Coronavirus and Auto Lending: A Market Outlook

Special Report

April 16, 2020

The coronavirus pandemic has caused an unprecedented economic crisis in the United States (and globally). Many market sectors are bearing the pain, with the trillion-dollar auto lending industry being no exception. As massive layoffs take place and consumer confidence plunges, players in the auto lending market face increasing challenges.

Market Background

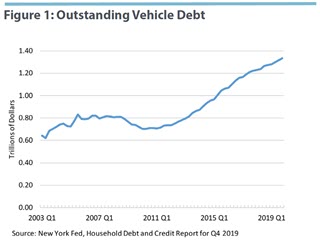

Prior to the coronavirus outbreak, the U.S. auto lending market had grown quickly over the past decade. According to the New York Fed's Household Debt and Credit Report for Q4 2019, outstanding vehicle debt increased by 68 percent between the fourth quarter of 2008, when Americans owed $791 billion, and the fourth quarter of 2019, when they owed $1.33 trillion. (See Figure 1 below.)

Coronavirus Impact

The coronavirus crisis could have large negative effects on auto lending, hurting both borrowers and lenders. The impact is likely to channel through rising default of existing loans and falling issuance of new loans.

- Impact on Loan Default

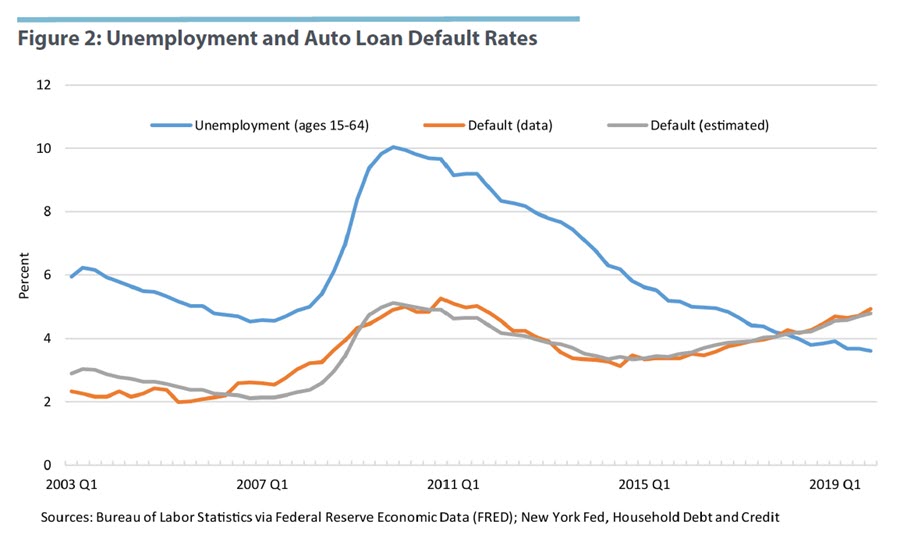

Historically, auto loan defaults, defined as becoming 90 or more days past due, tend to correlate with unemployment. Since 2014, however, the default rate has picked up despite the continuing decline in unemployment, which suggests the increase in defaults is driven by other causes (see chart below)2. As of the fourth quarter of 2019, the auto loan default rate climbed to 4.94 percent, close to the peak level of 5.27 percent that followed the Great Recession.

A back-of-the-envelope calculation can provide a first-order approximation of the impact of the coronavirus crisis on auto loan defaults. To do so, we assume that the correlation between unemployment and auto loan default stays constant over time, and we use a post-2013 time trend to capture the extra increase in the default rate since 2014. A simple linear regression shows that the estimated default rate matches the data pretty well.3

The estimation shows that a 1 percent increase in unemployment may lead to 0.54 percent increase in auto loan defaults, and the post-2013 time trend adds a 0.13 percent increase in default each quarter forward.

Therefore, if we assume that the unemployment rate rises to 10 percent (i.e., the peak level during the Great Recession) in the second quarter of 2020, the auto loan default rate would rise to 8.53 percent. This roughly corresponds to an increase of $47.75 billion in defaulted loans (i.e., $1.33 trillion x (8.53% - 4.94%) = $47.75 billion).

If the unemployment rate instead rises to 20 percent, the auto loan default rate would rise to 13.96 percent, an increase of $119.97 billion in defaulted loans. In an even more severe scenario, if the unemployment rate rises to 30 percent, the auto loan default rate would rise to 19.38 percent, an increase of $192.05 billion in defaulted loans.4

- Impact on Borrowers

A large number of U.S. consumers take out auto loans: Auto loan accounts totaled 116 million in the fourth quarter of 2019. The median credit score of auto loan borrowers at the time they originated a loan has been above 650 since 2004, but more than 10 percent of borrowers had a credit score below 600. If defaults on auto loans increase significantly, many consumers may lose their vehicles and may face difficulties getting to work and supporting their families.

