Linking Municipal Defaults to Inward Migrations

Economic Brief

November 2019, No. 19-11

Not all municipal defaults are created alike. Many follow local bust periods — yet some follow local booms. This Economic Brief presents research linking both bust defaults and boom defaults to the overborrowing incentives created by migration into a municipality. The research also analyzes several possible changes in the policy and financial environments and finds only modest predicted effects from eliminating state-imposed borrowing limits, making certain bailouts available, or increasing interest rates to early 1990s levels.

For municipalities, as for households, heavy borrowing can lead to financial distress — and, in the worst case, to default and eventual bankruptcy. While a municipality in default generally cannot have its assets seized, the practical consequences can nonetheless be serious, including employee layoffs, deferral of payments to vendors or to employee retirement accounts, and cutbacks in services. A municipality with an untenable debt burden may even be taken over by an emergency manager or control board, as in the cases of Flint, Michigan, in 2011 and Washington, DC, in 1995. From 1970 through 2012, some seventy-three municipalities defaulted on Moody's-rated bonds.1

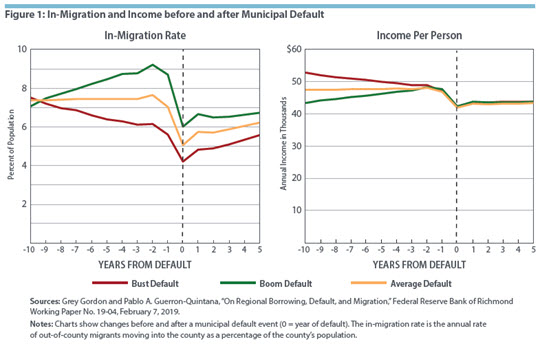

Many instances of municipal overborrowing and default follow a familiar and intuitive pattern in which the municipality suffers a drop in population or personal incomes, causing the tax base to decline faster than the cost of services — a "bust" default. Such a shift may be accompanied by a drop in productivity in the area, possibly reflecting the departure of high-productivity jobs and companies. But there is also a surprising alternative pattern, the "boom" default, in which default is preceded by a population or productivity boom. Two of the authors of this brief, Gordon and Guerron-Quintana, have developed a model to explain the puzzling existence of boom defaults, one that gives a pivotal role to inward migration; they have found support for their model in data on past municipal defaults.2

Looking at Defaults, Boom and Bust

In an effort to isolate some generalities, or stylized facts, about municipal default, the researchers began by considering eight municipalities that served as case studies of default or financial distress: Chicago, Illinois; Detroit, Michigan; Flint, Michigan; Harrisburg, Pennsylvania; Hartford, Connecticut; San Bernardino County, California; Stockton, California; and Vallejo, California. Four of the cities — Chicago, Detroit, Flint, and Hartford — had followed the expected pattern in which their populations declined during the period leading up to their defaults or severe distress. Four municipalities — Detroit, Flint, Stockton, and San Bernardino — had followed the expected pattern in which productivity declined during the period leading up to their defaults.

Yet some municipalities in the group exhibited quite different patterns regarding population, productivity, or both. San Bernardino, Stockton, and Vallejo all saw significant population growth leading up to their defaults. For instance, the population of San Bernardino increased 4.3 percent over the five years leading up to its bankruptcy declaration in 2012. (The population of Harrisburg remained stable.) Hartford and Vallejo saw large productivity gains prior to their defaults. Gordon and Guerron-Quintana label such cases "boom" defaults.

What united these municipalities was, of course, high debt levels. While the average U.S. city owed less than $1,000 per resident in 2011, Detroit owed about $12,000. In some instances, policymakers took steps to move a city's debt off of its balance sheet as a formal matter; for example, Harrisburg sold an incinerator project to a municipal authority while also guaranteeing the debt issued by the authority, thus remaining responsible in reality.

Modeling Municipal Borrowing

In Gordon and Guerron-Quintana's model, municipal policymakers seek to maximize the welfare of current residents. This motivation means that a flow of migration from other areas into the municipality acts as an externality that will tend to lead policymakers to borrow more: current residents will benefit in the short term from the projects funded by the debt, but those residents will not bear the full burden of repayment — the debt will be repaid by both current residents and future arrivals. A positive shock that causes a greater flow of in-migration will therefore create an incentive for policymakers to borrow more.

