Job Openings Up, But Jury Still Out

Macro Minute

June 23, 2026

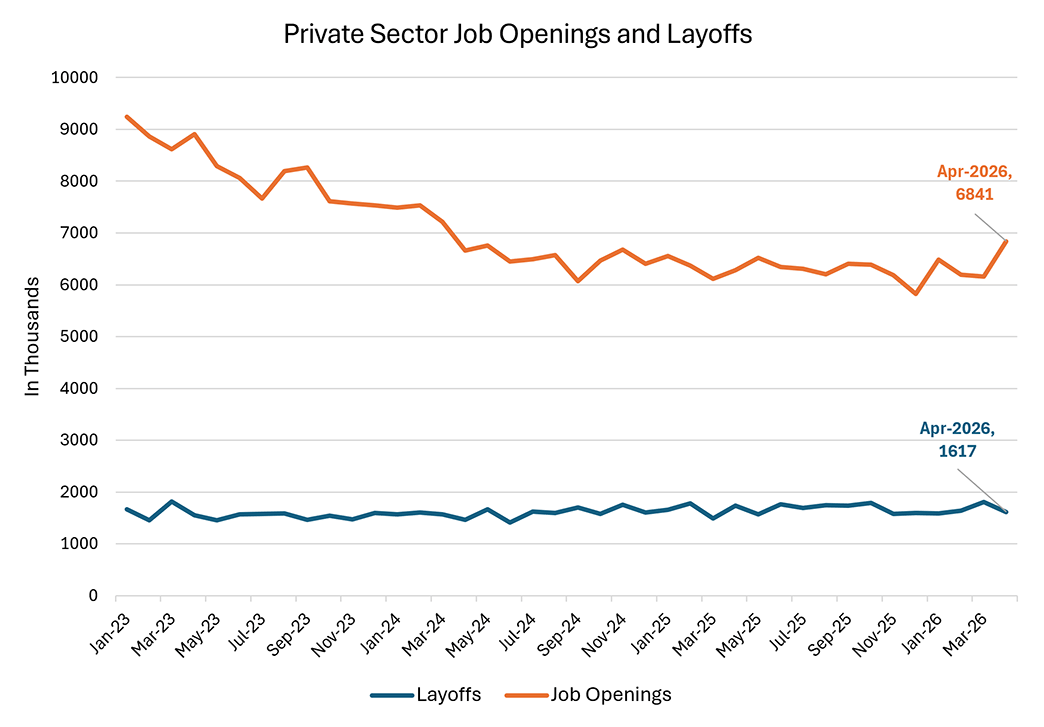

The latest Job Openings and Labor Turnover Survey (JOLTS) release offered a potential sign that labor market activity could be picking up. As shown in Figure 1, private sector job openings rose 11 percent from 6.2 million in March to 6.8 million in April, which is their highest level since March 2024. Meanwhile, private sector layoffs remained low at 1.6 million in April (compared to 1.8 million in March) and have remained relatively stable over the past three years.

