Modelling Unemployment Insurance in the Real World

Economic Brief

May 2026, No. 26-16

Key Takeaways

- We create an economic model of unemployment insurance designed to accurately capture the life cycle of workers.

- A socially optimal unemployment insurance program would replace 63 percent of a worker’s income for six months after termination.

- This result bridges the previous disagreement between partial and general equilibrium models of unemployment insurance.

There is a robust literature evaluating whether the U.S.'s current unemployment insurance (UI) program — which provides roughly 50 percent of an employee's wages for six months after termination — is the optimal system to maximize welfare. The models used in this literature — which are called partial equilibrium models and focus on effects of the labor market — generally find that the current UI system is close to optimal, with some papers indicating that UI should be even more generous.1

General equilibrium models, on the other hand, attempt to describe an entire interconnected economy instead of a single piece. For UI, these models introduce capital as a production factor, allowing them to describe the interaction between firm production, labor provided by workers, and taxes collected by the government and redistributed as UI. General equilibrium models find that UI is at best useless and at worst harmful: UI reduces both labor (as workers have less incentive to save for periods of unemployment and, thus, work less) and capital (as lower savings means firms cannot invest as much), and these reductions outweigh the benefits of UI.

My (Nicholas) 2023 working paper "Unemployment Insurance when the Wealth Distribution Matters" —co-authored with Facundo Piguillem and Hernán Ruffo — makes an important modification to past general equilibrium models. Most general equilibrium models of UI use infinitely lived workers. Such an assumption makes the economic model easier to compute but fails to model the life cycle of an average worker, who enters the workforce with relatively little experience and wealth and slowly builds up both until retirement. Functionally, these models create an environment where the income conditions that facilitate welfare gains from UI rarely appear. Thus, they indicate a lack of need for UI.

We rectify the discrepancy between partial and general equilibrium models by creating a general equilibrium model with life-cycle effects. Like partial equilibrium models, we find that the U.S.'s current UI policy is close to optimal, if slightly too conservative. Through modifications to the model, we demonstrate that the difference in effects between this model and other general equilibrium models is a result of including life-cycle effects and choice of taxation scheme.

Modelling Unemployment Insurance Policy

The model consists of several agents:

- Firms, which can hire workers and rent capital to maximize their profits

- Workers, who start working at age 23 and stop working at 65, can gain skills (permanently increasing their future income), can be fired, and if fired collect UI benefits and apply for jobs

- The government, which distributes unemployment benefits and collects just enough taxes to fund those benefits

Each period, a certain number of workers are born and some die with a probability determined by their age.

