Price Pressures Pop at the End of 2025

Macro Minute

March 3, 2026

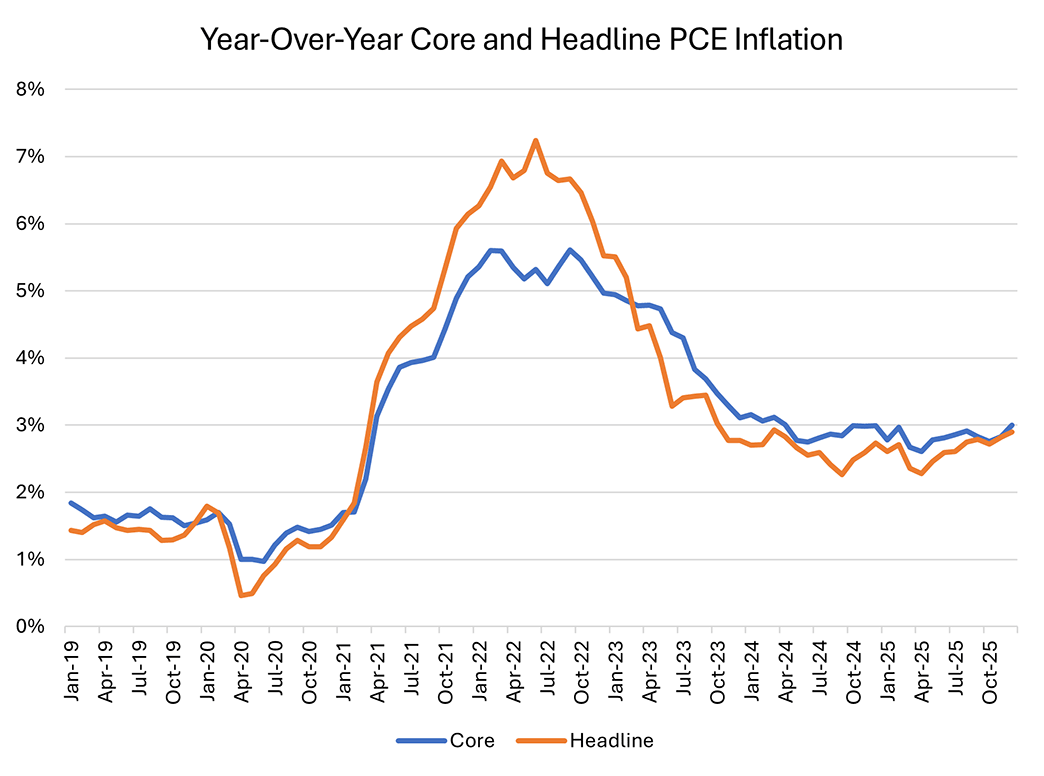

PCE inflation remained high at the end of 2025. Headline PCE prices rose 0.4 percent monthly in December (the same as in November), making the year-over-year headline inflation rate 2.9 percent. Core PCE prices rose 0.4 percent monthly in December (compared to 0.2 percent in November), making year-over-year core inflation 3.0 percent in December. By comparison, in December 2024, year-over-year headline and core inflation was 3.0 percent and 2.7 percent, respectively, indicating little progress over 2025 in bringing inflation to the Fed's 2 percent target.

