Bank Lending in the Time of COVID

Economic Brief

February 2021, No. 21-05

We discuss the evolution of bank lending during the first several months of the COVID-19 pandemic. Large domestic banks and foreign-related banks increased significantly their lending to businesses during these months, much of it through existing lines of credit. Small domestic banks played an active role in providing paycheck protection loans. In terms of consumer credit, the stock of banks' residential mortgage loans did not change substantially, and the amount of bank credit flowing directly to consumers decreased.

In March 2020, when the COVID-19 pandemic hit the economy, the U.S. banking system was in strong financial condition following a decade-long process of recapitalization and improvements in liquidity planning.1 In the first several months of the pandemic, banks were able to provide a significant amount of new credit, particularly to firms, according to weekly data collected by the Federal Reserve on a representative sample of banks. This flow of credit helped businesses confront what was initially perceived to be a relatively short-lived shock.

C&I Loans

The largest increases occurred in C&I loans, which are loans (secured or unsecured) to business enterprises, including working capital advances and loans to individuals to start a business. Bank lending accounts for around 20 percent of the total credit extended to firms of all sizes and is often the only type of credit available to smaller firms. Many firms borrowed during this time to build up their cash buffers,4 perhaps because of increased uncertainty and stress in short-term funding markets.

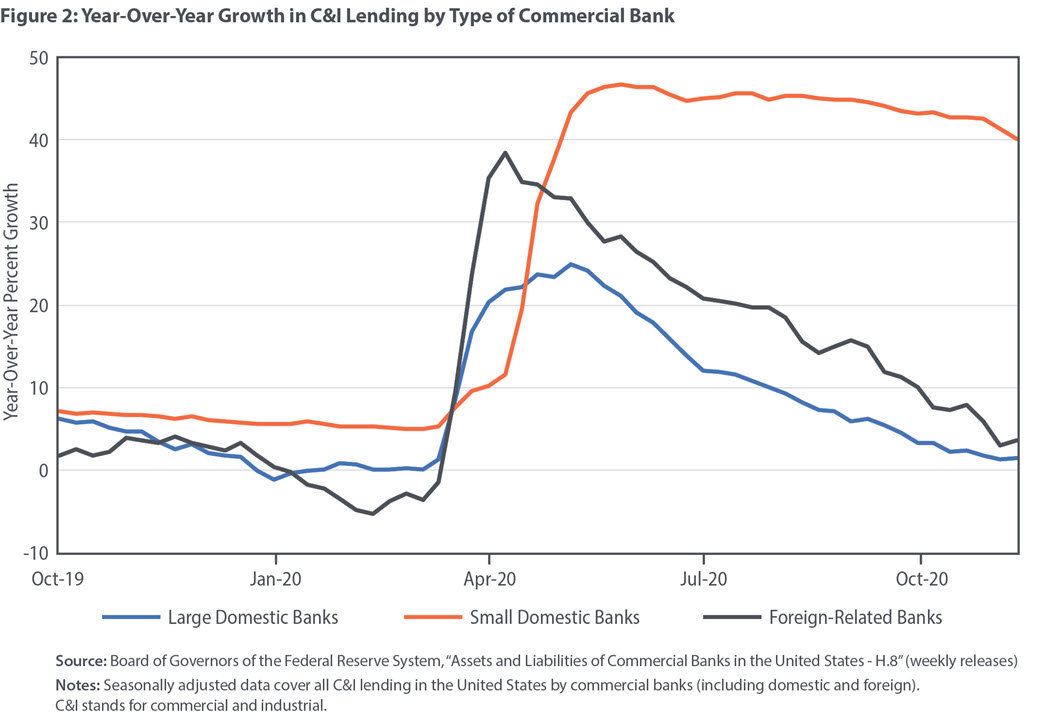

Figure 2 shows that large domestic banks and foreign-related institutions increased C&I lending sharply (between 20 percent and 40 percent of their lending during the same week of the previous year) in early March, and it remained high for a few weeks. Foreign banks started to decrease C&I lending in mid-April, and large domestic banks started to decrease it in mid-May. Small domestic institutions increased their lending later, toward the end of April and the beginning of May, to greater than 45 percent of their previous year’s lending. For these smaller institutions, the level has remained persistently high. It is important to keep in mind, though, that their total lending amounts to only about 50 percent of that of large banks.