For the regressions with which they test their model, Gordon and Guerron-Quintana use Census Bureau data to calculate county-by-county measures of population, migration, interest rates, debt, government spending, and productivity. Their regression results support their theoretical model in which a shrinking population leads to a bust default, while in-migration during booms creates an incentive for overborrowing, leaving the boom city overleveraged and vulnerable to negative shocks. (See Figure 1.)

The researchers then use the model to analyze the likely effects of several potential changes to the policy environment or financial environment. The first is eliminating state-imposed borrowing limits, which exist in many states to constrain local government borrowing — probably reflecting an intuition on the part of state policymakers that localities would tend to overborrow under some conditions if left to their own devices. Such limits are commonly based on a percentage of assessed property valuations, although California is a notable exception in tying its limit to local indebtedness and revenues. Data from California and Michigan indicated that municipalities in both states were generally close to the legal limit of their indebtedness, suggesting that many were borrowing as much as they legally could. To help determine how important borrowing limits were for restraining debt and default, the researchers analyze the counterfactual scenario of no borrowing limits. They find that eliminating the limits probably would have little effect because private credit markets constrain municipal borrowing almost as much as the state-imposed rules.

Another change that Gordon and Guerron-Quintana test is making bailouts available to distressed municipalities — specifically, the smallest bailouts adequate to avoid default. Consistent with the view that anticipated bailouts create moral hazard, in much the same manner that the expectation of a bailout may reduce the self-discipline of private financial institutions in taking on risk,3 they find that the availability of minimal bailouts to municipalities doubles the occurrence of default. The effect is not larger, they conclude, because municipal policymakers should be indifferent between a minimal bailout and default and because either option is costly to residents. However, the results could be very different if bailouts were significantly more attractive to residents.

Finally, the researchers analyze the effect of increasing municipal bond interest rates — namely, raising the nominal interest rate on top-rated municipal bonds from 4 percent (its value in 2010) to 6.5 percent (its value in the early 1990s). They find that costlier debt induces local governments to reduce municipal debt per person by an average of 16 percent. At the same time, the higher cost of debt service modestly accelerates migration out of high-debt, low-productivity cities. The effect in terms of cost per taxpayer of moving between these interest rates is minor, however, and thus the effect overall is also minor. In principle, this result implies that a financially equivalent change in the tax-exempt treatment of municipal bonds also would have only minor effects, though the researchers did not separately evaluate such a change.

Gordon and Guerron-Quintana conclude by suggesting that their model for analysis of municipalities also should be useful for analyzing the policies of state and national governments. In their view, a drastic population flight from Puerto Rico, a population decline in Greece, and a large in-migration to Spain are instances in which their model may prove instructive.

Pablo A. Guerron-Quintana is an associate professor in the Economics Department at Boston College. Grey Gordon is a senior economist and David A. Price is senior editor in the Research Department at the Federal Reserve Bank of Richmond.

1

Moody's Investors Service, "U.S. Municipal Bond Defaults and Recoveries, 1970–2012," May 7, 2013. This figure likely understates the actual occurrence of municipal default in that it is limited to rated bonds. For both rated bonds and nonrated bonds, the New York Fed has calculated that a total of 2,521 defaults occurred during the same period. See Jason Appleson, Eric Parsons, and Andrew F. Haughwout, "The Untold Story of Municipal Bond Defaults," Federal Reserve Bank of New York Liberty Street Economics blog, August 15, 2012.

2

Grey Gordon and Pablo A. Guerron-Quintana, "On Regional Borrowing, Default, and Migration," Federal Reserve Bank of Richmond Working Paper No. 19-04, February 7, 2019.

3

Arantxa Jarque and David A. Price, "Living Wills: A Tool for Curbing Too Big to Fail," Federal Reserve Bank of Richmond Economic Quarterly, First Quarter 2015, vol. 101, no. 1, pp. 77–94.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us