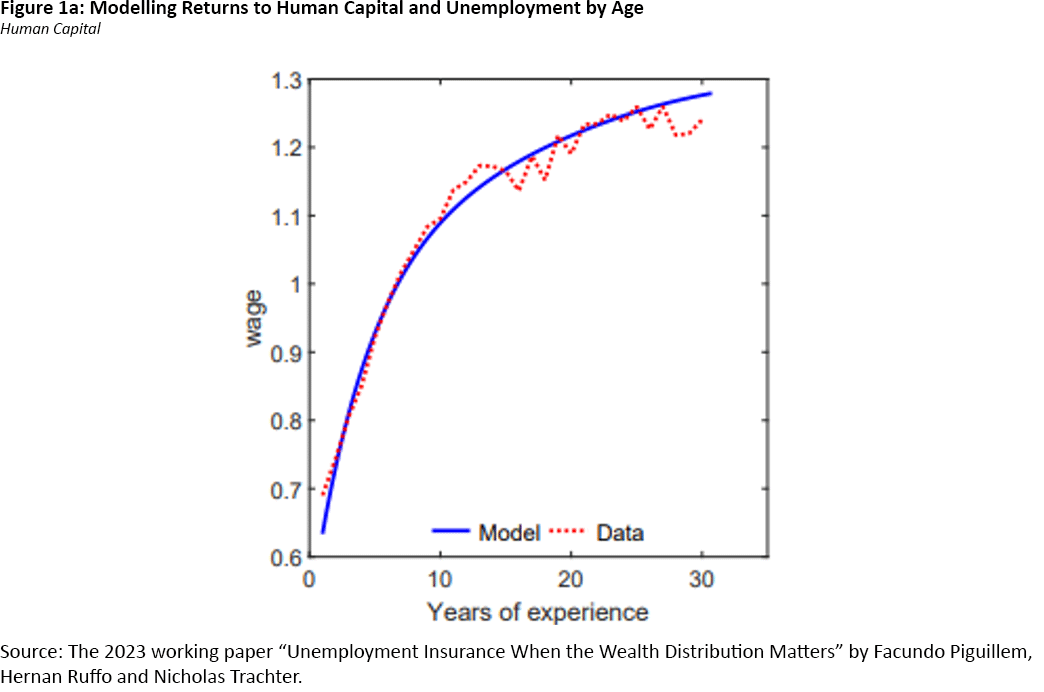

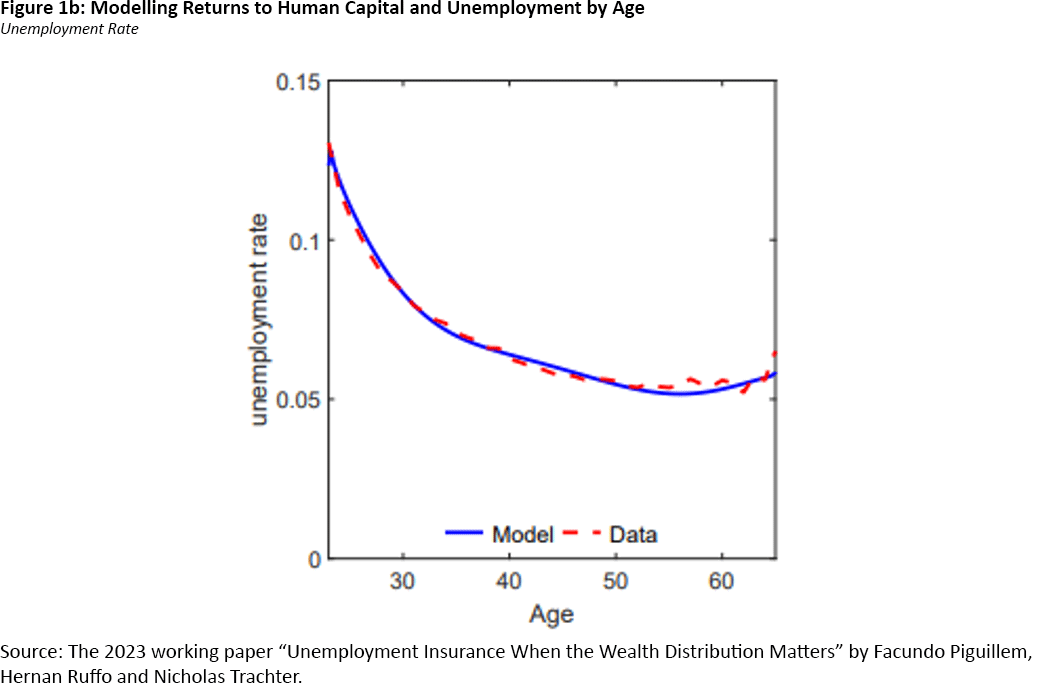

As an initial verification of the model's accuracy, we tested it against real world data. As shown in Figure 1, its predictions of wage by years of experience and of unemployment by age are accurate both in level and in slope.