An important mechanism driving the increase in loans to businesses during the early stages of the pandemic was businesses drawing down existing lines of credit.5 (This also occurred at the onset of the 2008 global financial crisis.)6 After the initial spike in credit line drawdowns, the surge in C&I lending was fueled by participation in the Paycheck Protection Program (PPP).7 Banks started lending under the PPP on April 13, 2020, and PPP activity stayed high for several months. The program closed Aug. 8 with more than 5 million loans for a total of $525 billion lent through 5,460 participating institutions (banks, savings and loans, as well as other entities). The average loan size was $100,729.

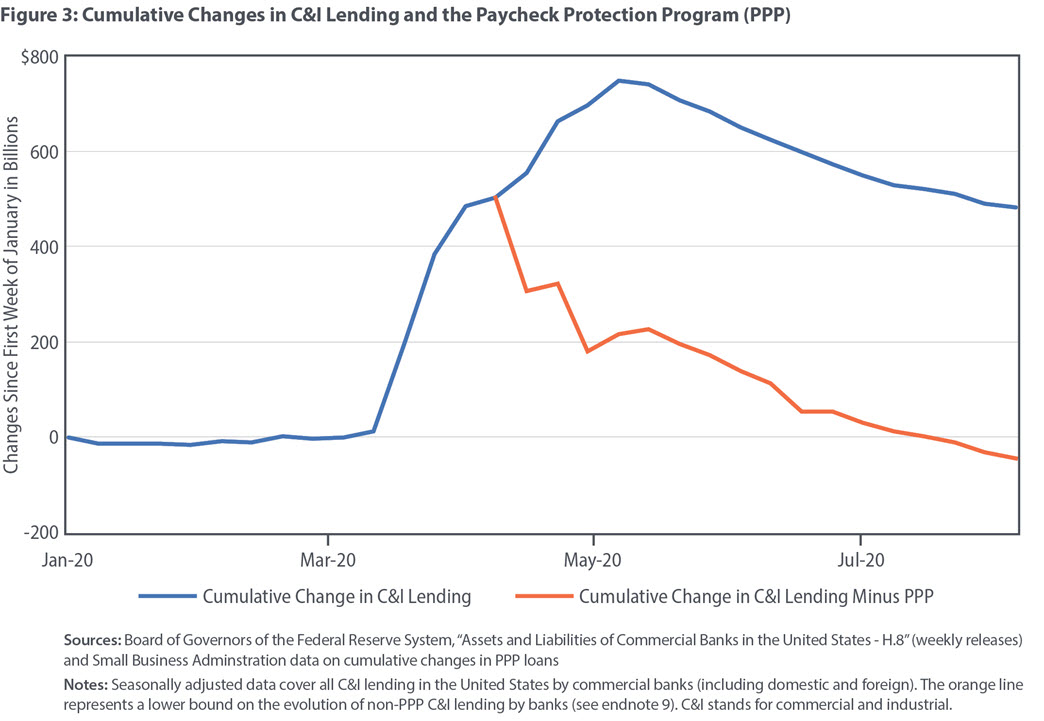

Figure 3 combines H.8 data on cumulative changes in C&I bank loans with data from the Small Business Administration (SBA) on cumulative changes in PPP loans.8 Once PPP loans were available, it appears that very few new non-PPP loans were made, and many outstanding ones were repaid.9 Indeed, there is evidence that once smaller firms had access to PPP loans, they significantly reduced their non-PPP bank loans.10 This evidence suggests the terms of the government-sponsored loans were more advantageous for small firms.

