Recent Trends in Fifth District Housing Market Indicators

Regional Matters

February 16, 2023

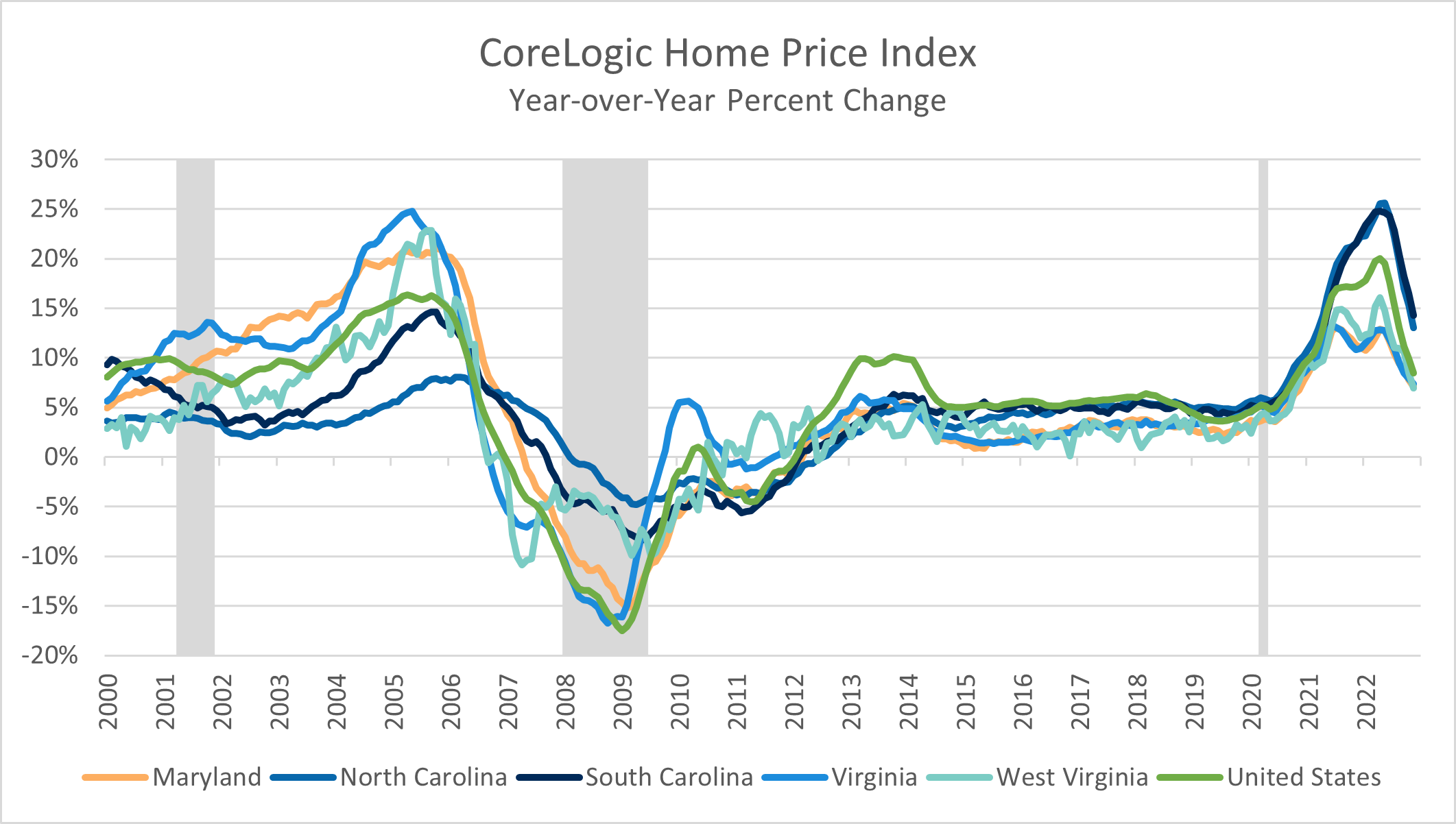

There is evidence that the tight housing markets of the past few years are starting to loosen, with increased supply and falling prices. However, many Americans still struggle to buy a home. Between the fall of 2020 and the summer of 2022, home price growth accelerated in the United States and in all Fifth District states after being relatively steady for a decade. Using the CoreLogic Home Price Index, price increases were most dramatic in North Carolina and South Carolina, where year-over-year increases reached historic highs of 25 percent. While price increases remain high relative to the period between the Great Recession and the fall of 2020, they have moderated for every Fifth District state and for the United States over the past six months. (See chart below.)

Several pandemic-related factors contributed to the run-up in prices, and rising mortgage rates have played a part in cooling them off. Despite price moderation, however, home ownership affordability remains a challenge. This post explores recent movements in underlying home supply and demand indicators and discusses how evolving market conditions are influencing affordability.

Housing Inventory

On the supply side, inventory of homes for sale has started to pick back up after rapidly declining in all five Fifth District states from 2020 into 2021. It measures how many new and existing homes are actively listed for sale at the end of a given month.

The decline in inventory from the beginning of the pandemic through much of 2021 was due in part to delays in construction related to the COVID-19 pandemic, as well as a decline in the number of households putting existing homes on the market. Inventory is now rising on a year-over-year basis in all Fifth District states. (See chart below.)

Months' Supply of Housing

Another indicator — the months' supply of housing — takes into account how well the supply of homes for sale is keeping up with buyer demand. It is measured by the ratio of housing inventory to home sales in a given month. Increasing months of supply indicates that there are more homes available per buyer.

Since mid-2022, months' supply increased in all Fifth District states, reversing the tightening trend between March 2020 and the summer of 2022. (See chart below.)

Sale-to-List Price Ratio

In the past five to six months, sales prices have started to fall below list prices, which is clear from the aggregated ratio of sale prices to list prices. A sale-to-list price ratio greater than 100 percent indicates strong demand because the owner sold the house for more than listed; a value less than 100 percent indicates that the owner sold at a discount, or at least below their expectations.

Leading up to 2020, sale-to-list price ratios in the five Fifth District states were generally below 99 percent, but all increased from 2020 into 2021. During that time, sale-to-list price ratios exceeded 100 percent consistently in Maryland, North Carolina, and Virginia, and in peak demand months in South Carolina and West Virginia.

Starting in the fall of 2022, sale-to-list price ratios began to decline in every Fifth District state, dipping below 100 percent by the end of the year. (See chart below.)

Overall Home Ownership Affordability

Despite rising inventory and moderating price growth, homeownership remains unaffordable to many Americans. The Atlanta Fed’s Home Ownership Affordability Monitor (HOAM) evaluates how affordable home ownership is in national and local metropolitan markets over time, including how much of affordability (or unaffordability) is explained by changes in income, prices, and interest rates. Nationally, the affordability of homeownership has declined since early 2021, with price increases driving the decreased affordability in 2021 and interest rate increases decreasing affordability since the spring of 2022.

Conclusion

Over the past two years, housing markets have been tight with stronger than normal home price growth. There are signs that the housing market is cooling, but affordability remains a challenge for buyers as higher mortgage rates have offset moderating price growth.

To further explore these recent trends and the outlook for the housing market, the Richmond Fed is hosting a special event next Thursday, Feb. 23, "The Highs and Lows of the Housing Market." We invite you to register to attend in person or virtually.

Contact Us