Model Results

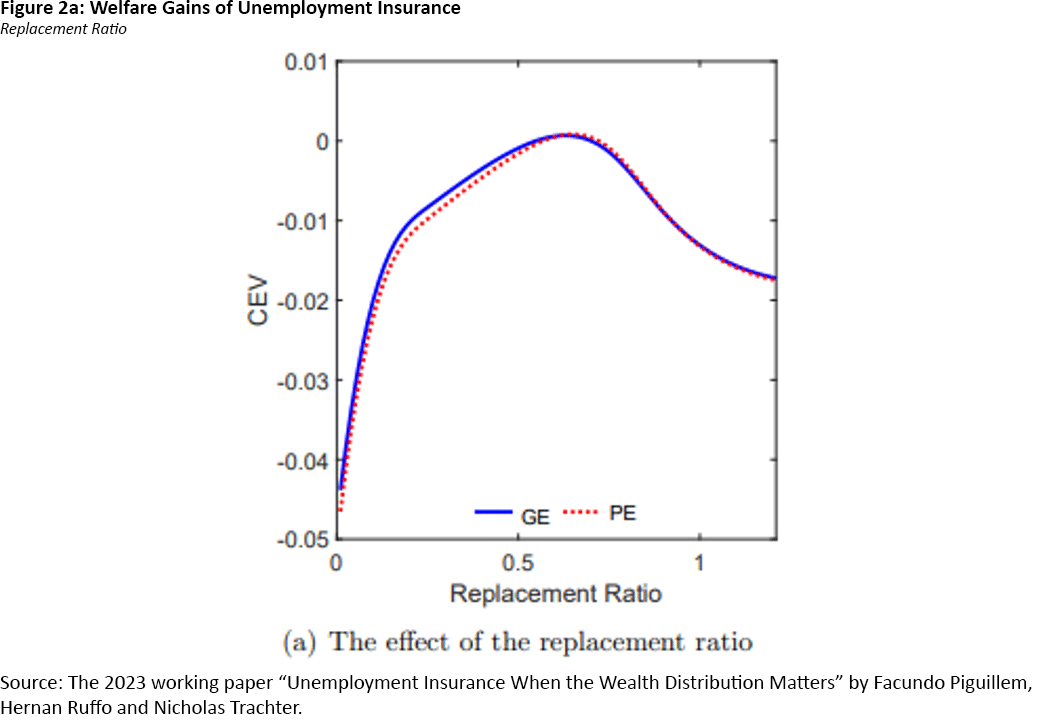

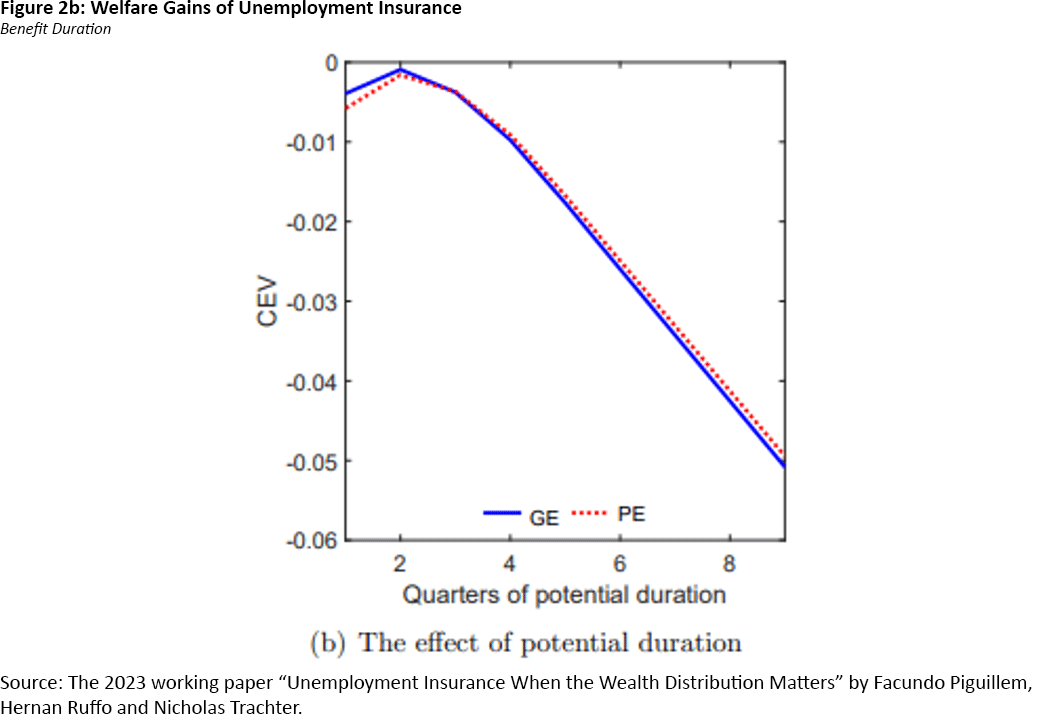

Using this model, we calculate the UI system that maximizes the welfare of all agents in the economy. A key metric here is consumption-equivalent variation (CEV): the percentage change in consumption in all future economies required to make an agent in the benchmark economy indifferent to the reformed economy. In other words, CEV is the welfare loss caused by not implementing the optimal UI system, and the system with a CEV of zero is optimal.