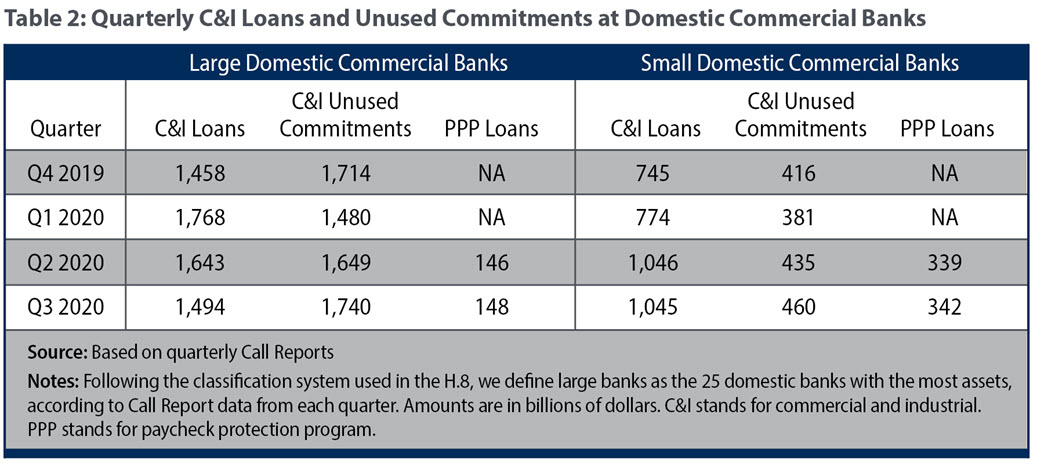

Table 2 looks more closely at changes in C&I lending. At large domestic banks, the increase in C&I lending in the first quarter of 2020 ($310 billion) corresponds closely with the drop in unused credit lines ($234 billion), consistent with the idea that credit line drawdowns were a major source of increased C&I lending. At smaller banks, unused commitments actually fell more than the increase in C&I loans during the first quarter of 2020, perhaps because some credit lines were canceled or discontinued.

In the second quarter of 2020, C&I loans by large banks dropped even though large banks originated $146 billion in PPP loans, which indicates an even more significant drop in non-PPP C&I lending. For small domestic banks, the dramatic increase in PPP loans was commensurate with the increase in C&I loans. Interestingly, by the third quarter of 2020, when the growth in PPP loans stopped (the program ended on Aug. 8), total C&I lending by large domestic banks continued to fall, and unused commitments returned (approximately) to their level before the pandemic started. At smaller banks, C&I lending leveled out, but did not fall, after PPP lending stopped growing.

Some of the decrease in C&I loans observed during the second and third quarters of 2020 likely resulted from many businesses repaying the loans that originated from lines of credit in March and April. Repayments on PPP loans, on the other hand, were not very significant during that time. As of Nov. 22, 2020, the SBA website reported that loans totaling $38 billion have been repaid, and loans totaling $83 billion have been submitted for forgiveness.

Another factor that is likely to have influenced lending trends during this period was that banks responded by tightening lending standards as the pandemic continued.11 Researchers have established a connection between credit line drawdowns and tighter term lending: Banks that had their credit lines more intensively tapped early in the pandemic (typically by large corporations) tightened their term lending to other borrowers to a greater degree.12 It is also worth noting that the quality of C&I loans in banks’ portfolios deteriorated noticeably in the second and third quarters of 2020, as reported in the November Financial Stability Report of the Board of Governors of the Federal Reserve System, with borrower leverage at historic highs.