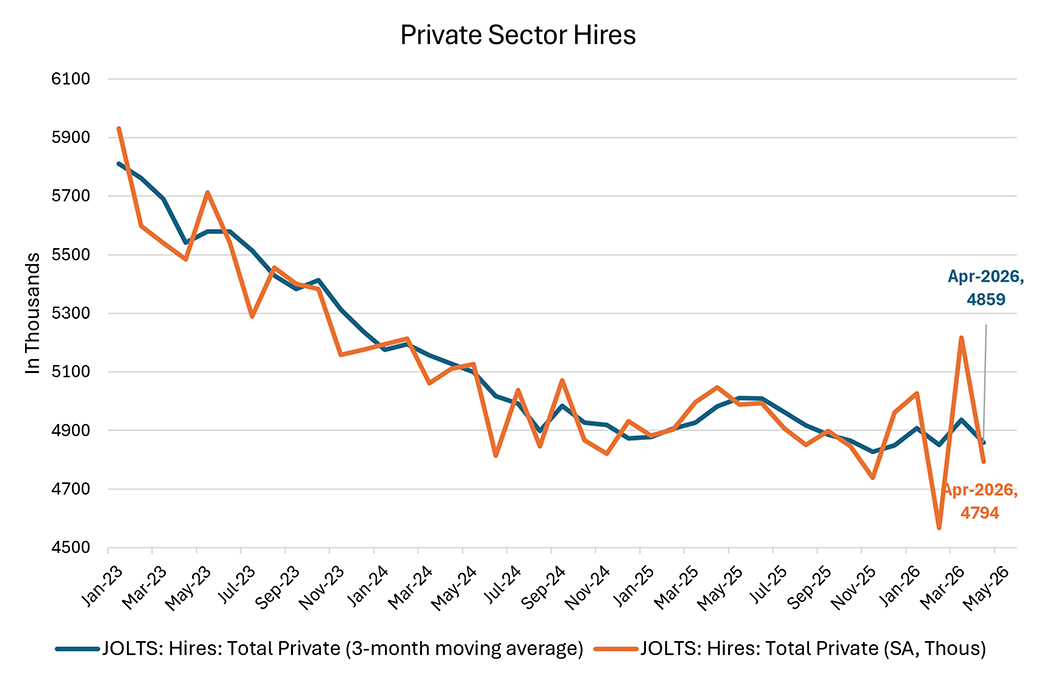

However, April's JOLTS report also showed that the increase in job openings was not accompanied by an increase in hiring. Figure 2 below shows that private hires fell 8 percent in April to 4.8 million, compared to 5.2 million in March. While the latest monthly hires readings have been volatile, the three-month moving average of private hires has remained stable at 4.9 million, similar to the levels observed over the past three months. Although there can be a lag before new openings are converted into new hires, the latest data support the idea that the labor market remains in a state of low hiring.