Figure 2 plots the CEV of a UI system by replacement ratio (the percentage of a worker's initial income they get after being fired) and length of insurance benefit. The optimal policy — a 63 percent replacement ratio for six months — is extremely close to the U.S.'s current policy of 50 percent for six months. This result is almost entirely unaffected by the choice between general equilibrium and partial equilibrium models (which include and exclude, respectively, capital as a production factor).

Bridging General and Partial Equilibrium

Why is there no longer a discrepancy between general and partial equilibrium models? The cause rests primarily on the inclusion of life-cycle effects in the model. We modify the initial model to closely resemble past general equilibrium models with infinitely lived agents and constant incentives to save. Thus, we remove human capital accumulation (so workers make constant wages), retirement and pensions from the model.

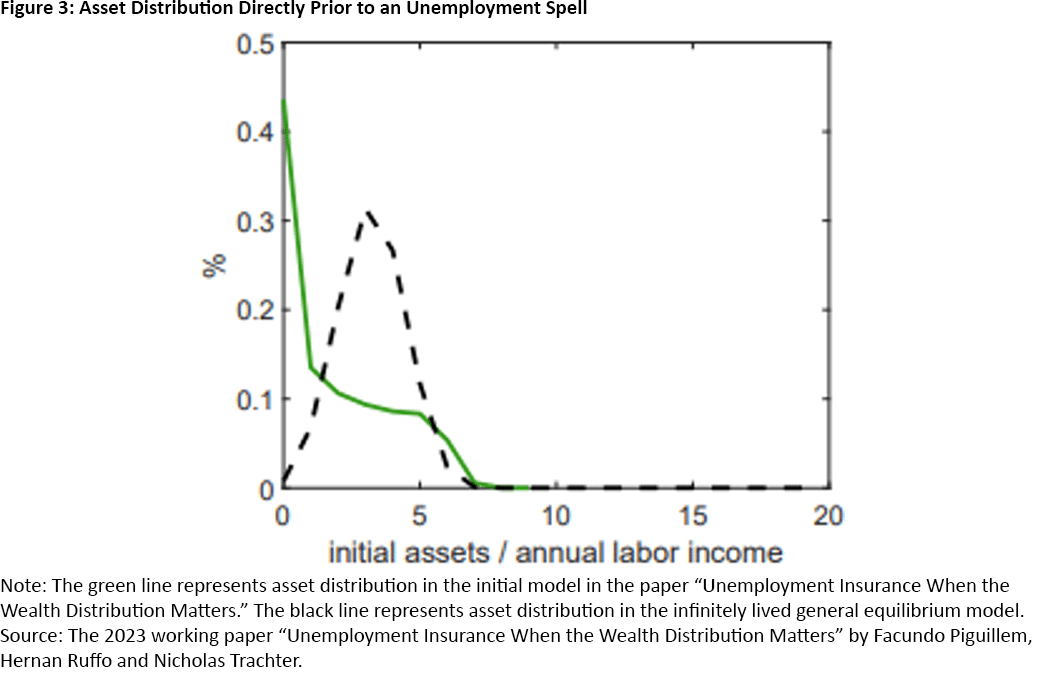

Like past general equilibrium models, the infinitely lived model predicts an extremely small optimal UI policy, which is practically zero percent. This is due in part to the asset distribution among infinitely lived agents. Figure 3 displays the distribution of unemployed workers' assets relative to their annual income at the start of their unemployment spell.

In the extension described in this section, approximately 1 percent of workers have little or no wealth at the beginning of an unemployment spell, compared to 44 percent in the initial model. This does not accurately represent the distribution of assets in the U.S.,2 and it creates an environment in which UI is not beneficial. When a worker has savings above the level required to finance an unemployment spell, the only effect of UI is causing that worker to reduce their savings. Effectively, an infinitely lived general equilibrium model lets workers "save their way out" from the negative consequences of unemployment, making UI useless.