Real Estate Loans

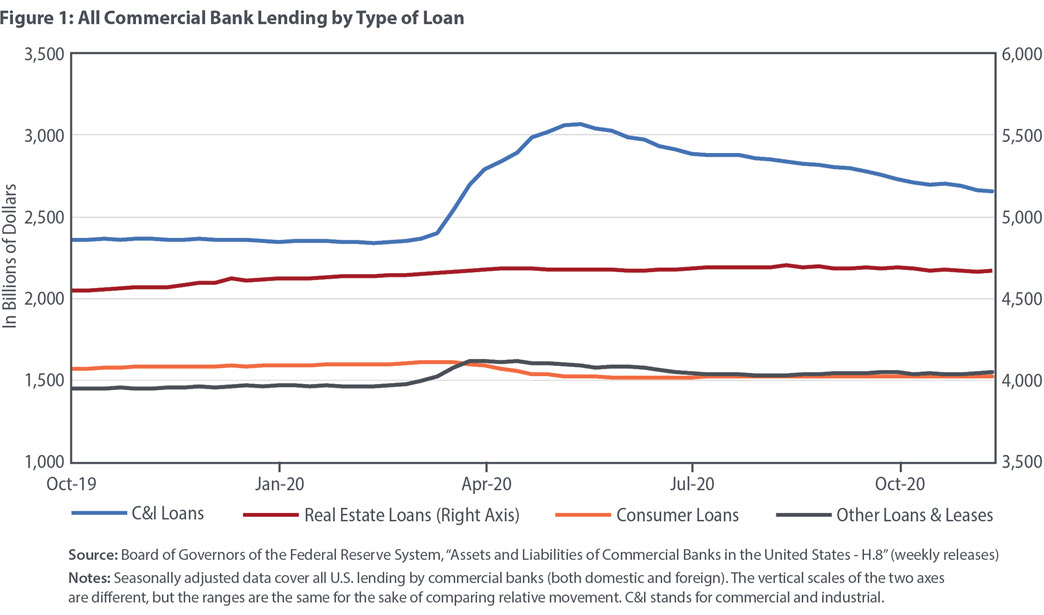

As seen in Figure 1, the crisis did not affect total real estate loans in any significant way. When we disaggregate this category into its two main subcategories, residential and commercial, and also between large and small domestic commercial banks, we find very similar behavior (not shown in the figure).13

This may be surprising given that, on one side, the residential housing sector has been booming for much of the pandemic, and on the other side, loans linked to commercial real estate could suffer more acutely from the effects of lockdowns and other government-imposed restrictions on business activity.14 Such effects, however, are not evident in these data — if anything, it seems that the recent stock of residential real estate loans was relatively sluggish compared with commercial real estate lending.

Several factors may underpin these patterns. Much of the lending activity on the residential side was associated with mortgage refinancing, where one loan replaces another. Furthermore, banks sell a significant proportion of the new mortgages that they originate, and more than half of new mortgages originated year-to-date have been granted by nonbank originators (recall that the H.8 data only cover depository institutions).15 On the commercial real estate side, it is possible that weakness in some sectors (hotels, offices and shopping centers) is countered by strength in others (construction and warehousing), leaving the aggregate largely unaffected.

Arguably, the main change in real estate lending has been the deterioration of commercial borrowers’ credit worthiness. This is the natural consequence of weakened consumer spending in some sectors, which has translated into rental income declines and increased vacancies, especially in COVID-affected properties, such as hotels and retail establishments.16 On the residential side, while mortgage refinancing activity (which tends to improve the average credit score of borrowers) has been strong due to low interest rates, a significant portion of mortgages also is participating in government-sponsored loss-mitigation programs. For more details, see the Financial Stability Report issued by the Federal Reserve in November 2020.

Consumer Loans

Figure 1 shows that consumer loans fell in March and April and remained low for several months. To better understand these patterns, we take a more disaggregated look at consumer loans.

