Supply Struggles: A Multifamily Melodrama

Macro Minute

March 31, 2026

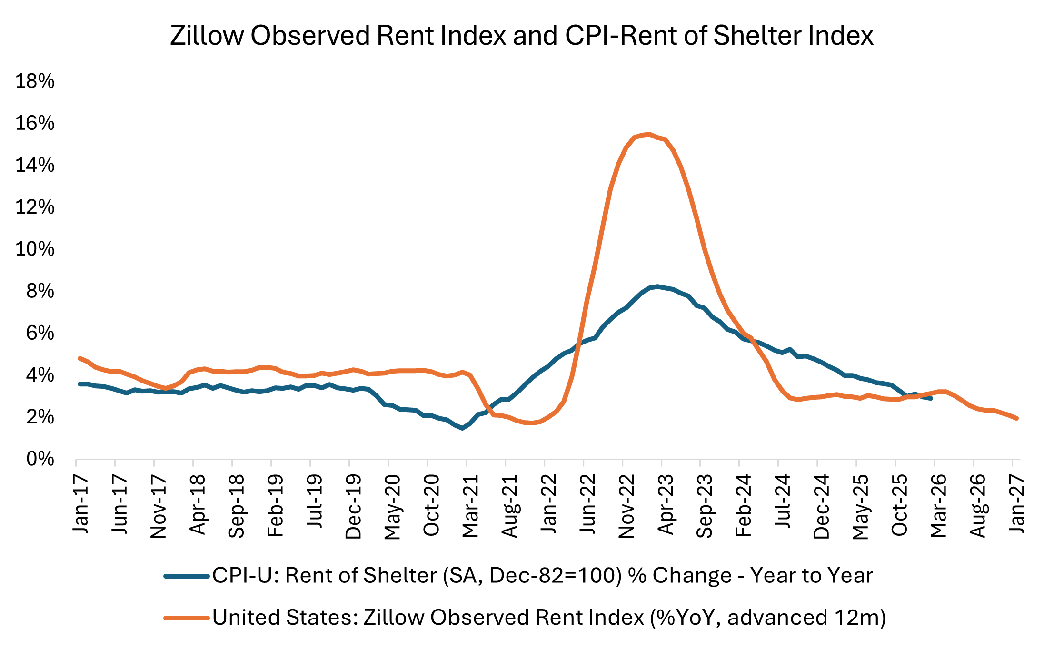

Despite a string of recent high inflation readings, one component of inflation that has been encouraging is rent of shelter, which encompasses rents paid by tenants as well as the imputed rents paid by homeowners on housing services. Figure 1 below shows that year-over-year rent inflation has already returned to prepandemic levels.

More good news on rent inflation could be coming: In a previous post, we discussed how market rents can lead the official rent index by about a year, and Figure 1 shows that the growth rates of market rents as measured by Zillow suggests that the rent growth slowdown is projected to continue over the next 12 months. In this week's post, I discuss how abundant multifamily housing supply has contributed to moderating price pressures in the rental market.

