Can We Tax Social Security Benefits More Efficiently?

Economic Brief

November 2017, No. 17-11

Many seniors pay taxes on their Social Security benefits due to a provision in the program's 1983 reform, under which the portion of benefits that's taxable rises with total income. This tax structure can impose high marginal rates on seniors even if their other income sources are modest. These high marginal rates, in turn, can determine whether beneficiaries decide to keep working or retire. Research suggests that several policy alternatives are more likely to keep seniors in the workforce and to generate more revenue for the Social Security Trust Fund.

Many older Americans are hit with a surprise once they start collecting Social Security — they find that a portion of benefits are taxable. In fact, more and more seniors pay taxes on their benefits each year. But this wasn't always the case. From Social Security's inception in 1935 through decades of expansion, the federal government never taxed the program's benefits. In the 1970s, however, Social Security came under considerable financial duress due in part to the decade's economic weakness, the disruption of high inflation, and policy missteps. In 1983, a bipartisan group of policymakers and experts (including future Federal Reserve Chair Alan Greenspan) hashed out a comprehensive deal to place the program back on the path toward solvency. They also tried to shore it up for the decades to come so that it could absorb the strains of a declining U.S. birth rate and the impending retirement of the baby boomer generation.1 The overhaul was widely seen as successful, although the Social Security Trust Fund still faces long-term solvency issues. (It's projected to run out in 2035, at which point benefits would still be paid, but at lower levels, unless there's a policy fix.)2

That 1983 deal included several provisions, such as gradually hiking the full retirement age from sixty-five to sixty-seven, to stave off insolvency. It also sought to find some new sources of revenue for the Trust Fund. One of those was taxing a portion of Social Security benefits for relatively better-off seniors for the first time. The idea was that lower-income seniors would remain exempt, while those in the middle and upper tiers would pay tax on some of their benefits according to a formula based on their other income. In 1993, Congress established a second, higher threshold so that wealthier seniors would pay an even greater share.3

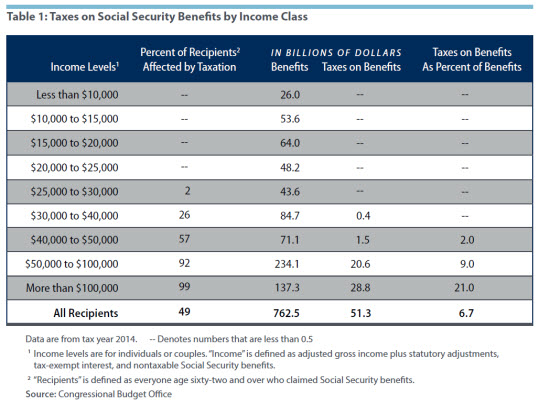

This tax on benefits, while providing revenue to the program, has had some significant consequences on how seniors plan the trade-off between work and leisure. Because policymakers never indexed the original thresholds set in 1983 and 1993 to inflation, these taxes apply to more and more seniors each year. By 2014, nearly half of all beneficiaries owed taxes on their Social Security benefits.4 (See Table 1.) And due to how the thresholds are structured, some of these seniors face marginal tax rates that exceed their statutory rates by 85 percent, even if their total income puts them only in the middle class.

At the same time, an increasing number of Americans are opting to work in their later years. In 1983, for example, only 12 percent of those over sixty-five were in the labor force; in 2016, that share had risen to 19 percent. Yet many seniors (more than one-third) decide to claim benefits early, starting from age sixty-two, and by age sixty-six, more than 90 percent claim benefits. Taken together, these trends mean that many seniors have both wage income and benefit income.5 This fact underlies the key question in this Economic Brief: How do the marginal tax rates on Social Security benefits affect a senior's decision on whether to work, and if so, how much to work? In other words, does the current approach to taxing benefits reduce a Social Security beneficiary's incentive to stay in the labor force, given the prospect of low after-tax pay?