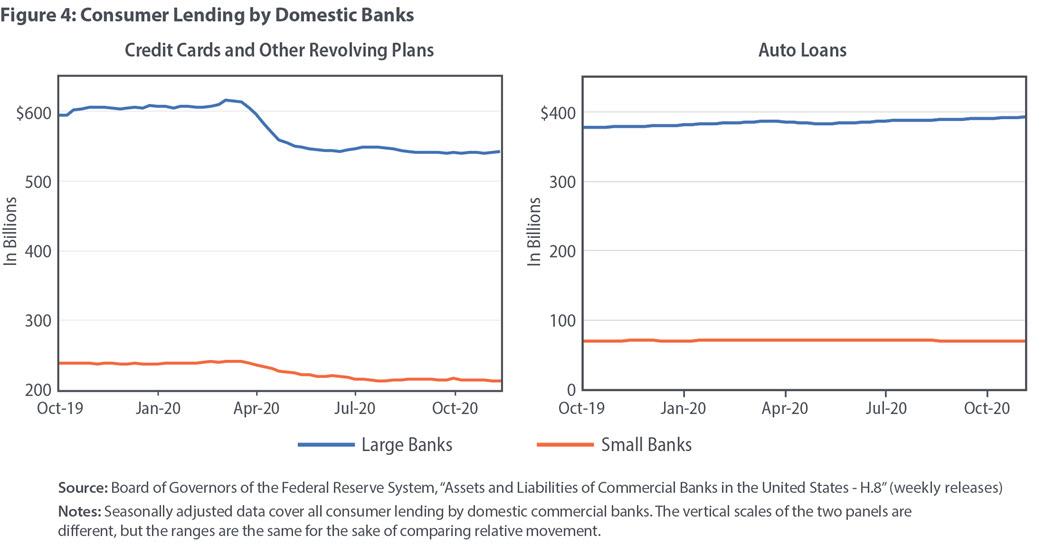

Credit card loans and auto loans are the two main categories of consumer lending. Figure 4 shows that credit card loans decreased at large and small domestic institutions, with the lion’s share of the dollar-volume decline occurring in large banks. Auto loans made by large banks also dropped some in March and April but then started growing again.17 Smaller banks make far fewer auto loans, and their lending in that market has not been affected noticeably by the pandemic.

On the supply side, in both the April and July Senior Loan Officer Opinion Survey (conducted by the Federal Reserve), banks reported tighter lending standards on all categories of consumer loans. For example, banks reported reduced credit limits on new credit cards and increased basic requirements to obtain new cards. Credit standards on auto loans, such as the maximum loan maturity or the minimum credit score required to obtain a loan, tightened as well.

Banks also experienced weaker demand for consumer loans, which could have multiple origins. For example, at the beginning of the pandemic, car sales dropped significantly — partly due to strict lockdowns, increased unemployment and the uncertainty experienced by prospective buyers.18 Another source of weaker demand is the combination of restrictions in access to certain services and the significant government transfers received by households. These likely reduced the need to accumulate credit card balances and, in many cases, even allowed consumers to pay down previously accumulated credit card debt.19

All Other Loans

This category includes loans from banks to nondepository financial institutions and all other loans, such as loans to banks in foreign countries, loans to finance agricultural production and loans to purchase securities. As seen in Figure 1, the overall pattern for these loans was comparable to that of C&I loans, although the changes were less abrupt. Most of the sharp increase in other loans happened early in the pandemic and came from an increase (of more than 30 percent) in loans to nondepository financial institutions.20 Much of this increase resulted from drawdowns on existing lines of credit and was concentrated in large banks' and foreign banks' portfolios.21 In this sense, the behavior of other loans resembles the behavior of C&I loans excluding PPP activity.