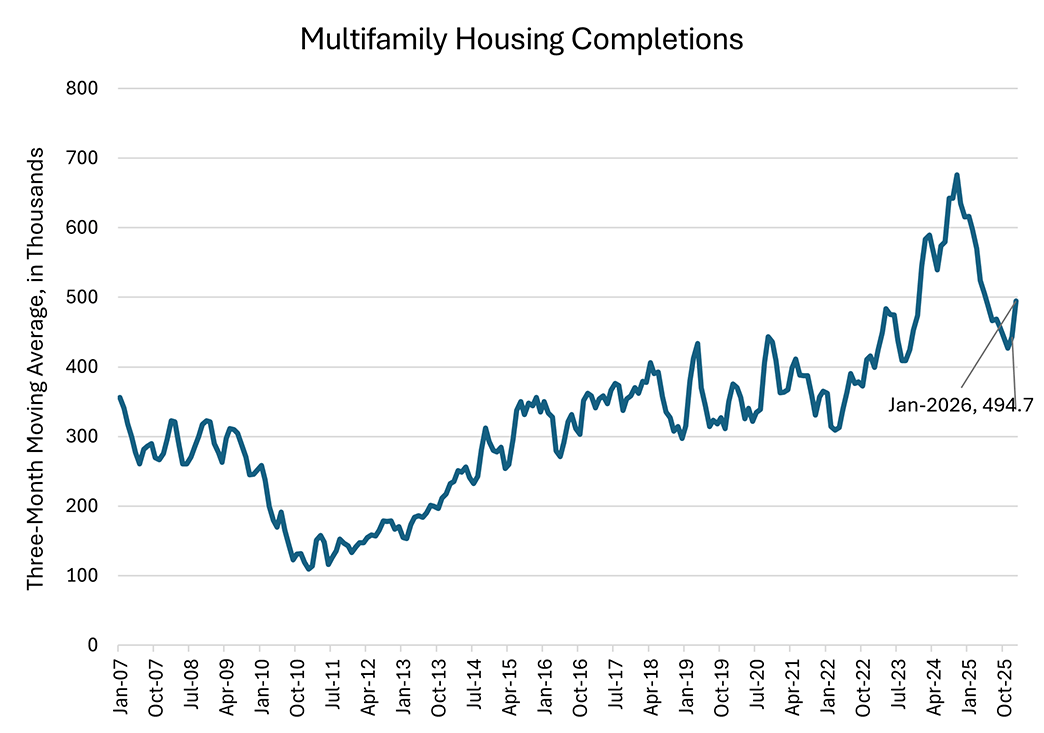

In particular, an influx of new multifamily housing supply has contained rent increases, as seen in Figure 2 below. While multifamily housing completions have fallen since their peak late 2024, they have risen over the past few months and remain well above levels observed during the prepandemic decade. Falling real rents (as rent growth is outpaced by overall inflation) are a possible sign that the quantity of multifamily housing being delivered is in excess of demand growth.