Research by one of this Economic Brief's coauthors, John Bailey Jones, in conjunction with Yue Li of the University at Albany, State University of New York, has found that taxation of Social Security benefits does influence seniors' decisions regarding work, even if many are initially unfamiliar with how benefit taxation exactly works. After testing multiple scenarios on how benefits could be taxed differently, Jones and Li discovered that taxing benefits in the same way as normal income would slightly diminish seniors' labor force participation overall because some lower-skilled workers would tend to drop out. But more highly skilled workers would tend to work more, which on net would bring more revenue into the Trust Fund via the payroll tax on wages. This alternative would allow policymakers to reduce the payroll tax rate without losing revenue.6

A Tale of Two Taxpayers

So how does benefit taxation actually work? The 1983 reform established an income threshold of $25,000 for an individual ($32,000 for couples) so that those below it would be completely exempt from benefit taxation. Then, in 1993, a higher threshold of $34,000 for individuals ($44,000 for couples) was introduced, so that those seniors earning above those totals would see a greater share of their benefits taxed. As noted above, more and more seniors are subject to these taxes, with the greatest impact on those with incomes over $50,000.

The first step in calculating the taxable share of Social Security benefits is adding one's basic income (for example, wages, investment earnings, and other pension income) to one-half of total Social Security benefit income. If the result exceeds the initial 1983 threshold, the difference between that sum and the threshold is divided in half (that is, multiplied by 50 percent). The result, in turn, is the taxable amount of benefits. But if the higher 1993 threshold is crossed, the amount in excess of that second cut-off is multiplied by 85 percent rather than 50 percent.7

As an example, take two individuals, John and Mary. John has a basic income of $26,000, while Mary's is $32,000. Each collects an additional $16,000 annually in Social Security benefits, around the average in 2016. This means that half of those benefits, or $8,000, is added to their basic income to determine whether the initial thresholds are crossed. Accordingly, John's new "provisional income" is $34,000, and Mary's is $40,000.8

This calculation means that John crosses the first threshold of $25,000 but stops exactly at the second threshold. By contrast, Mary crosses both thresholds, with a total well over $34,000. So John must list $4,500 of his benefits as taxable income (half of $9,000, or the difference between $34,000 and $25,000). This lifts his adjusted gross income — basic income plus taxable benefits — to $30,500. But Mary must list $9,600 in taxable benefits ($4,500, like John, plus an additional $5,100, or 85 percent of the difference between $40,000 and $34,000). This boosts her adjusted gross income to $41,600. These adjusted gross income totals are very important because they determine how much tax John and Mary actually pay.

In effect, then, a much larger share of Mary's benefits is subject to taxation even though they both collect the same amount in Social Security payments, and the difference in their basic income (outside of benefits) is only $6,000. So how do these differences in taxable income translate into taxes owed? Based on the Internal Revenue Service's 2016 tax tables and assuming that John and Mary both take a standard deduction of $6,300, claim a personal exemption of $4,050, and apply no other adjustments, John would owe $2,563 in tax on his $30,500 in adjusted gross income, while Mary would owe $4,228 in tax based on her $41,600 in adjusted gross income. In other words, Mary's additional $6,000 of basic income results in an additional $1,665 of tax owed.

Suppose Mary is working a part-time job that earns her that extra $6,000 a year. Once Mary sees the difference between her tax bill and John's, she might rethink her income strategy. In the absence of the Social Security benefits, Mary would fall in the second lowest income tax bracket and pay a marginal tax rate of 15 percent on her earnings. Because of the benefit taxation formula, however, Mary's effective tax rate is 27.75 percent. That jump means that benefit taxation increases Mary's marginal income tax rate by 85 percent.9 In short, she may decide to scale back her hours or even quit.

If Mary does cut back on hours or quit, that outcome is what economists call the substitution effect: she substitutes more leisure in exchange for relatively little after-tax pay. Alternatively, the taxation of her Social Security benefits could encourage Mary to work more while receiving benefits to offset the relatively large tax bill. This outcome is what economists call the income effect. Because households differ in their benefits, earnings, and other income, the substitution and income effects of benefit taxation can vary greatly.10

Making Work Pay

An important insight for understanding these trade-offs is the concept of labor elasticity, or how much a person's incentive to work changes depending on pay and other circumstances. Prime-age workers tend to be labor-inelastic. Wage income is their primary means of support, and they don't have many options for replacing that income with other revenue. Seniors, by contrast, typically have other sources of support, such as Social Security, asset income, or private pension income. Accordingly, they're more likely to have some flexibility on whether they want to substitute work for leisure, everything else being equal. (They also tend to not be supporting dependents at that point, and they have guaranteed health care through Medicare starting at age sixty-five.)11

