Projecting Unemployment and Demographic Trends

Economic Brief

September 2019, No. 19-09

Demographic forces have profoundly shaped the dynamics of U.S. labor force participation and unemployment over the past forty years. Recognizing the importance of these employment indicators for the conduct of monetary policy, this Economic Brief explores how they have been influenced by the U.S. population's changing gender, educational, and age profile. Based on the authors' estimates, the trend U.S. unemployment rate will decline to 4.3 percent over the next ten years as the population continues to age and increase its educational attainment.

There is a fundamental asymmetry in the Federal Reserve's interpretation of its "dual mandate" of price stability and full employment. Whereas the Fed has adopted a simple, time-invariant inflation target of 2 percent, it has no fixed employment target. Full employment, according to the Fed, "is largely determined by nonmonetary factors that affect the structure and dynamics of the labor market. These factors may change over time and may not be directly measurable. Consequently, it would not be appropriate to specify a fixed goal for employment."1

In monetary policy discussions, "full employment" is commonly identified as the level consistent with the "natural rate of unemployment." Conceptually, a rate of unemployment below the natural rate is associated with excess aggregate demand and accelerating inflation, while unemployment above the natural rate is associated with insufficient aggregate demand and decelerating inflation. Thus, the natural rate of unemployment not only provides an indicator for the Fed's full employment mandate, it also provides a guidepost for the Fed's price stability mandate. Unfortunately, the relationship between unemployment and inflation has varied over time and appears to have weakened in recent years, limiting its usefulness as a policy guidepost.2

The Fed publishes what are, in essence, its policymakers' natural rate estimates on a regular basis. They are labeled "longer-run" unemployment rate projections, and they are defined as the rates to which policymakers expect the economy to converge over time in the absence of further shocks and under appropriate monetary policy. In June 2019, the longer-run unemployment projections ranged from 3.6 percent to 4.5 percent. In contrast, the published projections for longer-run inflation show no variation. Every policymaker's projection is reported as 2.0 percent because it is assumed that the Fed's inflation target is achievable in the absence of shocks and with appropriate monetary policy.3

Based on these considerations, it is no surprise that researchers and policymakers have devoted a great deal of effort to decomposing the unemployment rate into its trend (a notion of the natural rate) and its more transitory cyclical component (the deviation from the natural rate). Among the wide variety of modeling strategies that economists have deployed, a particularly interesting approach is to model the unemployment trends for various demographic groups defined by gender, education, and age. The estimated group trends are then combined with estimates of the demographic groups' labor force participation (LFP) rates and population shares to calculate an aggregate, economy-wide unemployment trend. This research approach is purely statistical and does not presuppose any relationship between inflation and deviations of unemployment from trend.

Two authors of this brief, Hornstein of the Richmond Fed and Kudlyak of the San Francisco Fed, build on this research in a recent working paper.4 According to their estimates, the trend U.S. unemployment rate declined steadily from 7.0 percent in 1976 to 4.7 percent in 2018. Moreover, they find that the decline in the aggregate trend rate has been driven almost exclusively by demographic changes — in particular, shifts to an older and more educated population as opposed to the changes in the trend unemployment rates of different demographic groups. They forecast that the trend unemployment rate will further decline to 4.6 percent this year and to 4.3 percent over the next ten years.

