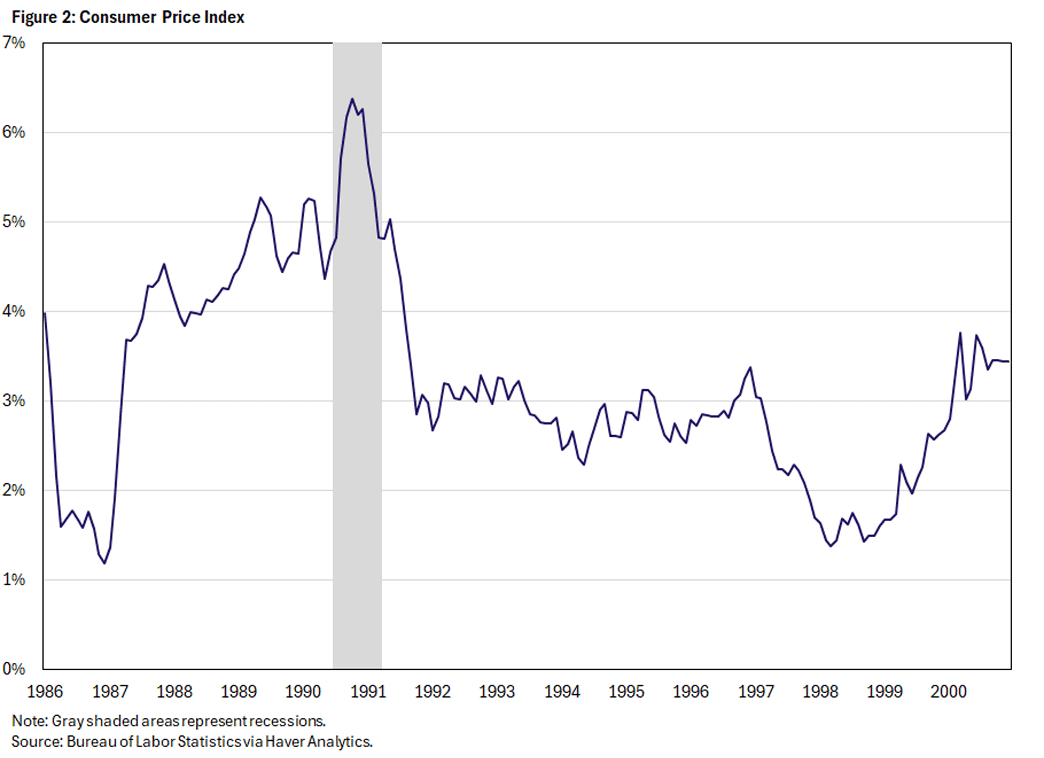

In the late '90s, Greenspan famously emphasized the first set of factors. He inferred that a sustained increase in productivity growth was occurring and used that as a basis to both help explain the low inflation numbers at the time (as seen in Figure 2)2 and — to a lesser extent —argue against tightening monetary policy.

In contrast, Broaddus emphasized the second set of factors. The analytical framework he used — relating consumption growth to real interest rates — dates back to Irving Fisher's 1930 book Theory of Interest. This framework was a central element of the real business cycle (RBC) theory that came to prominence in macroeconomics while Broaddus was research director at the Richmond Fed in the late 1980s and early 1990s. And then, when Broaddus became president of the Richmond Fed, those same ideas were incorporated into extensions of RBC theory that could be applied to the study of monetary policy.

Economists and consultants at the Richmond Fed were important contributors to this literature, so it was natural for Broaddus to be the leading voice in bringing these ideas to the FOMC. A notable example from the academic literature is the 1997 article "The New Neoclassical Synthesis and the Role of Monetary Policy" by Richmond Fed economist Marvin Goodfriend and consultant Robert King. Goodfriend and King wrote,

Recently, a possible pickup in productivity growth has been cited as a reason why the Federal Reserve need not raise short-term real interest rates to maintain low inflation. In fact, the standard RBC component of the [New Neoclassical Synthesis] model suggests, at a minimum, that real rates would have to rise one for one with an increase in trend productivity growth, e.g., a 50-basis-point increase in the growth rate would be matched by a 50-basis-point increase in real interest rates. Importantly, rates would have to rise even if the economy were otherwise operating at a noninflationary potential level of GDP.