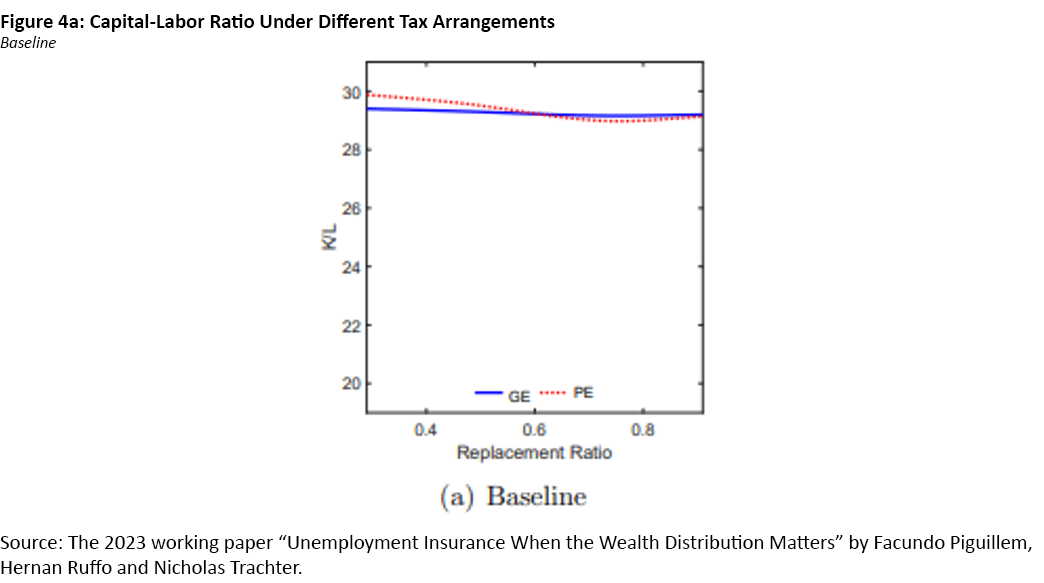

Another cause of the discrepancy between general and partial equilibrium models lies in the sensitivity of the capital-labor ratio. In both general and partial equilibrium, workers must decide how much labor to provide to firms and how much to save, which determines the cost of purchasing capital. In the baseline model that uses a simple income tax, even though UI policies impact the quantity of both labor and capital available to firms, they adjust in similar proportions. As a result, the capital-labor ratio and, correspondingly, prices and welfare loss for workers remain unchanged. This is illustrated in Figure 4a: Even as the replacement rate of UI changes, the capital-labor ratio remains the same.

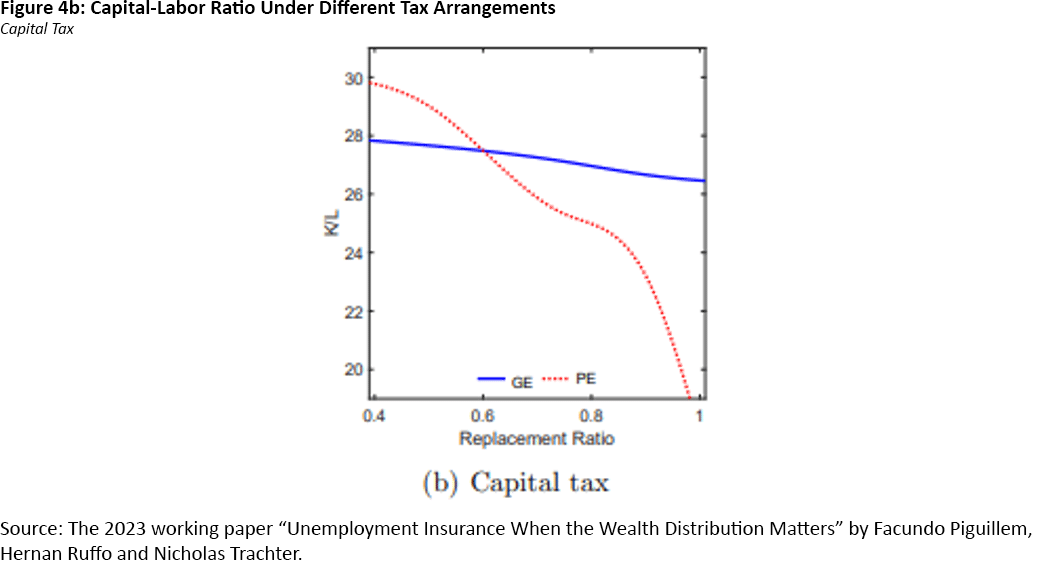

Notably, the capital-labor ratio is not the same between general and partial equilibrium in all economies. As an example, Figure 4b shows an economy that taxes capital at a much higher rate than labor would decrease savings, increasing the interest rate and reducing wages. The capital-labor ratio's elasticity is substantially higher in the general equilibrium model, however, so a general equilibrium model under this taxation scheme predicts a lower optimal replacement rate than a partial equilibrium model.

