Flight to Safety: Where Turbulence Means Higher Demand

Macro Minute

April 7, 2026

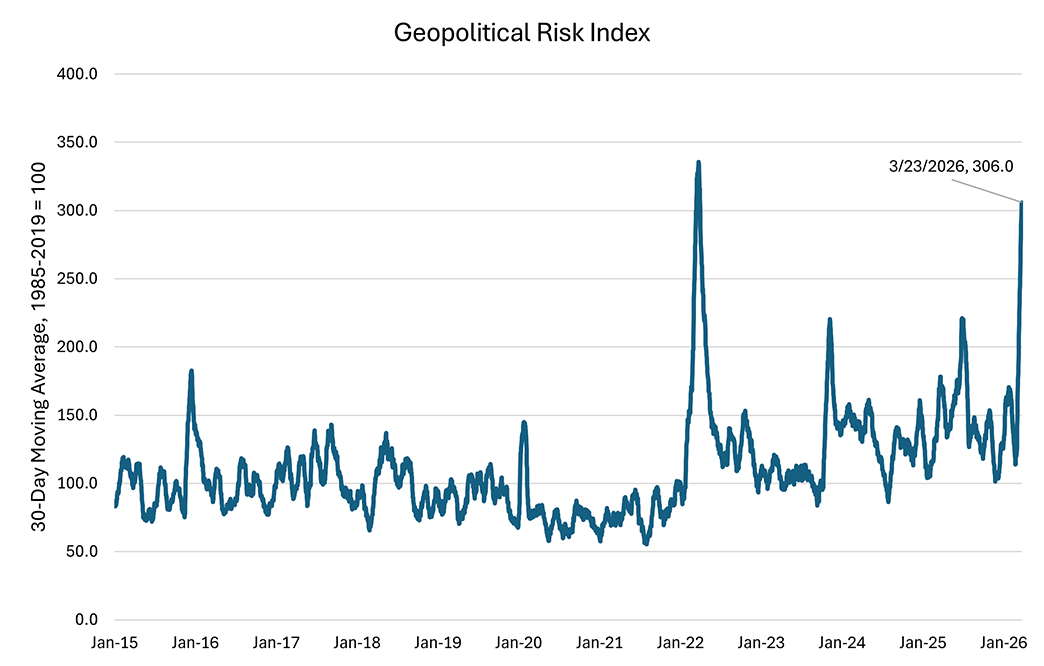

The world economy experienced a geopolitical shock on Feb. 28 when Israel and the United States launched airstrikes on Iran. Figure 1 below shows that the 30-day moving average of the geopolitical risk index — a measure of adverse geopolitical events and risks based on text analysis of newspaper articles — rose to its highest levels since 2022, when Russia invaded Ukraine. According to the authors of the index, higher levels of the geopolitical risk index foreshadow lower investment, stock prices and employment.

Geopolitical shocks can also induce another phenomenon, namely flight-to-safety capital flows as global investors seek to reallocate their capital toward safer assets. In this week’s post, we look at how this flight-to-safety effect has impacted the U.S. dollar and U.S. long-term Treasury yields since the outbreak of the Iran conflict.

The United States has traditionally served as a safe haven for global investors, with U.S. dollar-denominated assets experiencing higher demand during times of economic and geopolitical turbulence. This safe haven status comes from factors such as having a high sovereign credit rating, deep and liquid markets, political and economic stability, and a strong legal system.