Broaddus would echo and elaborate on these points at FOMC meetings from May 1997 through June 1999.

Broaddus and the FOMC: 1996-99

The following is an overview of FOMC discussions regarding productivity growth and monetary policy during this period, with special attention to Broaddus’s contributions. In addition, I include a couple of excerpts concerning related issues that remain highly relevant.

September 1996 to May 1997: Introducing the Ideas

Perhaps the first time that Greenspan raised the possibility of an increase in productivity growth (along with the connection to inflation) was the September 1996 FOMC meeting. The real economy seemed to be strong, with the unemployment rate falling and inflation stable at what was then considered a low level. At that time, Greenspan viewed the high productivity growth as unmeasured:

...how to explain the extraordinary behavior of prices when wage increases are very clearly accelerating. The answer is that we can explain it only if productivity is indeed rising a lot faster than our statistics indicate.3

In March 1997, the FOMC raised its short-term interest rate target to 5.5 percent, after more than a year at 5.25 percent. According to the minutes of the FOMC meeting, the committee "saw a clear need for a preemptive policy action that would head off any pickup of inflation, and it was noted that a shift to a tighter policy stance would seem to pose little risk to the expansion."4

By the spring of 1997, higher productivity growth was starting to be observed, and the possibility that it could continue seemed real. At the May 1997 FOMC meeting, Broaddus spelled out in detail the link between productivity growth and real interest rates, and then to monetary policy:

Let us suppose that markets are confident that the Fed will conduct policy so as to hold the CPI increase to a rate of 3 percent this year and that inflation expectations are anchored at 2 percent — that that is not an issue. Let us assume in that environment that the productivity trend increases. What does that do to financial markets and specifically to real interest rates? Broadly speaking, the improved productivity trend is going to cause firms to expect higher future earnings and workers to expect higher future wages. The point that needs to be emphasized in this situation is that, at the existing level of real interest rates, businesses and households are going to want to bring some of that expected future income into the present. Workers may want to fix up their houses; business firms may want to invest in new plant and equipment; and they will try to do this by borrowing against expected future increases in income. But, of course, the economy does not have the future income and output yet so real interest rates have to rise in order to restrain this new demand for credit. In effect, the higher real rates raise the price of current consumption in terms of future consumption foregone so that firms and households will be content to wait until the economy actually has the output in hand before they try to consume it. The point of the story is — and this is the bottom line — that even if the productivity trend turns out to be higher than the staff is assuming, which would remove some of the inflationary risk stemming from the labor markets, real interest rates would still need to rise to prevent a further credit-driven increase in aggregate demand.5

Even while arguing for an increase in interest rates, Broaddus acknowledges Greenspan's point that higher productivity growth may push down inflation in the short run. Separately, it is notable that Broaddus refers to inflation expectations being anchored at 2 percent, as this was 15 years before the Fed formally established its 2 percent inflation target. In fact, Broaddus was an early and outspoken advocate for a formal inflation target.6

July 1997: Reiterating and Explaining Why Rates Need to Move

At the next FOMC meeting, Broaddus pointed to the behavior of investment as support for both the possibility of a sustained increase in productivity growth and the need for higher real interest rates. Equipment investment had been growing rapidly since 1993, and nonresidential structures investment followed suit in 1996 and early 1997: Over the four quarters ending with the first quarter of 1997, real equipment investment had grown at a 10.5 percent rate, and real nonresidential structures investment had grown at a 9.6 percent rate. Structures had grown at just an annual rate of 2.7 percent over the prior four years.

The economy seems to be experiencing something that is at least approaching an investment boom. While I think the staff is right to be cautious about concluding in any definite way that the longer-run trend growth in productivity has increased, there is certainly a possibility that we may be looking at a moderate increase. As I said at the last meeting, either of those events would imply a need for higher real interest rates. With inflation expectations basically stable, a moderate increase in the nominal funds rate would give us a moderate increase in real interest rates.7

At the same meeting, Broaddus made a more general related point about the need for nominal interest rates to move around over time in a regime where monetary policy successfully anchors inflation expectations. We now would call this a successful inflation targeting regime.