Demographics of the Labor Market: 1979 and 2018

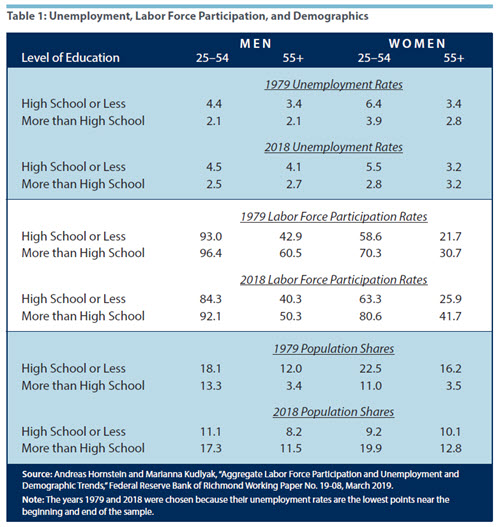

Hornstein and Kudlyak first discuss some of the major labor market changes that have taken place over the past forty years. Using microdata from the Current Population Survey, they calculate unemployment rates, labor force participation rates, and population shares for various demographic groups in 1979 and 2018. The resulting statistics are shown in Table 1 below, where the population is split into eight different groups based on divisions by age (twenty-five through fifty-four versus fifty-five and older), gender (men versus women), and education (high school or less versus more than high school).

The top panel illustrates that unemployment rates tend to be substantially lower for more educated workers and somewhat lower for older workers. Over time, the unemployment rate has increased for all categories of men but has declined for younger women. The middle panel shows that LFP rates are lower for less educated workers, for older workers, and for women. Between 1979 and 2018, LFP rates decreased for men and increased for women, independent of education and age, and the changes have been relatively large. The bottom panel shows that the population grew older between 1979 and 2018, with the share of those fifty-five and older increasing by about 7 percentage points. The population also has become more educated, with the share of those with more than a high school education increasing by about 30 percentage points.

Based on these data, the researchers address the question: What would have been the aggregate impact of the population's changing demographic composition on the trend unemployment rate and trend LFP rate, assuming no changes within each group? They find that the shift toward an older and more educated population tended to lower the aggregate unemployment rate. However, these demographic shifts had opposing effects on the aggregate LFP rate. The shift toward an older population tended to lower the aggregate LFP rate, while the shift toward a more educated population tended to increase the LFP rate.

The Empirical Framework

The authors contribute to an existing literature that has used age-cohort models of demographic groups to estimate aggregate trends for labor force participation and unemployment. One challenge for these models is that age-specific effects tend to shift over time. For example, older workers participate at higher rates in the labor market now than two decades ago; and young workers (sixteen to twenty-four) participate at a much lower rate than in the 1990s. To capture the evolution of these age effects, some researchers have used additional explanatory variables, such as school enrollment and Social Security payouts.5

Hornstein and Kudlyak, however, take an alternative approach that allows for time variation in age effects while being explicit about the stochastic processes that drive age and cohort effects. Moreover, they use educational attainment to define the demographic groups that they model, rather than including educational attainment as an additional explanatory variable.6

The authors estimate separate models for different demographic groups defined by gender and education. For example, they estimate one model for male high school graduates and another model for female college graduates. The model for each gender-education group assumes smooth local trends for the age and cohort effects. Each model also includes a common cyclical effect that impacts all age subgroups; however, the model allows the amplitude of the cyclical effect to vary across age subgroups. After estimating these models, the authors calculate the LFP and unemployment trends for various demographic groups defined by gender, education, and age.

To construct the projections of the aggregate unemployment and LFP trends, the authors' approach requires information on the projections of the size of demographic groups. For this purpose, the authors use Census Bureau (2018) population projections based on its "middle" assumptions for fertility, life expectancy, and net immigration levels. But this is not enough — it is also necessary to forecast the population's educational profile. For this purpose, the authors estimate a cohort-age model of educational attainment that they use to construct forecasts of the population's age-gender shares by education.