Allowance for Credit Losses

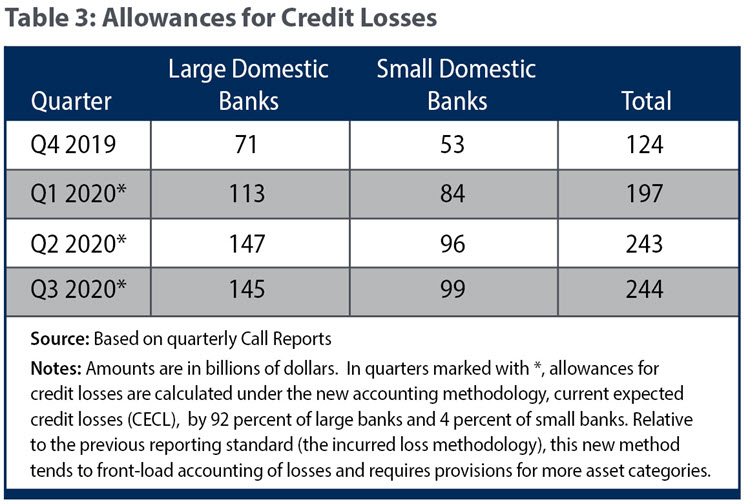

Banks are required to put aside funds ("provisions") to cover expected losses on their loans and securities. The cumulative balance of these provisions is a bank's allowance for credit losses. Call Report data suggest that banks started increasing their allowances in March.22 This confirms that banks increased their expectations of potential loan defaults. It also implies that banks will be prepared to withstand these losses, if and when they materialize, while maintaining their regulatory capital requirements.23

As shown in Table 3, Call Reports indicate that allowances nearly doubled between the fourth quarter of 2019 and the second quarter of 2020 and remained flat through the third quarter of 2020. Note that out of the $244 billion of credit allowances in the third quarter, $35 billion — $21 billion at large banks and $14 billion at small banks24 — can be attributed to the adoption of a new accounting methodology, current expected credit losses (CECL), that requires more aggressive provisioning. This implies that, out of the cumulative $119 billion increase in allowances through the third quarter of 2020, $85 billion is attributable to deteriorating loan repayment expectations ($54 billion for large banks and $31 billion for small banks).

1

Randal K. Quarles, "What Happened? What Have We Learned From It? Lessons From COVID-19 Stress on the Financial System," Speech at the Institute of International Finance, Washington, D.C., October 15, 2020.

2

The H.8 weekly releases estimate aggregate data for all domestically chartered commercial banks and U.S. branches and agencies of foreign banks from a weekly survey of a representative sample of banks. Estimates for the entire U.S. banking industry are constructed by benchmarking the survey data to the Call Report data filed by all banks at the end of each quarter. Our sample period includes data through November 2020.

3

We follow the H.8 definition of "large" — the 25 domestic banks with the most assets, according to Call Report data from the quarters before the measurement weeks. As of December 2013, the asset-size threshold for inclusion in the large-bank panel was approximately $85 billion.

4

Viral V. Acharya and Sascha Steffen, "The Risk of Being a Fallen Angel and the Corporate Dash for Cash in the Midst of COVID," Review of Corporate Finance Studies, November 2020, vol. 9, no. 3, pp. 430–471.

5

Banks report their lines of credit (unused loan commitments) in the quarterly filing of balance sheet data required by regulatory agencies, i.e., the Call Reports. Most business lines of credit, when drawn down, become C&I loans. See Gabriel Chodorow-Reich, Olivier Darmouni, Stephan Luck and Matthew Plosser, "Bank Liquidity Provision Across the Firm Size Distribution," Federal Reserve Bank of New York Staff Report No. 942, October 2020, for evidence that the increase in non-PPP loans to businesses during the first and second quarters of 2020 came almost entirely from drawdowns by large firms on precommitted lines of credit. Also, see Lei Li, Philip E. Strahan and Song Zhang, "Banks as Lenders of First Resort: Evidence From the COVID-19 Crisis," Review of Corporate Finance Studies, November 2020, vol. 9, no. 3, pp. 472–500; Acharya and Steffen, "The Risk of Being a Fallen Angel and the Corporate Dash for Cash in the Midst of COVID;" and Daniel L. Greenwald, John Krainer and Pascal Paul, "The Credit Line Channel," Federal Reserve Bank of San Francisco Working Paper No. 2020-26, November 2020.

6

See, for example, Victoria Ivashina and David Scharfstein, "Bank Lending During the Financial Crisis of 2008," Journal of Financial Economics, September 2010, vol. 97, no. 3, pp. 319–338. Early on during the health crisis, before much data was available about changes in bank credit or government emergency programs, Viral V. Acharya and Sascha Steffen, "'Stress Tests' for Banks as Liquidity Insurers in a Time of COVID," Voxeu.org, March 22, 2020, used data from nonfinancial firms' credit line drawdowns during the 2008 crisis to estimate an expected $264 billion increase in C&I loans in response to the pandemic. Based on this estimate, the pace of credit line drawdowns recently was much more pronounced than in 2008. For the original study of credit line drawdowns during the 2008 crisis, see Tobias Berg, Anthony Saunders, Sascha Steffen and Daniel Streitz, "Mind the Gap: The Difference Between U.S. and European Loan Rates," Review of Financial Studies, March 2017, vol.30, no. 3 pp. 948–987.

