From Loophole to Mandate

Federal policies have fostered employment-based health insurance

Econ Focus

First Quarter 2014

COURTESY OF BAYLOR SCOTT & WHITE HEALTH

A plaque at Baylor University Hospital marks the birthplace of Blue Cross.

Employment-based health insurance was born at Baylor Hospital in 1929. At the time, most births still happened at home, but on the eve of the Great Depression, health care delivery and health care financing were on the brink of dramatic transformations.

In 1929, many medical services were beginning to move from homes to hospitals as people became aware of significant advances in medical science. These breakthroughs made institutional health care more attractive, but just as the demand for hospital services was increasing, people’s ability to pay for those services was decreasing.

When Justin Ford Kimball was put in charge of Baylor Hospital in Dallas, he quickly discovered that many of its patients were not paying their bills. He also noticed that many of those nonpayers were teachers in the public school system, where he had served previously as superintendent. So Kimball devised a prepaid group hospitalization plan for teachers in the Dallas area. For 50 cents a month, they could purchase insurance that would pay for up to three weeks in Baylor Hospital.

The idea caught on with other hospitals, and by 1940, several of these prepaid plans were operating under the Blue Cross banner following guidelines from the American Hospital Association (AHA). The success of the Blue Cross plans demonstrated that focusing on large groups of employed people could make health insurance work by mitigating the problem of adverse selection — the concern that only sick people would sign up for such plans.

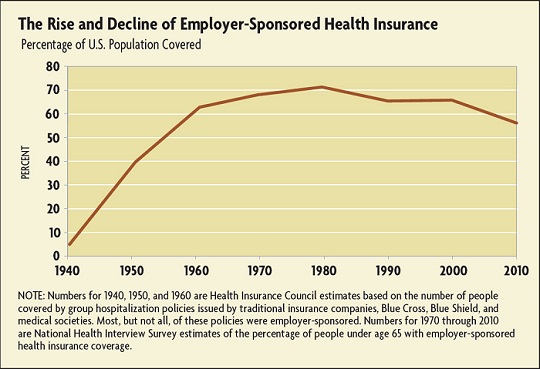

Less than 10 percent of Americans were covered by health insurance in 1940. That percentage was growing as more Blue Cross plans took shape and as commercial insurers began to enter the market, but it was federal government policies that made employment-sponsored health insurance the dominant financing mechanism for American health care. During World War II, the United States instituted strict wage controls administered by the National War Labor Board, but the board did not define employer-paid health care premiums as wages. Faced with surging demand for goods and services and a shortage of traditional workers, corporations started offering group health insurance. By 1957, more than 75 percent of Americans were covered by health insurance, and the vast majority of that coverage was obtained through employer-sponsored plans.

The employment-based system was much better than the charity-based system of hospital financing that it gradually replaced. It kept many hospitals in business, mitigated the problem of adverse selection, introduced economies of scale, and increased access to health care for many people. The system also helped finance the development of new technologies and new drugs that were highly effective. But economists have argued that linking health insurance to employment distorted a variety of labor market decisions and contributed to excessive levels of health care coverage and health care spending.

Despite these flaws, the employer-sponsored system is not likely to go away anytime soon. In fact, mandating employer-sponsored health insurance for employers with 50 or more full-time-equivalent workers is a key provision of the Patient Protection and Affordable Care Act, also known as "Obamacare." The Act’s employer mandate, which takes effect next year, may alleviate some existing labor market distortions while potentially creating some new ones.

Early History

In 1847, the Massachusetts Health Insurance Co. started issuing "sickness" insurance to cover lost wages. At the time, replacing wages was a far bigger issue for sick people than paying health care expenses because most medical treatments were inexpensive and ineffective. Many people resorted to institutional health care only in desperation.

Some employers and labor unions maintained sickness funds, primarily to offset lost wages, and in the late 1800s, a few larger corporations — mostly railroads, lumber companies, and mining operations — started deducting fees from employees’ wages to pay company doctors. These arrangements helped inspire the Blue Cross and Blue Shield plans that emerged in the 20th century.

By 1920, there were 16 European countries with some form of compulsory national health insurance, according to Melissa Thomasson, an economics professor at Miami University’s Farmer School of Business. In sharp contrast, American movements to create compulsory health insurance programs failed in 16 states during the 1910s.

"We didn’t really have the labor movement until the Progressive Era, and when World War I hit, a lot of anti-European sentiment took over," she explains. "We didn’t have the strong centralized government that could make things happen, and on the state level, there wasn’t the organization and the impetus to make it happen."

But the biggest reason why the United States did not follow Europe’s lead was a simple lack of demand. "The public had little confidence in the efficacy of medical care," Thomasson wrote in a 2002 article in Explorations in Economic History. "Patients were typically treated at home, and hospitals were charity institutions where the danger of cross-infection gave them well-earned reputations as places of death."

There was a huge difference between good physicians and bad physicians, she notes, but even the best doctors provided few effective treatments. "Good physicians who were educated before 1920 could diagnose you accurately, they could set bones, they could give you diphtheria antitoxin, and they could talk about hygiene, but that’s about it."

The development of antibacterial sulfonamides (sulfa drugs) did the most to boost public confidence in doctors and hospitals, Thomasson says. "In 1924, Calvin Coolidge’s son gets a blister on his big toe. It goes septic and he dies. In 1936, Franklin Roosevelt’s son contracts strep throat. It goes septic and they think he’s going to die, but researchers at Johns Hopkins were testing sulfa drugs at the time. They give them to Roosevelt and he makes a miraculous recovery."

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us