To test the outcomes of different tax policy alternatives, Jones and Li constructed a model based on the parameters of the U.S. economy in 2006. By analyzing data on work and retirement decisions, and on when seniors claimed benefits, they ran six different scenarios on taxation alternatives, two of which are discussed in detail here. They found that whether benefits are taxed as normal wage income, or not taxed at all, labor force participation and hours worked among higher-skilled seniors rises in both cases. Indeed, in the latter case — not taxing benefits at all — the fiscal impact is effectively neutral because the increased share of seniors working means more revenue for the Trust Fund from the payroll tax.12

So what would the outcome be if most benefits — in this case, 85 percent — were treated like wage earnings, with 6.2 percent dedicated to the payroll tax and the rest taxed as normal income? Jones and Li found that on net, labor force participation among those sixty-two and over would fall slightly, from 28.8 percent to 28.3 percent. But a more important finding concerns what Jones and Li term "efficiency units." This measure takes into account not just the straightforward questions of labor force participation and hours worked, but how workers' skills differ, as well as how much they increase when workers stay in full-time jobs rather than transitioning to part-time positions.13 In this scenario, total efficiency units of labor increase by more than 8 percent, reflecting the increased participation and hours worked among higher-skilled seniors. But perhaps the most dramatic effect would be on the fiscal side: the extra money coming from more highly skilled seniors contributing payroll tax means that the current 12.4 percent levy (which is split between workers and employers) could be lowered to 11.54 percent while staying revenue neutral. This would benefit all workers.

What if Social Security benefits were simply tax-free, like they were before the 1983 reform? Here, too, Jones and Li found positive effects. Labor force participation among those sixty-two and older would rise in this case, from 28.8 percent to 32.3 percent, while total efficiency units for the group would jump almost 16 percent. As for the fiscal effect, the current payroll tax basically could be left unchanged: even though the Trust Fund would no longer get revenue from benefit taxation, most of that would be made up by more seniors paying payroll taxes. (In 2016, benefit taxation generated 3.4 percent of the Trust Fund's total income.)14

Opting In, Opting Out

Regarding these findings, Jones and Li note an important caveat with important policy implications. In their model, they assume that seniors have perfect knowledge of how Social Security benefits are taxed. In the real world, many seniors are unaware of these taxes until they start claiming benefits, and even then, some don't fully understand the complex calculations needed to evaluate the trade-offs. Indeed, other research has shown that only 57 percent of prime-age workers know that benefits are taxable.15 To see how much this knowledge matters, Jones and Li run another calculation under a "limited information" model, in which seniors become aware of benefit taxation only after they have received Social Security for one year. Jones and Li find a modest income effect — on net, seniors work more, so that they can earn more income to offset the unexpected new taxes — but this effect is smaller than the effects of the policy alternatives described above. Their findings also suggest that seniors who are aware of benefit taxation prior to claiming are more likely to delay taking benefits.

Jones and Li's other key findings relate to the nature of labor supply: the impact of Social Security taxation is primarily seen through a worker's decision to stay in the labor force (what economists call the "extensive margin") rather than adding or reducing hours worked per week (the "intensive margin"). This is because the fixed time costs of working (commuting, etc.) encourage most people to work either many hours or none at all. In other words, when a senior faces benefit taxation, it's likely that his or her main decision is whether to stay employed full time or quit altogether. Even though seniors may not know exactly how benefit taxation works, it's clear that working will lead to significantly higher taxes, regardless of whether they adjust hours worked per week. This may well be enough to inform their labor supply decisions.16

In sum, this research shows that potential policy solutions exist that might induce more seniors to stay in the workforce, perhaps even boosting Social Security's solvency. Even though benefit taxation is complex, it has a clear impact on important lifecycle decisions in one's later years given the longer life expectancy and increased labor participation among today's seniors. The subject merits more research among economists to better understand how these decisions are made.

Helen Fessenden is an economics writer and John Bailey Jones is a senior economist and research advisor in the Research Department of the Federal Reserve Bank of Richmond.