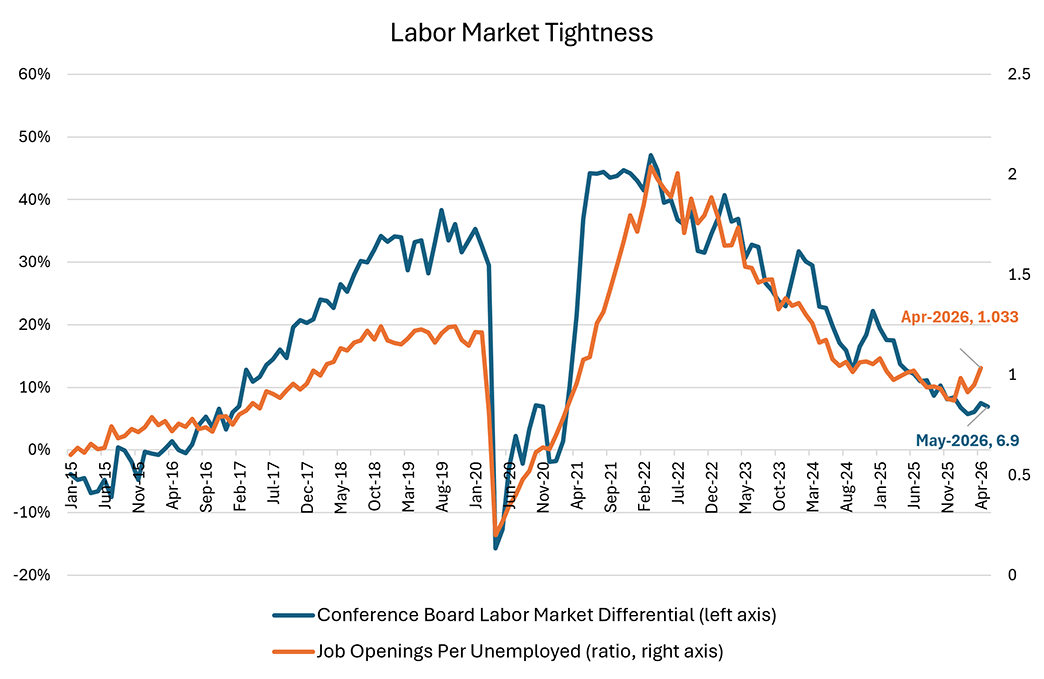

Limited hiring may explain why sentiment measures of labor market tightness have not increased as much as job openings. Figure 3 below plots the Conference Board's labor market differential, which is a consumer survey-based measure of labor market tightness calculated by subtracting the share of respondents who think jobs are hard to get from the share of respondents who see jobs as plentiful. In recent months, this measure has not picked up as notably as the ratio of job openings to unemployed (V/U), which is computed from official data from JOLTS and the Current Population Survey. While the V/U ratio is currently at its highest level since January 2025, the latest labor market differential dropped from April's readings and remains below all of its 2025 readings.

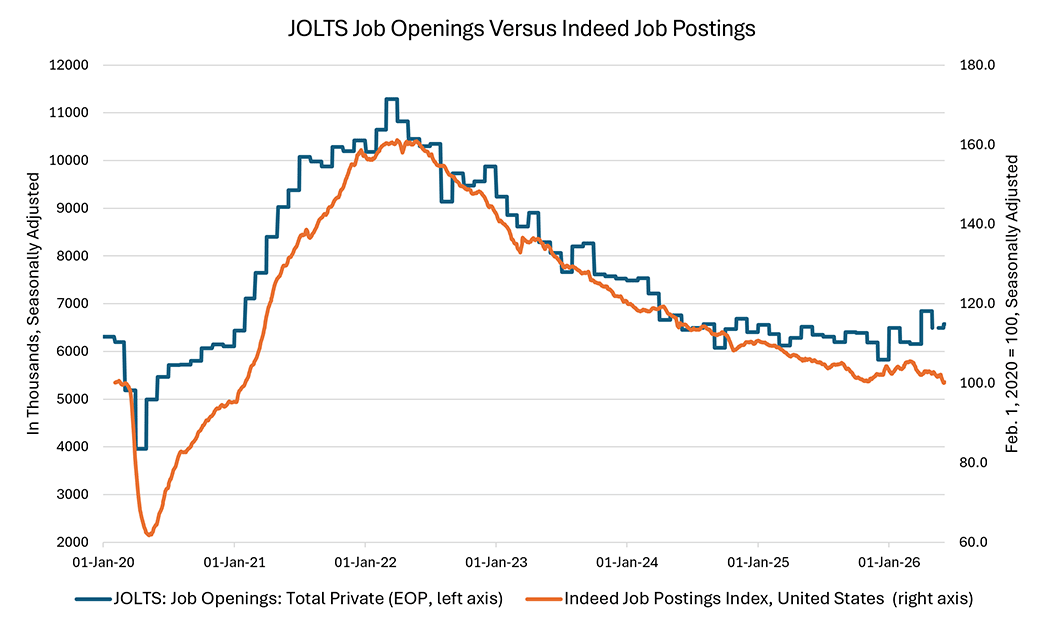

Furthermore, alternative data suggest reasons to view the latest uptick in job openings with caution. Figure 4 below compares the official JOLTS private sector job openings measure with Indeed's job postings tracker. While the Indeed measure has reliably tracked the official job openings series since the start of the pandemic, it appears to be diverging from the JOLTS survey. In the latest weekly readings, Indeed job postings appear to have flatlined or even be slightly trending downwards, in contrast to JOLTS and its apparent upward trend.

With job market sentiment and alternative job postings data continuing to look weak relative to recent official data, it remains uncertain whether the labor market is notably strengthening heading into the summer. Although job openings may have recently jumped, it's best not to jump to conclusions.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us