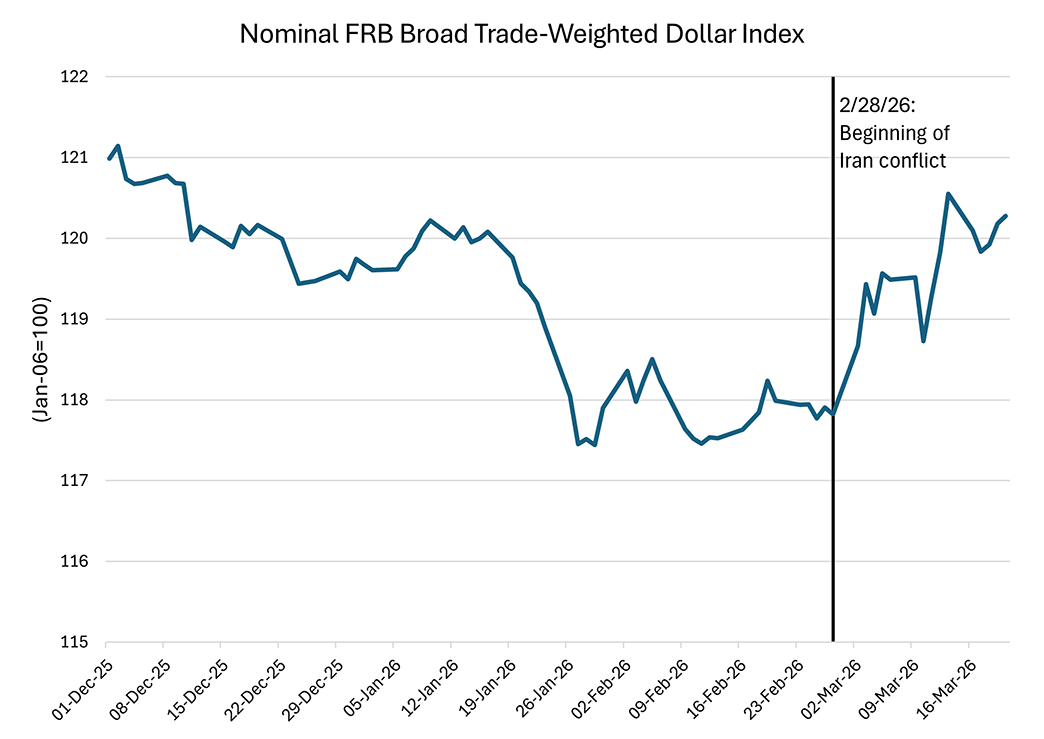

To invest in U.S. assets, foreign investors must first purchase U.S. dollars, and increased demand for dollars following a geopolitical shock can lead to U.S. dollar appreciation relative to the currencies of its trading partners. Figure 2 below shows that the U.S. dollar appreciated after Feb. 28 relative to currencies of trading partners, with upward movements in the broad trade-weighted dollar index indicating currency appreciation.

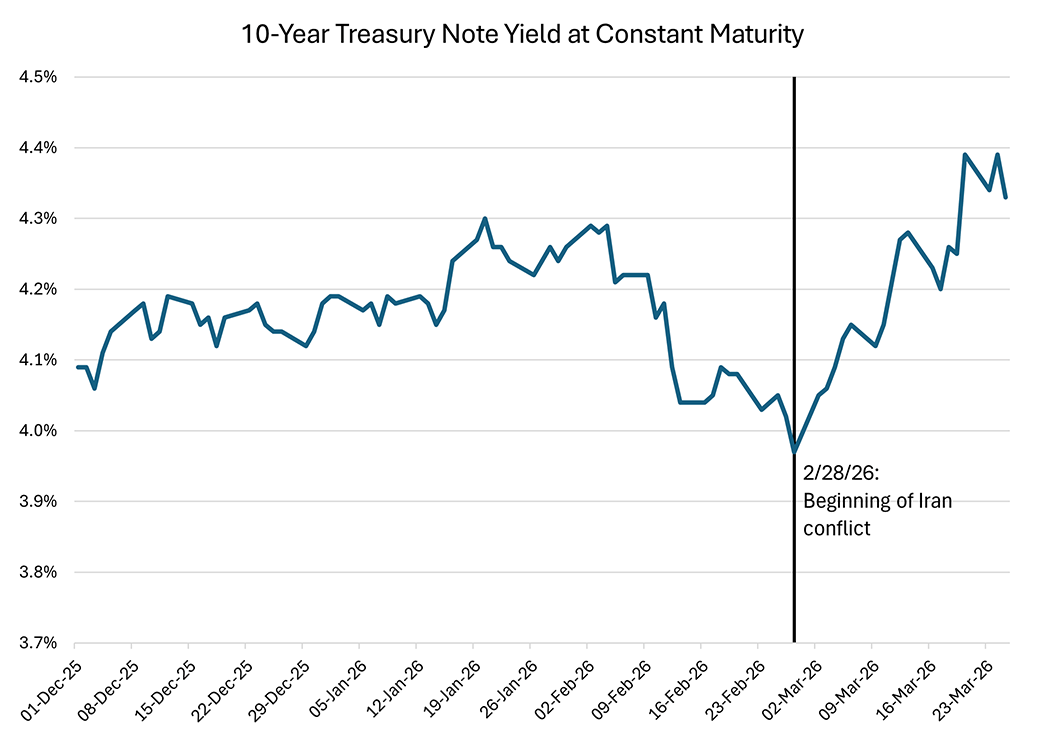

Higher demand for U.S. government debt is associated with higher prices of Treasurys and lower yields. With flight-to-safety capital flows toward U.S. bonds, Treasury yields might be expected to fall. However, Figure 3 below shows that the 10-year Treasury yield rose following the start of the Iran conflict and is roughly 40 basis points above its preconflict level of 3.97 percent on Feb. 27.