7

The PPP was created by the CARES Act to incentivize small businesses with fewer than 500 employees to keep workers on payroll during the pandemic. Under this program, a participating financial institution makes a two-year, uncollateralized loan at a 1 percent interest rate to a qualified small business; the Small Business Administration provides guarantees and possibly forgiveness of the loan if certain conditions are met. While other nonbank financial institutions could offer PPP loans, banks played a significant role in the program. See João Granja, Christos Makridis, Constantine Yannelis and Eric Zwick, "Did the Paycheck Protection Program Hit the Target?" National Bureau of Economic Research Working Paper No. 27095, Revised November 2020.

8

Note that the SBA reports net loan balances through Aug. 8, 2020.

9

Note that PPP loans are not exclusively granted through banks, and hence the C&I excluding PPP loans is a lower bound on non-PPP C&I lending. Banks report PPP loans as a special item in their Call Reports, but not on the weekly H.8 survey. Based on Aug. 8, 2020, statistics provided by the SBA and the Call Report data on PPP loans, nonbank institutions may have granted between $18.9 billion and $35 billion out of the total $525 billion.

10

Gabriel Chodorow-Reich et al. (2020).

11

See the April and July 2020 Senior Loan Officer Opinion Survey (SLOOS) conducted by the Federal Reserve.

12

Greenwald, Krainer and Paul (2020).

13

Foreign-related institutions do not have large portfolios of real estate loans, with under $100 billion as an aggregate. Furthermore, as with the other types of banks, this component of foreign banks' portfolios was not significantly impacted by the pandemic.

14

On the residential side, for example, the New York Fed Quarterly Report on Household Debt and Credit states that, in the third quarter of 2020, mortgage debt increased by $85 billion, a good pace of growth. The volume of mortgage originations, which includes refinances, was especially strong, with over $1 trillion in loans.

15

See Ben Eisen, "Mortgage Originations Are on Pace for Best Year Ever," WallStreetJournal.com, December 10, 2020.

16

See, for example, Jim Dobbs, American Banker, "Hotel Lending: Banks in 'Race Against Time,'" November 23, 2020.

17

Much of the growth in lending to consumers, including residential mortgages and auto loans, has been concentrated in the prime credit segment, with almost no growth in lending to less creditworthy borrowers, according to the Fed's Financial Stability Report of November 2020.

18

Zhu Wang, "Coronavirus and Auto Lending: A Market Outlook," Federal Reserve Bank of Richmond Report on the Economic Impact of COVID-19, April 16, 2020.

19

This situation has been widely reported in the business press. See, for example, Robert Armstrong, "Bank Credit Card Profits in Question as U.S. Consumers Pay Down Debt," Financial Times, November 15, 2020.

20

A possible source for this increase is borrowing by nonbank mortgage originators, who fund their origination with warehouse lines of credit from large banks, which they then pay off when they sell the loans in the securitization market.

21

See, for example, the Federal Reserve's May and November 2020 Financial Stability Reports.

22

The H.8 data tell a similar story, although they need to be interpreted with caution due to changes in accounting methodology over the time period.

23

The increase in allowances from the start of the pandemic through the third quarter of 2020 amounts to approximately 0.5 percent of total assets. Note that, since PPP loans are guaranteed by the SBA, banks do not need to provision for these loans.

24

Upon adoption, banks provided in their Call Reports the one-time impact that the new CECL accounting rule had on their credit allowances (both for loans and for other securities that were not subject to provisions under the old accounting methodology).

25

Li, Strahan and Zhang (2020).

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us