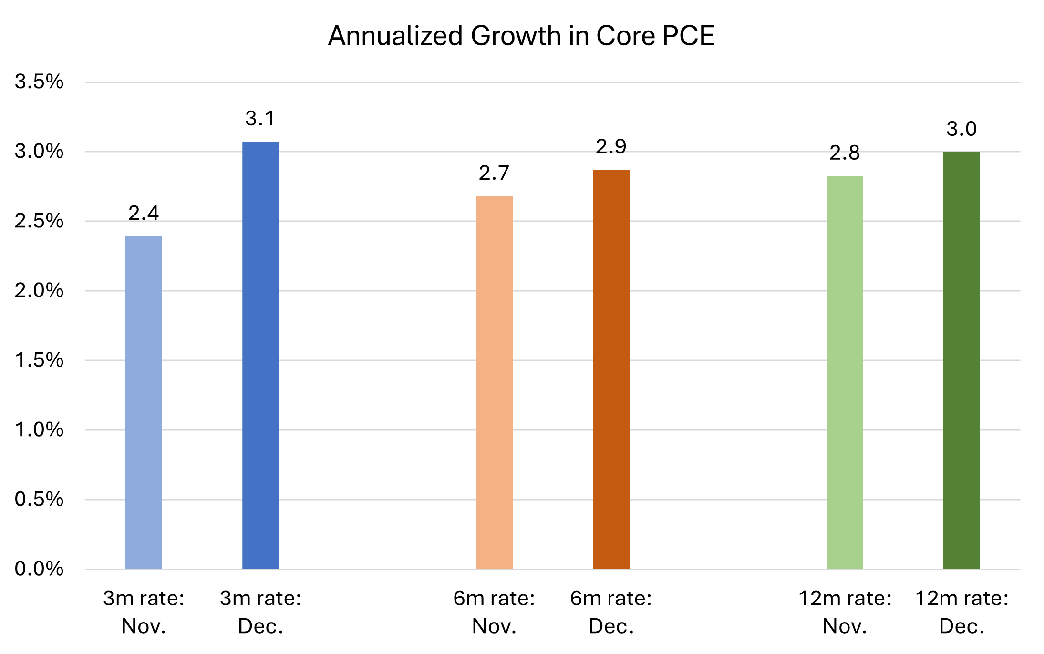

Core PCE price growth over the past three months and six months has also remained high. As shown in Figure 2 below, both the three-month and six-month annualized percent changes in the core PCE price index were around 3 percent, which shows a lack of sequential progress as the calendar year ended. In contrast, if inflation pressures had lessened over the course of 2025, the three-month annualized growth rate in December would have been lower than the 12-month growth rate.