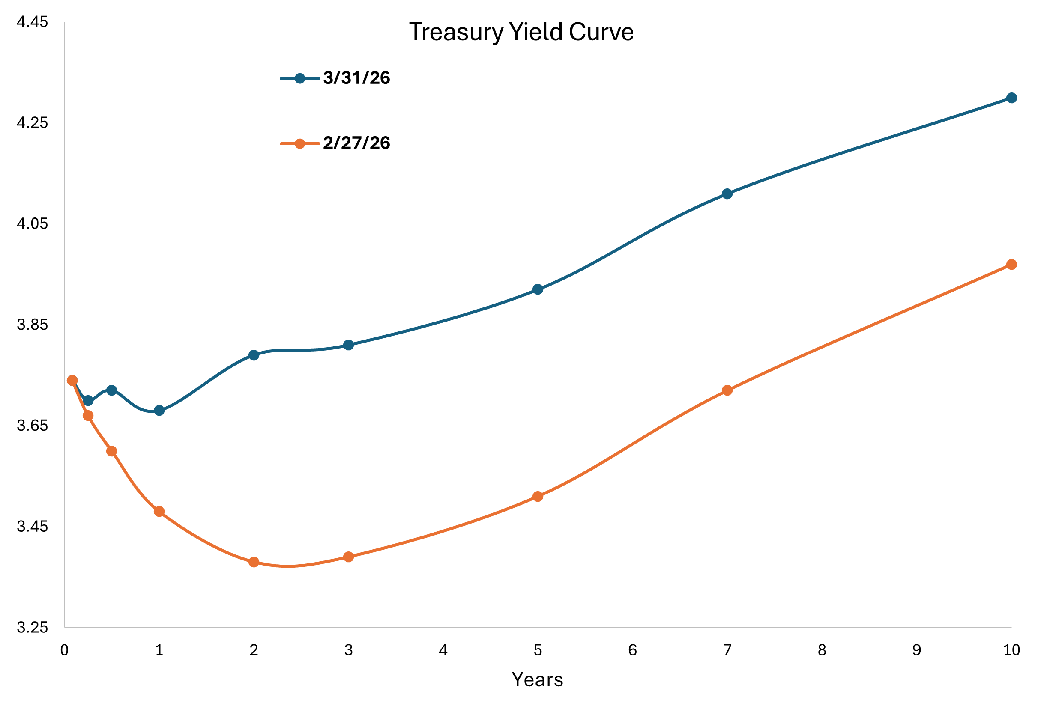

Figure 4 below shows that the rise in the 10-year yield was observed across other maturities as well, leading to an upward shift in the Treasury yield curve.

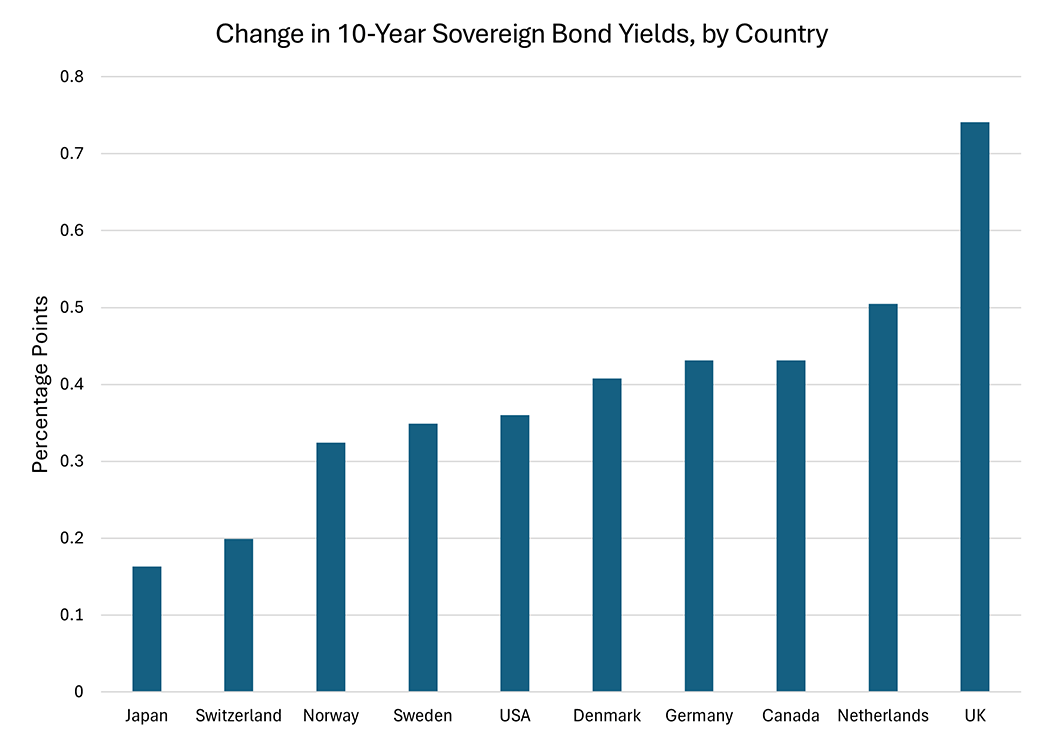

Does the rise in Treasury yields indicate that the United States has lost its safe-haven status? Not necessarily. Figure 5 below shows that, since Feb. 27, yields on sovereign bonds have risen across several countries traditionally viewed as safe havens during episodes of elevated geopolitical stress. This shared increase suggests that other factors — such as an increase in global inflation risks, a reassessment of the likely path of short-run rates or elevated overall uncertainty — may be more predominant in driving up long-term global bond yields, compared to the downward pressure on yields associated with flight-to-safety flows. Amid such factors, the flight-to-safety effect may still be operating in the background, preventing U.S. Treasury yields from rising further than they already have.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us