In this situation, I think it is very important that we make every effort to do a better job of explaining to the public how we expect the funds rate that we target, and for that matter other short-term interest rates, to behave in the current regime and why. Specifically, I think we need to make the point that in the current environment, where actual inflation is low and our anti-inflationary credibility is relatively high, though maybe not perfect, short-term nominal interest rates are essentially short-term real interest rates, and short-term real rates routinely will have to move up and down in order to clear credit markets.8

The case of a sustained increase in productivity growth is one example of how the nominal interest rate needs to move to keep inflation stable and the economy operating at potential. But as Broaddus emphasized, there is a far more general principle: Stability of inflation and inflation expectations does not imply stability of nominal interest rates. In fact, it requires nominal interest rates to move around so that real interest rates can move appropriately.

May 1998: Humility but Sticking to His Guns

It would be almost a year before Broaddus returned to the issue of productivity growth and real rates. In the meantime, he had been arguing for tighter policy, dissenting at the November and December 1997 FOMC meetings when he was a voting member. During this period, he had been predicting higher inflation, and that had not come to pass.

At the May 1998 FOMC meeting, Broaddus acknowledged that his inflation prediction had been off, but he explained that he continued to see significant upside risk to inflation. He reiterated his basic argument about real interest rates, but this time incorporating the term structure. According to Broaddus, the market was pushing up the longer-term real rate, but the Fed was holding down the short-term real rate, exacerbating inflation risks:

...If permanent productivity gains are in fact driving the expansion at this stage, one would expect on general economic grounds to see higher real interest rates as consumers borrow against expected future income gains and firms borrow to take advantage of favorable investment opportunities. Sure enough, real interest rates are rising, and they already are relatively high. That then raises the key question in this analysis. Is it possible that our policy stance is still inflationary even though real interest rates are at a relatively high level? I think it's possible. First, if technological innovations have raised the marginal product of capital, and I believe many would agree that they have, then firms naturally would be willing to borrow at high real rates to finance acquisitions of new capital. But as the investment boom progresses, one would expect the capital deepening to cause the marginal return to capital to decline over time. That in turn would be consistent with the pattern of real interest rates where current short real rates are above expected future short real rates, resulting in a downward sloping real yield curve. The fact that the actual real yield curve now is basically flat at least raises the possibility, even though real rates are high, that with monetary policy we are holding current short real rates below the level they are trying to reach.9

March 1999: Situation Becoming More Urgent

In late 1998, following the Russian debt crisis and the near collapse of the hedge fund Long-Term Capital Management (LTCM), the Fed lowered its target for the fed funds rate by 75 basis points to 4.75 percent. By the March 1999 FOMC meeting, it was becoming clear that the U.S. economy had weathered the LTCM storm and that it might soon be appropriate to tighten policy. The consensus on the FOMC was that it was not yet time to even indicate a bias toward tightening, but Broaddus pushed against this view:

We are looking at an acceleration of productivity in this country. If that is true, that implies an increase in real interest rates. That is not antigrowth; that is just the way the macro economy works, as I understand it. And I worry that if we fail to validate that increase, we risk over-stimulating the economy and eventually producing inflation.10

May 1999: Doubling Down

When the FOMC met at its next meeting less than two months later, even Greenspan was sympathetic to the view that policy was too loose. He commented,

... I can't get away from the fact that the growth in aggregate demand still exceeds the rate of increase in productivity and is continuing to put pressure on the system. ... It is hard to avoid the conclusion that there is an increasing imbalance here that we have to address. While I am not ready to move rates, I do think that those of you who have raised the issue of moving to a tilt toward restraint have the arguments strongly on your side.11

For Broaddus, a bias toward tightening did not go far enough. He viewed the high current demand growth — an economy that looked like it was overheating — as indicating that short-term real interest rates were being held below the level required by the presumed increase in trend productivity growth:

Mr. Chairman, what you are proposing is certainly a step in the right direction, but my preference would be to go ahead and move the funds rate up ¼ percentage point today. ... As I have said at some earlier meetings, I believe there has been a case for tightening our policy for some time now on a lot of different grounds. We have talked a lot about productivity trends at this meeting. To me it seems increasingly likely that trend productivity growth is rising. Some may see that as a reason to stand pat on policy, but higher trend productivity growth will lead at least some households and businesses to expect higher incomes in the future. Some are going to try to act on that expectation now by borrowing to increase their spending even though the actual increase in output is not yet available. In that situation, interest rates need to rise to keep demand from becoming excessive.

