Presidential Politics and Monetary Policy: Lessons from the 1896 Election

Economic Brief

February 2020, No. 20-02

The U.S. presidential election of 1896 provides an excellent natural experiment to measure the impact of exchange-rate uncertainty on bank balance sheets and the broader economy. The evidence suggests that the election's contentious free-silver debate significantly constrained banking activity and real economic activity by creating greater uncertainty about U.S. commitment to the gold standard. This finding reinforces the modern-day wisdom of insulating monetary policy from politics.

Historians view the U.S. presidential election of 1896 as a pivotal contest — both in political terms and in monetary terms, although it was impossible to separate those two realms in the late nineteenth century. Against the backdrop of a deep depression, monetary policy was a key issue, pitting "free silver" Democrat William Jennings Bryan against "gold standard" Republican William McKinley. More broadly, the issue divided the nation by pitting farmers against manufacturers, exporters against importers, and debtors against lenders.1 The monetary melee split both the Republican and Democratic parties, permeated American political discourse, and even spilled over into popular culture.2

At the Democratic convention, Bryan delivered a rousing oration in favor of bimetallism — expanding the money supply by increasing the value of silver relative to gold as legal tender. The Mint Act of 1792 pegged the U.S. dollar to both silver and gold at a ratio of 15 grains of silver to 1 grain of gold.3 And in 1834, Congress adjusted that ratio to roughly 16 to 1. But by the time of Bryan's speech, the actual value of gold relative to silver had doubled to 32 to 1, effectively driving silver coins out of circulation. Free-silver advocates wanted to revert to the 1834 ratio, which Bryan mistakenly called "the money of the constitution."

"When we have restored the money of the constitution all other necessary reforms will be possible," Bryan declared in his famous convention speech.4 He concluded by saying, "We shall answer their [Republicans'] demands for a gold standard by saying to them, you shall not press down upon the brow of labor this crown of thorns. You shall not crucify mankind upon a cross of gold."

The convention caught fire with enthusiasm. "Frantic men and women wildly waved handkerchiefs, canes, hats, and umbrellas," as one newspaper described the scene. "Some, like demented things, divested themselves of their coats and flung them high into the air."5 On the following day, the delegates gave Bryan the Democratic nomination.

Initially, McKinley was heavily favored to win the general election, partly because disaffected "Gold Democrats" had nominated their own candidate and partly because other Democrats had bolted to the Populist Party. But Bryan was a dynamic speaker and a tenacious campaigner. While McKinley stayed close to home and made "front porch" speeches to select groups of supporters, Bryan traveled more than 18,000 miles, delivering 600 speeches in just three months.6 The Populist Party and the Silver Party ultimately endorsed Bryan as well, and the election outlook became far less certain. And if the election was in doubt, so was America's commitment to the gold standard.

The Natural Experiment of 1896

The United States was technically on a bimetallic monetary standard until 1900, but the Coinage Act of 1873 made no provision for minting silver coins. As a result, only gold coins circulated widely.7 This condition spawned a "free-silver" political movement to bring silver coins back into circulation. One goal of the movement was to greatly expand the money supply, thus helping farmers obtain higher prices for their produce while servicing their debts with inflated dollars. In fairness to the farmers, the free-silver movement emerged during a period of trend deflation, so they likely were weary from repaying debts with deflated dollars. In a temporary victory, the movement spawned the Sherman Silver Purchase Act of 1890, which required the U.S. Treasury to buy large quantities of silver.8 Some economists have linked the depression that followed the panic of 1893 to the strain that those silver purchases put on the Treasury's gold holdings and the uncertainty they created regarding America's commitment to the gold standard.9 To allay fears of inflation, President Grover Cleveland convened a special session of Congress to quickly repeal the Sherman Silver Purchase Act,10 but the monetary debate continued to intensify — climaxing during the 1896 campaign.

McKinley won the presidency, a victory that boosted the credibility of the gold standard, but Bryan's dynamic campaign kept the election outcome in doubt until the end. After the election, an increase in domestic and global gold supplies reduced the economic rationale for free silver, but two authors of this Economic Brief (Fulford and Schwartzman) observe that the 1896 election was the clear breakpoint in the likelihood of a dollar devaluation relative to gold. Motivated by this insight, they exploit the election as a natural experiment for studying the effect of exchange-rate uncertainty on bank balance sheets and the broader economy.11

Fulford and Schwartzman examine balance sheet data for national banks in different states from 1880 through 1910.12 They take the cross-state pattern of balance sheet changes around the election as indicative of typical effects of shocks to currency-devaluation expectations. To explain the observed pattern, they develop an economic model in which variations in the expected exchange rate between dollars and gold affect bank balance sheets. They focus on data showing banks' leverage — defined as banks' ratios of debts to assets.13

Immediately after the election, overall banking activity (measured by levels of bank leverage) increased sharply, particularly in states where gold was more available and therefore more likely to be used for transactions by bank depositors. Fulford and Schwartzman show that those effects are consistent with a banking model in which banks have to compete for depositors' savings with assets denominated in other currencies. Moreover, the pattern they observe around the election appears to be similar to other important junctures when uncertainty around the gold standard was high, such as the Sherman Silver Purchase Act of 1890 or the panic of 1893.