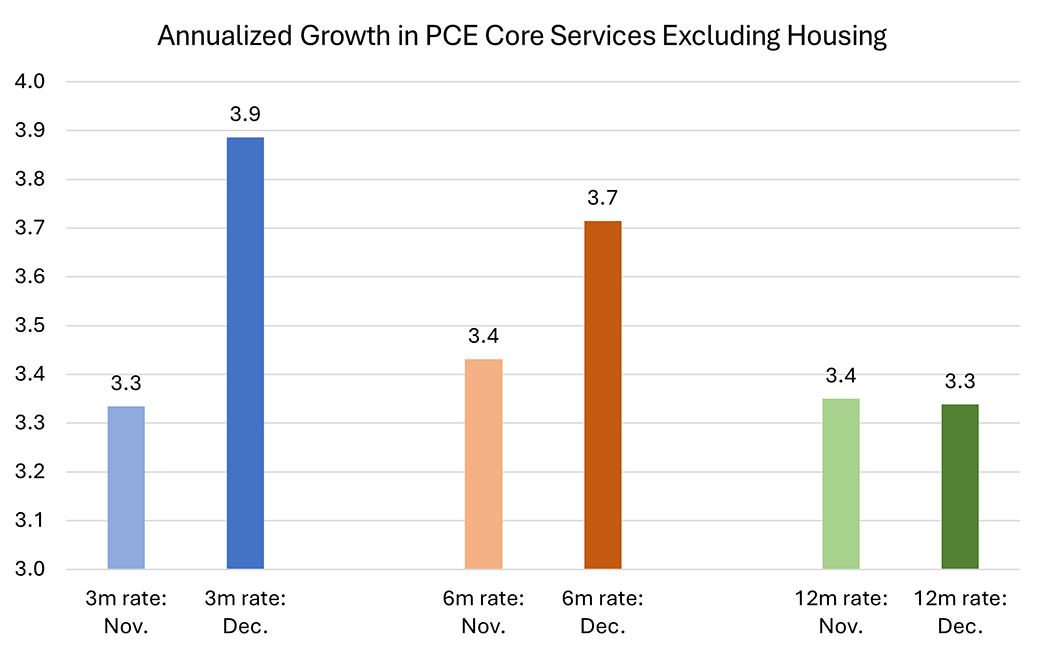

The lack of progress in 12-month headline and core PCE inflation in 2025 is a concern because year-over-year growth in the rent components of PCE are currently downwardly biased. These components — which capture tenant rents and imputed rents of owner-occupied housing — make up over 15 percent of the headline inflation measure and nearly 20 percent of the core inflation measure. The downward bias in measuring year-over-year rent growth stems from the government shutdown late last year, which led statistical agencies to assume zero rent growth in October 2025. This issue will be resolved in April 2026 when the housing units that should have been measured in October will be reassessed by the Bureau of Labor Statistics.

In the meantime, price indexes that exclude rents arguably provide a less biased view of inflation progress. One such index is the price index for services excluding energy and housing (also called "core services ex housing"). Figure 3 below shows the three-month, six-month and 12-month annualized growth rates of the PCE core services ex housing price index. December saw the three-month rate rise to 3.9 percent, higher than the six-month rate of 3.7 percent and the 12-month rate of 3.3 percent. This ordering suggests price pressures in nonhousing core services worsened over the course of the year. By comparison, during the 2015-19 prepandemic period, all three growth rates were close to 2 percent.

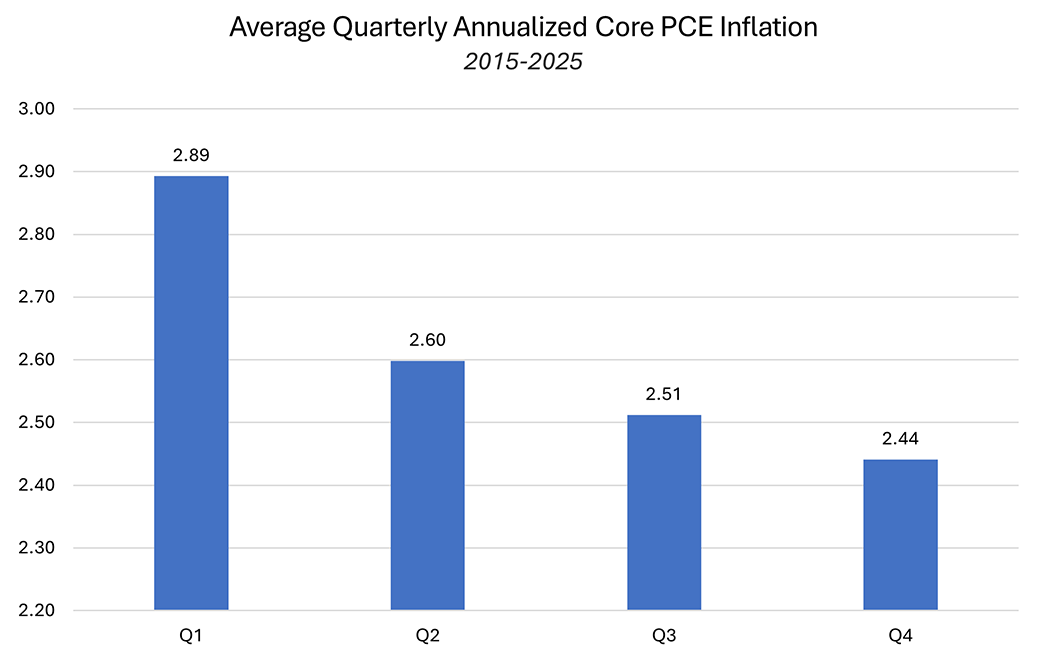

Elevated price pressures toward the end of the year are also concerning in the context of the typical seasonal pattern of price growth seen over the past decade. As shown in Figure 4 below, on average between 2015 and 2025, price growth toward the end of the calendar year has been slower than growth observed earlier in the year. Elevated price pressures at the end of 2025 could be an indication of upside inflation risk in the first quarter of 2026.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us