... as Governor Meyer mentioned earlier, when we last reduced the funds rate in November, I believe a lot of people around this table saw that move as extra insurance, so to speak, against the possibility that the financial difficulties we had experienced would undermine the general economy. Those fears clearly have not materialized, so I think there is a case for taking back that last rate reduction.12

June 1999: Coming Back to the Need for Rates to Move

At the June 1999 FOMC meeting, the committee voted to increase rates 25 basis points, with just one dissent. There would be further increases in five of the next seven meetings for a combined increase in the fed funds rate target of 175 basis points.

To some extent then, Broaddus no longer needed to argue that higher productivity growth called for higher real interest rates. However, at the June meeting, he came back to the general point he had raised in July 1997: Nominal interest rates would need to move around in what we would now call a successful inflation targeting regime. He further linked this point to a critique of simple Taylor rules, which only prescribed rate movements if there were gaps:

Finally, I'd like to point out a deficiency in the Taylor rule as I see it; I think it is fundamentally the one identified in the Orphanides paper. And that is that the rule suggests that we only need to move the real funds rate away from a fixed constant, given by the historical average, if in fact an output gap or an inflation gap arises. But as Larry Meyer suggested earlier, even if these gaps were zero, macroeconomic developments can make it necessary for real short rates to move and for us to follow and accommodate those rate changes. An example, one Larry cited earlier — and I've made this point in some previous meetings — is that an increase in trend productivity growth means that real short rates need to rise. Just to repeat, the reason is that households and businesses would want to borrow against their perception of higher future income now in order to increase current consumption and investment before it's actually available. So the rate needs to rise to induce those consumers and business to defer that spending until in fact the output is available. The Taylor rule doesn't give any attention to that kind of real business cycle reason for a move in rates. It only allows reaction to inflation gaps and output gaps.13

Summing Up

The late 1990s was a period of high productivity growth and low inflation in the U.S. It is widely known that Greenspan explained the low inflation as resulting, in large part, from the high productivity growth. This essay has highlighted Broaddus' contributions to the discussions of productivity growth and monetary policy in the late '90s. Broaddus was an early and articulate proponent of the view that a higher trend productivity growth rate called for higher real interest rates. In a world of stable inflation expectations, a need for higher real interest rates translated directly into a need for higher nominal interest rates. Current speculation about the possibility that AI may deliver an increase in trend productivity growth gives this history from the late 1990s renewed relevance today.

Alexander L. Wolman is vice president for monetary and macroeconomic research in the Research Department at the Federal Reserve Bank of Richmond.

1

For more discussion, see my 2003 paper "Boom and Bust in Telecommunications," co-authored with Elise Couper and John Hejkal.

2

Figure 2 displays CPI inflation instead of PCE because at the time most FOMC discussions involved CPI.

3

See page 28 of the transcript for the September 1996 FOMC meeting (PDF).

4

See the minutes of the March 1997 FOMC meeting.

5

See page 22 of the transcript for the May 1997 FOMC meeting (PDF).

6

His advocacy was discussed in the 2024 article "The Origins of the 2 Percent Inflation Target" by Matthew Wells.

7

See page 20 of the transcript for the July 1997 FOMC meeting (PDF).

8

See page 79 of the transcript for the July 1997 FOMC meeting (PDF).

9

See page 41 of the transcript for the May 1998 FOMC meeting (PDF).

10

See pages 60-61 of the transcript for the March 1999 FOMC meeting (PDF).

11

See page 57 of the transcript for the May 1999 FOMC meeting (PDF).

12

See pages 59-60 of the transcript for the May 1999 FOMC meeting (PDF).

13

See page 100 of the transcript for the June 1999 FOMC meeting (PDF).

To cite this Economic Brief, please use the following format: Wolman, Alexander L. (May 2026) "Al Broaddus, Productivity Growth and Monetary Policy in the 1990s." Federal Reserve Bank of Richmond Economic Brief, No. 26-15.

Views expressed are those of the author(s) and do not necessarily reflect those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us