The Crop Insurance Boom

A long-standing U.S. farm support program now covers almost every crop — but it attracts more and more critics as well

Econ Focus

First Quarter 2015

BOB NICHOLS/USDA

Corn withers during a drought in Texas in 2013.

Since he began planting cotton in the 1970s, South Carolina farmer John Hane has invested heavily in irrigation to manage risk. Despite the cost, he considers it the best possible protection against drought as well as a way of ensuring that fertilizer and pesticides are evenly distributed through the soil.

In addition, Hane also buys crop insurance. This federal program, which today covers more than 100 crops, lets farmers purchase policies from insurance companies at a subsidized rate. Cotton is among the many crops it covers, protecting against drops in yield or price, and cotton farmers now have more policies to choose from than before. For Hane, however, some of the new policies are more confusing than the traditional system of direct payments from the federal government, which were phased out for all crops in the 2014 farm bill.

"Irrigation helps a lot, but it's not a total solution," says Hane. "It doesn't protect you from hail or hurricanes. So we need something in addition."

A Success Story?

Under the multiyear farm bill enacted in early 2014, crop insurance is expected to cost taxpayers $41 billion over five years — a jump of almost 20 percent over the previous farm bill, enacted in 2008. Crop-insurance advocates argue it is a far more efficient program to manage an array of risks than ex post disaster relief. It has evolved from an underused program that was plagued by adverse selection in the 1980s to one that covers almost every crop today, with high participation. By 2013, 89 percent of all U.S. farmland was covered by the program, covering more than 290 million acres. In 2012, lawmakers didn't even pass stand-alone disaster aid legislation after a devastating drought because insurers' payouts were comprehensive enough for the crops affected. In the view of its supporters, crop insurance has succeeded as a risk management tool because it covers most farmers, pre-empts the need for ad hoc disaster relief, and effectively substitutes for other, less efficient forms of support.

Critics of crop insurance subsidies, however, point to the fact that the program is still a transfer from taxpayers to farmers and private insurance companies, and as constructed, it is more income support than classic insurance. The government covers about 60 percent of the cost of farmers' insurance premiums as well as 100 percent of administrative and operating costs for insurers, which means farmers can sign up for policies that provide payouts far more generous than reflected by their out-of-pocket cost.

This camp, which includes economists, deficit hawks on and off Capitol Hill, and the nonpartisan Government Accountability Office (GAO), argues there are less expensive ways for the government to help farmers protect themselves against extreme or unanticipated losses, and that private insurers do not need taxpayer assistance regardless. And some economists say that these subsidies have a distortionary effect. For example, they may reduce farmers' incentive to manage risk through other means, such as crop storage or prudent fertilizer and pesticide use; subsidies also may encourage planting in high-risk regions and on marginal land.

"The paradox is that crop insurance may be intended as risk management for farmers, but it actually encourages more risk-taking," said Vincent Smith, agricultural economist at Montana State University. "It's a transfer of risk away from the insurance firms and the farmers."

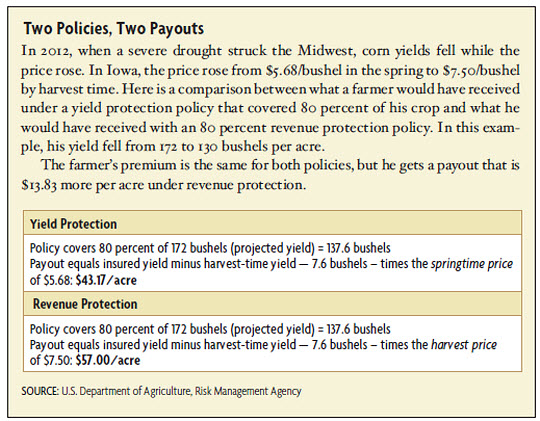

One of the program's most controversial aspects is the policy design. For most crops, farmers have an array of plans to choose from, but the most dominant is an option called revenue protection. Under one of the most popular revenue-protection plans, a farmer can purchase a policy to insure yield losses or revenue losses on certain crops, but he bases that coverage on the highest price of the season. If a low yield drives up the price of a crop from spring to harvest, the farmer is indemnified for lower yields at the higher harvest-time price; if the price falls over the course of the season due to overproduction, the farmer may use the higher springtime baseline when calculating compensation. Either way, this option maximizes the payout from the insurer. Revenue protection contrasts with yield protection, in which a farmer is protected against harvest-time losses in yield, say, in the case of drought; those payouts are pegged to the price projected at springtime. In 2014, about 75 percent of policies were revenue protection, compared with only 13 percent that were yield protection.