LFP and Unemployment Trends: Estimates and Forecasts

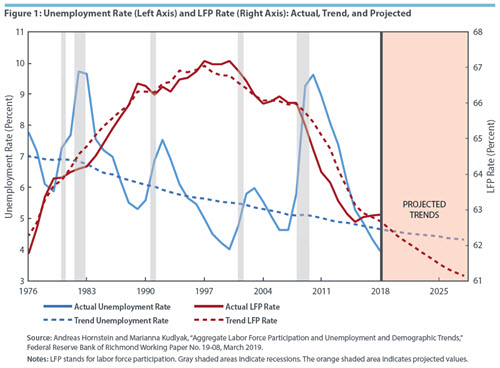

Figure 1 below shows actual, trend, and projected rates for LFP and unemployment. Focusing first on LFP, there is a hump-shaped pattern: the LFP rate increased from 1976 until 2000 and declined thereafter. Moreover, the LFP rate did not deviate much from the estimated trend — although LFP did decline relative to trend following the recessions of the early 1980s and in the aftermath of the financial crisis.

Trend LFP dynamics reflected a variety of underlying trends:

- Prior to 1990, the economy's overall LFP trend was boosted by an upward trend in the LFP rate of women. But this trend has since been reversed.

- Changes in the age distribution had a limited effect on the LFP rate prior to 2005, but since then, the aging population has lowered the aggregate LFP rate substantially.

- The population's increasing educational attainment tended to raise the trend aggregate LFP rate throughout the past forty years, but this tendency has been more than offset in recent years by the declining LFP rate of women and the impact of an aging population.

In 2018, the aggregate LFP rate was 62.9 percent — only 0.2 percentage points above the authors' trend estimate. The LFP rate is forecast to decline to 61.1 percent over the next ten years. The decline is largely due to Census Bureau forecasts of an increasingly aged population. This negative effect is forecast to be offset only partially by the positive impact of further increases in the population's educational attainment.

The aggregate unemployment trend is a weighted average of the various demographic groups' unemployment trends. In this calculation, the groups are weighted by their labor force shares, which in turn are determined by group population shares and group LFP rates.

Figure 1 shows a steady decline of the trend unemployment rate from 7.0 percent in 1976 to 4.7 percent in 2018.7 The authors find that the declining trend in the aggregate unemployment rate has been mostly attributable to an aging and more educated population. The average 2018 unemployment rate was 4.0 percent, about 0.7 percentage points below the authors' estimated trend. Their model projects that the trend unemployment rate will decline to 4.3 percent over the next ten years as the population continues to age and increase its educational attainment.

The authors' forecasts imply a lower rate of U.S. employment growth over the next ten years. Employment growth will be negatively impacted by lower forecast rates of population growth and LFP, and these negative effects will be offset only partially by the positive impact of a lower forecast unemployment rate. Assuming that productivity growth does not change, the decline in employment growth means a decline in GDP growth.

Marianna Kudlyak is a research advisor in the Research Department at the Federal Reserve Bank of San Francisco. Andreas Hornstein is a senior advisor and John Mullin is an economics writer in the Research Department at the Federal Reserve Bank of Richmond.

1

Board of Governors of the Federal Reserve System, "Federal Reserve Issues FOMC Statement of Longer-Run Goals and Monetary Policy Strategy," press release, January 25, 2012.

2

See Michael T. Kiley, "Low Inflation in the United States: A Summary of Recent Research," Board of Governors of the Federal Reserve System FEDS Notes, November 23, 2015.

3

Board of Governors of the Federal Reserve System, "Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents under their Individual Assessments of Projected Appropriate Monetary Policy," June 19, 2019.

4

See Andreas Hornstein and Marianna Kudlyak, "Aggregate Labor Force Participation and Unemployment and Demographic Trends," Federal Reserve Bank of Richmond Working Paper No. 19-08, March 2019.

5

For example, see Daniel Aaronson and Daniel Sullivan, "Growth in Worker Quality," Federal Reserve Bank of Chicago Economic Perspectives, Fourth Quarter 2001, vol. 25, no. 4, pp. 53–74.

6

This approach was taken by Joshua Montes in "CBO's Projection of Labor Force Participation Rates," Congressional Budget Office Working Paper 2018-04, March 2018.

7

The CBO puts its estimate of the natural rate of unemployment at 4.6 percent for 2018.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of their respective Reserve Banks or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us