The Credibility Index

To construct an index for the credibility of the gold standard, the researchers first assume that the only nationwide shock of importance around the time of the election was the change in commitment to the gold standard that occurred when McKinley won.14 They also assume that characteristics that make states more or less vulnerable to other macroeconomic shocks are uncorrelated with their exposure to the credibility of the gold standard.15

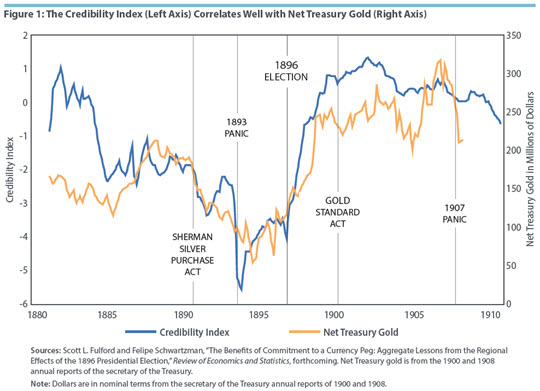

Given these key assumptions, the researchers estimate a factor model using seasonally adjusted changes in bank-leverage ratios. A factor model is a statistical framework constructed to explain a large number of observed variables by a small number of "factors" or "latent variables" that are unobserved. In this case, one might expect balance sheets of banks in all states to be simultaneously affected by the credibility of the gold standard and a few other variables of national relevance. There are well-established statistical techniques that allow researchers to separate the impact of such common factors from the impact of factors that are unique to each data series, such as changes in local economic conditions. The greater challenge is to identify a single latent variable — among the common factors — that could serve as a proxy for gold standard credibility. Fulford and Schwartzman employ the election (a single, well-defined event) for that purpose. Simplifying slightly, the intuition of their model works like this: if the election of 1896 marked a major resolution of uncertainty in favor of gold, then other time periods in which the cross-state bank-leverage pattern looks similar to that of 1896 would suggest similar movements in favor of gold. The resulting credibility index is depicted by the blue line in Figure 1.

The index is relatively volatile up to 1900, and then it becomes very stable. This large and abrupt reduction in volatility coincides with the passage of the Gold Standard Act, which increased the legal requirement and provided increased means for the Treasury to maintain the convertibility between the U.S. dollar and gold. The sudden reduction in index volatility also strongly indicates that changes in devaluation expectations played a key role in driving index volatility before 1900.

The index also exhibits strong movement around the Sherman Silver Purchase Act and the three-year period following the election. While the change in the index is positive at the time of the election, it is also noteworthy that it remains on a strongly positive path after the election. This continuing increase is associated with verification of large new gold reserves in Alaska and the increase in the global supply of gold from the growing adoption of the cyanide process of extraction. This correspondence to the historical narrative is further confirmed by the extent to which "free coinage" is mentioned in newspaper articles. The credibility index is most volatile during periods when this phrase most often appears. These historical narratives are buttressed by comparing the index to the amount of gold held by the Treasury over the years. (See Figure 1.) Higher gold reserves strengthen the Treasury's ability to defend the gold standard in the event of a speculative attack. Also, a perceived increase in the probability of an exit from the gold standard would be an incentive for people to exchange dollars for gold, thus reducing gold reserves at the Treasury.

The Impact of Imperfect Commitment

To evaluate the effects of imperfect commitment to the gold standard, Fulford and Schwartzman overlay their credibility index on their bank-leverage data. The two time series are highly correlated. There is no noticeable reduction in leverage following the Sherman Silver Purchase Act, but otherwise the two series share similar peaks and troughs. This correlation suggests that even if changes in commitment to gold do not fully explain all fluctuations in leverage from 1880 through 1910, they play a key role in the increase of bank leverage after 1896 and the reduction in volatility after 1900.

So imperfect commitment significantly constrained banking activity, but what was the impact on the real economy? To address this question, the researchers perform a structural vector autoregression analysis of the interaction between their credibility index and four measures of economic activity — business failures, pig-iron production, industrial production, and factory employment. Before 1900, using different identification approaches, the analysis finds significant reductions in three of the four measures of real economic activity. Raw industrial production is the only exception. Most notably, the analysis finds that fluctuations in commitment appear to account for 50 percent to 75 percent of the increase in business failures during the panic of 1893, which led to massive unemployment.

The researchers also apply this analysis to the years following 1900 as a placebo test. Eliminating shocks to commitment after 1900 does not change the volatility of real economic activity in amounts that are statistically significant. In other words, their credibility index matters when it should matter and doesn't matter when it shouldn't matter.