The effect of crop insurance on farmers' behavior and the agricultural economy is hard to quantify, because until recently, crop insurance has always co-existed with other farm programs with potentially distortionary effects of their own. Even in the most recent farm bill, which eliminated or overhauled other traditional forms of support, lawmakers still channeled $24 billion in aid over five years to commodity programs. Some economists, however, say evidence suggests that subsidies reduce farmers' willingness to manage risk more efficiently. And more broadly, the program's growing cost has prompted calls to cut the price tag through such measures as trimming payments to high-income farmers or scrapping the revenue-protection option.

Swapping Safety Nets

Farmers of most major crops have received government aid since the Great Depression. These programs have often consisted of price supports, production controls, and ad hoc disaster relief. Insurance has also been available for many crops for years, but a long-standing challenge was finding ways to encourage farmers to sign up for policies. Even after the government began subsidizing premiums in 1980, covering 30 percent of the cost, participation in the program rose only modestly, from 16 percent to 25 percent of eligible acreage. Accordingly, the crop insurance industry was challenged by adverse selection, as most policies were bought by at-risk farmers rather than a broad pool. With too few farmers paying in, the premiums that were paid to insurers often failed to cover the payouts to farmers, even with government subsidies.

All the while, Congress kept passing disaster relief legislation on an as-needed basis, which became frequent. For example, between 1987 and 1994, more than 60 percent of all farms got disaster aid at least once, with some getting it every year. These trends, taken together, bolstered the argument that farmers needed more incentives to buy crop insurance: Ad hoc disaster relief was expensive and unpredictable, but farmers viewed insurance premiums as too pricey.

"The challenge was whether we offer ex ante protection through insurance or ex post protection through disaster relief," said Keith Coble, agricultural economist at Mississippi State University. "Over the years, a consensus grew that ex ante is more efficient, because that way, farmers go into the growing season knowing what coverage they'll have."

New legislation in 1994 offered farmers subsidized catastrophic risk protection as well as the option to "buy up" coverage beyond that. But it was not until 2000, after more rounds of disaster relief, that the government ramped up the premium subsidy and equalized its support for both yield- and revenue-protection policies. Participation took off: Enrollment jumped from 182 million acres in 1998 to 265 million in 2011. The higher participation rate, in turn, has largely eliminated the problem of adverse selection. Still, Congress passed a series of disaster relief bills, totaling around $10 billion from fiscal 2001-2009, to cover losses, especially for under-insured, high-risk regions.

Outside of crop insurance, another change was underway: In 1996, many traditional support programs, which were based on historical price averages, were abolished and replaced with direct payments. These were not based on annual income, prices, or output; rather, they were automatic transfer payments intended to temporarily help transition farmers to a more market-based system. Still, Congress kept on reauthorizing direct payments, effectively converting them into long-term support. By 2011, direct payments averaged $5 billion annually. These transfers came under increasing fire because the program allowed much of the money to go to wealthy farmers, as well as to farmers who did not plant the covered crop in that crop year.

The most recent farm bill, passed in early 2014 as a five-year authorization, eliminated direct payments and some other forms of support while increasing the budget for crop insurance subsidies and bringing more specialty crops (like fruits and nuts) under its purview. It also added a program called STAX specifically for cotton, offering a subsidy based on county prices to help cover a farmer's deductible on top of existing subsidies for premiums. This measure was intended to entice more U.S. cotton growers to ramp up insurance coverage, in conjunction with a WTO settlement that ordered the United States to dismantle long-running cotton price supports and export subsidies after a successful lawsuit by Brazil.

Risk Management or Income Support?

A farmer has to make two basic decisions when signing up for a policy: how much of the crop to cover, and which type of plan to select. Crop coverage is offered in 5 percent increments; farmers usually choose to cover 65 to 80 percent of their crop. Many crops also have supplemental coverage options that help cover the deductible, which can bring effective coverage to as high as 90 percent.

Premiums are determined by the U.S. Department of Agriculture (USDA) Risk Management Agency and vary considerably, depending on the crop price and an array of risk factors. But the subsidy percentage rates are determined by legislation, and those have risen from an average of 37 percent in 2000 to 62 percent by 2013. Accordingly, the higher the premium is, the higher the dollar amount of the subsidy. And if commodity prices rise — as they have done for the most part in the past decade — the premium goes up as well, because the crop's insured value has grown.

The design and popularity of revenue protection explains much of the increase in crop insurance costs to the government: It offers the most generous payouts but does not require a commensurate hike in premiums compared to other policies. To critics, the revenue protection guarantee makes it easier for farmers to break even or make a profit on high-risk or marginal land that otherwise would not be worth the investment.

To him, the more clear-cut argument is that the current crop insurance regime "crowds out" other forms of risk management that would be cheaper to the taxpayer, including futures contracts as well as more traditional techniques.