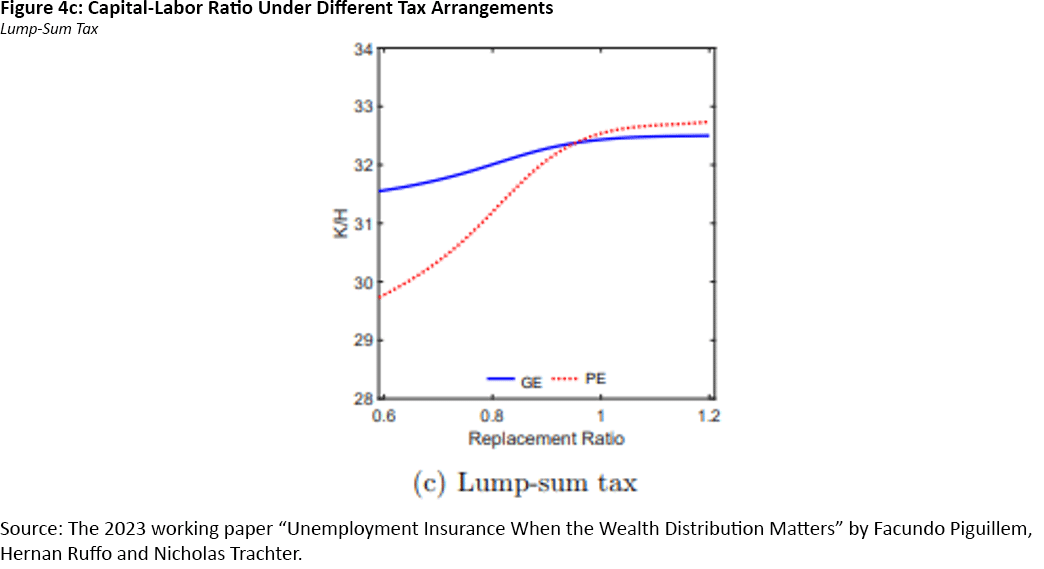

Conversely, in Figure 4c, an economy with a large lump-sum tax at the end of a worker's career increases the capital-labor ratio with more generous UI, with a higher capital-labor elasticity in the general equilibrium model. In this case, the general equilibrium model prescribes a higher optimal replacement rate than the partial equilibrium model.

Conclusion

Using a general equilibrium model that includes the government, firms and the complete life cycle of workers, our model predicts an optimal UI benefits system (63 percent replacement rate for six months) that is extremely close to the U.S.'s current UI system. It also concludes that past discrepancies between the optimal UI systems determined by partial and general equilibrium models are due, at least in part, to general equilibrium models not accounting for life-cycle effects and the funding system for unemployment insurance.

Spencer Cooper-Ohm is a research associate, and Nicholas Trachter is a senior economist and research advisor, both in the Research Department at the Federal Reserve Bank of Richmond.

1

For example, the 2008 paper "Moral Hazard Versus Liquidity and Optimal Unemployment Insurance" by Raj Chetty finds that UI replacement levels are near optimal: Increasing weekly benefits by $1 above the current UI level would yield the welfare equivalent of 4 cents. On the other hand, the 2015 paper "Assessing the Welfare Effects of Unemployment Benefits Using the Regression Kink Design" by Camille Landais finds that slightly increasing the replacement rate or length of UI would be welfare increasing.

2

See Table 2 in the previously mentioned working paper "Unemployment Insurance when the Wealth Distribution Matters" for details.

To cite this Economic Brief, please use the following format: Cooper-Ohm, Spencer; and Trachter, Nicholas. (May 2026) "Modelling Unemployment Insurance in the Real World." Federal Reserve Bank of Richmond Economic Brief, No. 26-16.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us