Interpreting the Results

The prospect of currency devaluation can be costly, even if the feared devaluation never occurs. In the case of the 1896 presidential election, Bryan's vigorous advocacy for free silver created a well-defined, one-time increase in uncertainty regarding the U.S. commitment to the gold standard. McKinley won the election, thereby restoring the credibility of the gold standard and preserving the value of the dollar, but the uncertainty created by the free-silver movement significantly restricted both financial activity and real economic activity during and following the panic of 1893.

One key difference between modern economies and the U.S. economy of the 1890s is the presence of central banks with the ability to set interest rates and "defend" currency pegs, even when foreign exchange reserves are lacking. In contrast, before the passage of the Gold Standard Act of 1900, when the Treasury's gold reserves were indeed running low, the Treasury had to obtain congressional authorization to issue bonds to replenish the reserves. This additional step — and continuing political intervention in the currency peg — contributed to the lack of credibility that prevailed before the Gold Standard Act of 1900, most notably during the 1893 crisis.16

Whether or not the gold standard was good monetary policy, this analysis highlights the costs of exchange-rate uncertainty, which illustrates the modern-day wisdom of keeping monetary policy free from political influence.

Scott L. Fulford is an economist at the Consumer Financial Protection Bureau. Karl Rhodes is a senior managing editor and Felipe Schwartzman is a senior economist in the Research Department at the Federal Reserve Bank of Richmond.

1

Many narratives boil the 1896 election down to inflation fears versus deflation fears, but some economists have suggested that the gold-silver debate was as much about the impact of the exchange rate on relative prices as it was about the impact of the exchange rate on the overall price level. See Jeffry A. Frieden, "Monetary Populism in Nineteenth-Century America: An Open Economy Interpretation," Journal of Economic History, June 1997, vol. 57, no. 2, pp. 367–395.

2

Some historians and economists have suggested that The Wonderful Wizard of Oz, written in 1900, contains many allegorical references to the bimetallic debate. "Not understanding the magic of the Silver Shoes, Dorothy walks the mundane — and dangerous — Yellow Brick Road," noted Henry M. Littlefield in "The Wizard of Oz: Parable on Populism," American Quarterly, Spring 1964, vol. 16, no. 1, p. 53. Of course, Dorothy's silver shoes became famously ruby red in the 1939 movie version. Also, see Hugh Rockoff, "The 'Wizard of Oz' as a Monetary Allegory," Journal of Political Economy, August 1990, vol. 98, no. 4, pp. 739–760.

3

See U.S. Mint, "Coinage Act of April 2, 1792," Section 9. The law equated one dollar to 371.25 grains of "pure" silver or 24.75 grains of "pure" gold. The value of one silver dollar is explicit in the act, but the value of one gold dollar must be calculated by dividing the grains prescribed for a gold eagle by ten or dividing the grains prescribed for a gold half eagle by five.

4

Official Proceedings of the Democratic National Convention Held in Chicago, Illinois, July 7–11, 1896, Logansport, Indiana: Wilson, Humphreys & Company, 1896, pp. 226–235.

5

"Boy Orator of the Platte Carries the Convention by Storm," Omaha Daily Bee, July 10, 1896.

6

See Michael Kazin, A Godly Hero: The Life of William Jennings Bryan, New York: Anchor Books, 2006. Also, see Lewis L. Gould, "William McKinley: Campaigns and Elections," University of Virginia Miller Center website, accessed in January 2020.

7

Milton Friedman and Anna Jacobson Schwartz, A Monetary History of the United States, 1857–1960, Princeton: Princeton University Press, 1963, pp. 114–115.

8

Friedman and Schwartz (1963), p. 133.

9

See Friedman and Schwartz (1963), pp. 133–134, and Oliver Mitchell Wentworth Sprague, History of Crises under the National Banking System, Washington, D.C.: Government Printing Office, 1910, p. 179.

10

Mitchell Bard, "Ideology and Depression Politics I: Grover Cleveland (1893–97)," Presidential Studies Quarterly, Winter 1985, vol. 15, no. 1, pp. 82–83.

11

See Scott L. Fulford and Felipe Schwartzman, "The Benefits of Commitment to a Currency Peg: Aggregate Lessons from the Regional Effects of the 1896 President Election," Review of Economics and Statistics, forthcoming.

12

Fulford and Schwartzman find similar trends in readily available state bank data.

13

Focusing on leverage allows the researchers to make reasonable comparisons to changes in bank activity across different states that have banking sectors of very different sizes and growth rates. Leverage measures exclude the bonds required to secure circulation of national bank notes. This approach removes the direct note-circulation function of national banks of the time period to make them more comparable to modern banks.

14

Fulford and Schwartzman use narrative evidence to consider and rule out several other factors from October 1896, such as financial disturbances, a newspaper story about gold in Alaska, reports of crop failures in India, and policy uncertainty over tariffs generated by differences in major party platforms.

15

The authors find only weak correlations between their cross-section of state-level leverage changes around the 1896 election and leverage changes around other key dates.

16

Fulford and Schwartzman, forthcoming.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond, the Federal Reserve System, or the Consumer Financial Protection Bureau.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us