"If they were really looking to manage risk, farmers could use off-farm income, diversification of crops, storage, and other macro risk-management tools that are more efficient," he said. "But we have to remember they don't buy insurance for risk management benefits alone. They buy it because the subsidies make it worthwhile."

In Smith's view, if subsidies were cut, farmers would invest more in traditional risk-management techniques rather than pay the market price for most costly, unsubsidized insurance premiums.

"If farmers had to pay commercial rates for insurance, most would be priced out because the insurers would pass along the considerable administrative and operating costs to the customers," he says. "It's more likely they would go back to older, cheaper ways of risk management, like crop diversification, better input use, storage, and so on. This is what we saw in the 1970s and 1980s."

The crop insurance program's growing cost has spurred new reform proposals since the farm bill. President Barack Obama's most recent budget called for cutting $16 billion over 10 years by trimming subsidies for revenue protection, among other measures. A recent bipartisan Senate proposal would also trim payout costs, while another would set a capon subsidies to $50,000 per recipient, saving more than $2 billion over 10 years. (Crop insurance currently has no caps on payments.) The challenge, however, is that farm bills are typically written only once every five years or so. The process has become more difficult in recent rounds, and what was once a bipartisan exercise has become a heavy lift. The last farm bill, in fact, took two years to complete.

The Cotton Case

Cotton is an unusual case for a U.S. commodity in that it has been affected by international trade litigation. The changes that South Carolina farmers like John Hane are adjusting to stem from a long-running dispute between the United States and Brazil. In 2004, Brazil charged that U.S. cotton price supports and export credit guarantees contravened World Trade Organization rules by keeping U.S. cotton acreage artificially high. The WTO ruled in Brazil's favor, forcing farm bill negotiators to find a way to make cotton compliant, and the case was finally settled in October 2014. Expanding crop insurance plans to growers was viewed as the easiest workaround once it was clear that cotton would lose its commodity-program support, and STAX was introduced in its stead.

Cotton, which is primarily an export commodity in the United States, is far less dominant in South Carolina than it used to be, but it remains among the top five crops. In 2012, the state's cotton sales totaled around $214 million, or around 7 percent of the agricultural economy. That share may well decline, however, as farmers face a global cotton glut, amid rising production and stock-piling abroad, and a resulting decline in prices. Cotton now fetches around $0.63 per pound, down from $0.94 per pound in 2012. Lower prices have coincided with the end of direct payments — seen as more generous than crop insurance — to make for a bumpy transition.

Moreover, cotton is more labor intensive than other crops, so it is seen as more expensive to insure. For years, growers were less inclined to buy insurance as long as they had other forms of assistance. Now that the older programs are gone, revenue protection policies are gaining popularity with the state's cotton growers, while STAX has had fewer sign-ups because most farmers see it as too confusing, according to Charles Davis, an agricultural adviser affiliated with South Carolina's Clemson University Extension Service.

Davis says he tells farmers that crop insurance is only one risk-management tool to consider, especially when compared to irrigation.

"In my county, Calhoun, we're highly irrigated, and we've taken the money made during good years and put it into long-term investments like irrigation to give us a high degree of security," he says. "Crop insurance can't do that. It helps cover your production costs and lets you survive another day, but it doesn't do much beyond that."

Davis adds that he has a standard response to farmers who tell him they are unhappy with the switch to crop insurance away from direct payments.

"This is still a benefit you paid for with your taxes," he says. "So quit complaining. You could have had no direct payments and no crop insurance subsidy."

Readings

Coble, Keith H., and Barry J. Barnett. "Why Do We Subsidize Crop Insurance?" American Journal of Agricultural Economics, January 2013, vol. 95, no. 2, pp. 498-504. (Paper![]() available by subscription.)

available by subscription.)

"Crop Insurance: In Areas with Higher Crop Production Risks, Costs Are Greater, and Premiums May Not Cover Expected Losses![]() ." Government Accountability Office, March 2015.

." Government Accountability Office, March 2015.

Glauber, Joseph W. "The Growth of the Federal Crop Insurance Program, 1990-2011![]() ." American Journal of Agricultural Economics, January 2013, vol. 95, no. 2, pp. 482-488.

." American Journal of Agricultural Economics, January 2013, vol. 95, no. 2, pp. 482-488.

Smith, Vincent H., and Barry K. Goodwin. "Crop Insurance, Moral Hazard, and Agricultural Chemical Use![]() ." American Journal of Agricultural Economics, May 1996, vol. 78, no. 2, pp. 428-438.

." American Journal of Agricultural Economics, May 1996, vol. 78, no. 2, pp. 428-438.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us