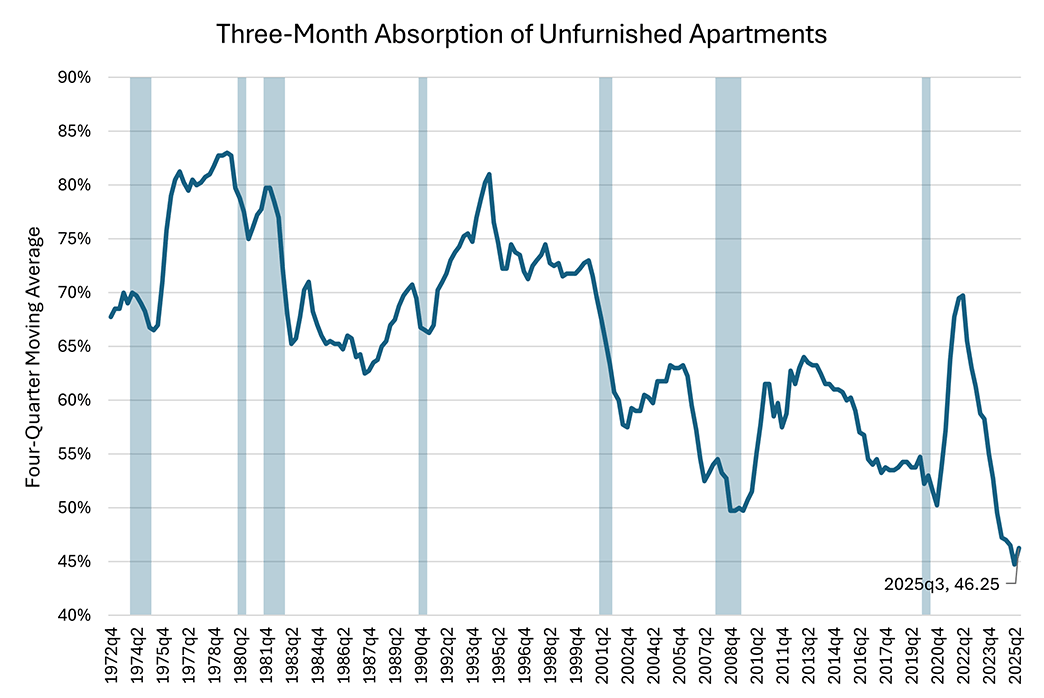

An even clearer sign that the current rate of multifamily housing completions is outpacing demand is a falling absorption rate. Consider the three-month absorption rate, which refers to the share of housing units newly completed during a quarter and rented out within three months. If this new supply outstrips demand, the absorption rate will tend to fall. Figure 3 below plots the four-quarter moving average of this absorption rate for privately financed, unsubsidized, unfurnished apartments based on data from the Census Bureau's Survey of Market Absorption of New Multifamily Units. After reaching a record low of 45 percent in the second quarter of 2025, the latest reading of 46 percent in the third quarter has shown little improvement.

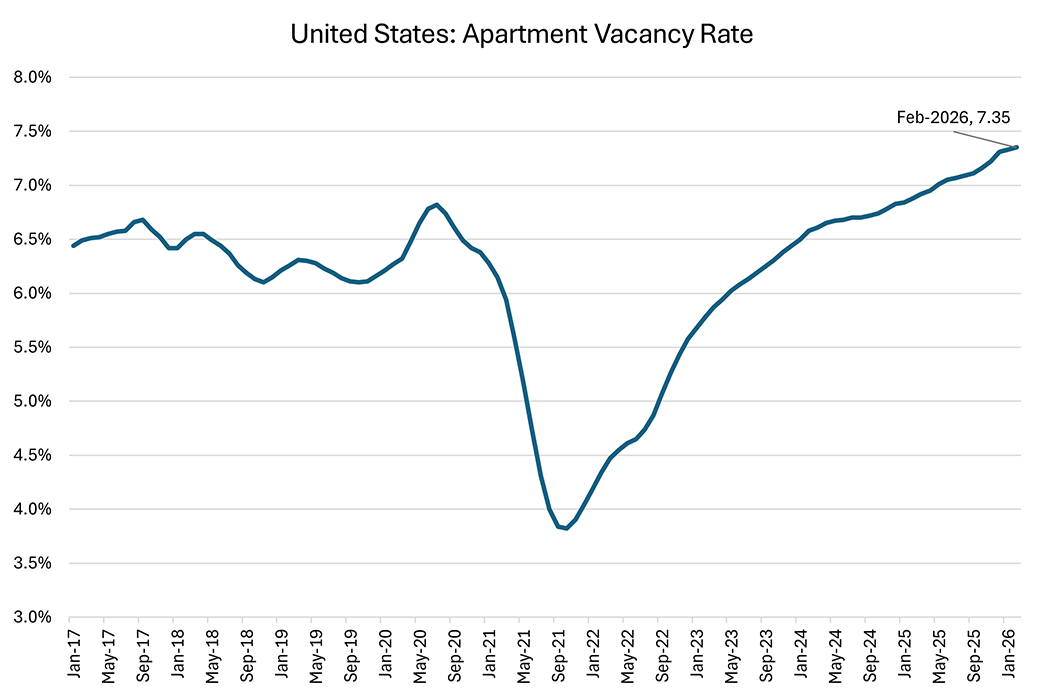

The absorption rate is related to (but distinct from) the vacancy rate, which is also a closely watched barometer of rental market balance. In contrast to the absorption rate — which refers only to the share of newly completed housing units rented out over a subsequent time period — the vacancy rate reflects the share of all housing units available for rent that are currently unrented. The vacancy rate tends to rise when rental demand is weak relative to supply. Figure 4 below plots the vacancy rate as computed by Apartment List, an online marketplace for apartment listings. The most recent reading of 7.4 percent in February 2026 was the highest since the series began in 2017, another sign of softness in the multifamily housing market.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us