1

For a concise overview of the program's history, including the 1983 overhaul, see Patricia P. Martin and David A. Weaver, "Social Security: A Program and Policy History![]() ," Social Security Bulletin, 2005, vol. 66, no. 1.

," Social Security Bulletin, 2005, vol. 66, no. 1.

2

Each year, the government provides an updated account of the health of the program. See Social Security Administration, 2017 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds![]() .

.

3

Robert M. Ball, a key Democratic architect of the program in the postwar years and commissioner of Social Security in the 1960s, made the case that year for hiking taxes on benefits. See "Raise Social Security Taxes," New York Times, July 2, 1993.

4

See Wayne Liou and Julie M. Whittaker, "Social Security: Calculation and History of Taxing Benefits," Congressional Research Service Report, October 27, 2016.

5

The 1983 reform kept intact the option to claim benefits early, starting at age sixty-two, with the trade-off that the monthly payouts are smaller. But it gradually lifted the full retirement age for Social Security from sixty-five to sixty-seven. In general, the share of seniors claiming early has been dropping by birth cohort, but it remains popular. See Alicia H. Munnell and Anqi Chen, "Trends in Social Security Claiming," Center for Retirement Research at Boston College Issues in Brief No. 15-8, May 2015.

6

See John Bailey Jones and Yue Li, "The Effects of Collecting Income Taxes on Social Security Benefits," Federal Reserve Bank of Richmond Working Paper No. 17-02R, September 19, 2017.

7

See Social Security Administration, "Benefits Planner: Income Taxes and Your Social Security Benefits."

8

This comparison has different income figures but is based on a similar example in Liou and Whittaker, 2016.

9

In a real-world case, Mary would pay payroll taxes on these part-time wage earnings as well. To keep the calculations in this article simple, however, payroll taxes are not included in the estimates for Mary and John.

10

Jones and Li suggest that the substitution effects of the benefit tax can dominate the income effects across quintiles. But other researchers suggest a stronger income effect for high earners. In other words, they find that the introduction of benefit taxation in 1983 caused more high-income seniors to stay in the labor force. See Timothy F. Page and Karen Smith Conway, "The Labor Supply Effects of Taxing Social Security Benefits," Public Finance Review, May 2015, vol. 43, no. 3, pp. 291–323 (available with subscription).

11

For an analysis of labor elasticity and how tax policy affects decisions across the life cycle, see Marios Karabarbounis, "A Road Map for Efficiently Taxing Heterogeneous Agents," American Economic Journal: Macroeconomics, April 2016, vol. 8, no. 2, pp. 182–214 (available with subscription).

12

The findings described in this section are explained in fuller detail in Jones and Li, 2017. That paper also elaborates on four other policy scenarios: eliminating the earnings test for benefits; eliminating the earnings test and benefit taxation; eliminating the higher tax threshold of 1993; and keeping both thresholds but indexing them to inflation. All of these are de facto forms of tax cuts for most beneficiaries, and all would increase labor force participation to varying degrees.

13

Typically, when older workers transition from full-time to part-time work, their hourly wages fall. See Daniel Aaronson and Eric French, "The Effect of Part-Time Work on Wages: Evidence from the Social Security Rules," Journal of Labor Economics, April 2004, vol. 22, no. 2, pp. 329–352 (available with subscription).

14

Benefit taxation revenues are split between the Social Security and Medicare Trust Funds. See Liou and Whittaker, 2016, p. 9.

15

Matthew Greenwald, Arie Kapteyn, Olivia S. Mitchell, and Lisa Schneider, "What Do People Know about Social Security?" Financial Literacy Consortium Working Paper, October 2010.

16

See Eric B. French and John Bailey Jones, "Public Pensions and Labor Supply over the Life Cycle," International Tax and Public Finance, April 2012, vol. 19, no. 2, pp. 268–287 (available with subscription). Older workers also tend to divide their late careers into phases, often finding a "bridge job" that is a transition between their former full-time career and retirement. See Michael D. Giandrea, Kevin E. Cahill, and Joseph F. Quinn, "Bridge Jobs: A Comparison across Cohorts," Research on Aging, September 2009, vol. 31, no. 5, pp. 549–576 (available with subscription).

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.