- Impact on Lenders

The coronavirus shock also affects auto loan lenders, and the relative impact is likely to be related to market shares. Recent data show that banks have the highest market share, making 35.9 percent of total (new and used) auto loans. Captive lenders (i.e., subsidiaries of the automakers) follow closely, taking 34.8 percent of the market. The shares of credit unions and financial companies rank third and fourth, at 19.5 percent and 8.5 percent, respectively.

Taking as given the market share of each lender type, we consider a simple thought experiment. As projected above, if the unemployment rate rises to 20 percent, the auto loan default rate would rise to 13.96 percent, an increase of $119.97 billion in defaulted loans. Allocating this amount to each lender type according to their market share, this would suggest an increase of $43 billion defaulted loans for banks and $23.4 billion for credit unions.5

As another thought experiment, we consider a case in which all borrowers are allowed to defer their repayment for two months. This would likely delay loan repayments for a total of roughly $59.1 billion6. Allocating this amount according to market shares, we estimate that banks would bear $21.22 billion of the delayed payment and credit unions $11.52 billion.

Another channel by which the coronavirus crisis could hit auto loan lenders is through the falling issuance of new loans. As of the fourth quarter of 2019, about 58 percent of the total (new and used) auto sale values were financed by auto loans. Because of the coronavirus pandemic, auto sales have plummeted. In March 2020, U.S. auto sales plunged to their lowest level in almost 10 years, according to Standard & Poor's. Sales on a seasonally adjusted, annualized basis were 32 percent lower than in February7. As a result, lenders may face not only higher default on existing loans, but also lower issuance of new loans and lower fee income.

It is worth mentioning that the amount of securitized auto loans (ABS) has been rising in recent years. The total reached $250 billion in 2019, representing 18.8 percent of total auto loans outstanding. Considering most auto loans are not securitized, the pain of bad loans will fall largely on the borrowers and their direct lenders. That said, within auto ABS, the share collateralized by subprime borrowers (i.e., borrowers with lower than mid-600 FICO scores) has been rising and reached almost 24 percent of total auto ABS outstanding in the first quarter of 2019. Because subprime borrowers typically have less ability to weather unexpected financial shocks, the performance of subprime auto ABS warrants a close watch.

Policy Responses

In response to the coronavirus shock, policymakers have taken major steps to mitigate the impact. In addition to all the fiscal and monetary easing policies, some measures are targeted directly at supporting the functioning of consumer credit markets, including auto lending.

Federal and state banking regulators have encouraged financial institutions to work constructively with borrowers affected by COVID-19. In fact, many auto lenders are now offering forbearance that allows borrowers to defer their payments. In support of these efforts, regulators will not categorize such loan modifications as troubled debt restructurings.

Meanwhile, the Federal Reserve has established emergency lending facilities to support the flow of credit to consumers and businesses. Specifically, the Term Asset-Backed Securities Loan Facility supports the issuance of asset-backed securities backed by certain types of consumer loans, including auto loans.

Conclusion

The auto lending market faces great challenges as the coronavirus pandemic continues to disrupt the U.S. economy. Rising loan default and falling auto sales and loan issuance loom large down the road. These developments will receive close monitoring by market participants and policymakers.

Zhu Wang is vice president for research in financial and payments systems in the Research Department at the Richmond Fed.

1

Jenn Jones, "Auto Loan Statistics 2020," LendingTree, January 10, 2020.

2

According to recent research from the Philadelphia Fed, the jump in the default rate following 2014 is largely attributed to nonspecific, year-of-origination effects, rather than to factors identifiable by borrowers’ observed characteristics. Factors not directly observed, such as changes in the balance sheet and liquidity characteristics of the borrowing population, could have propelled this trend. See Paul Calem, Chellappan Ramasamy, and Jenna Wang, "What Explains the Post-2011 Trends of Longer Maturities and Rising Default Rates on Auto Loans?" Federal Reserve Bank of Philadelphia Discussion Paper 20-02, April 2020.

3

The quarterly unemployment rate (seasonally adjusted) is from the Bureau of Labor Statistics via the FRED dataset hosted by the St. Louis Fed. The auto loan default rate (defined as percent of balance 90+ days delinquent) is from the New York Fed's Household Debt and Credit Report for Q4 2019.

4

According to the latest news reports, Goldman Sachs expects the U.S. unemployment rate to reach 15 percent by mid-2020, while JPMorgan forecasts the unemployment rate to be 20 percent in April. A recent St. Louis Fed blog post estimates that the U.S. unemployment rate could rise to 32.1 percent in the second quarter of 2020. See Miguel Faria-e-Castro, "Back-of-the-Envelope Estimates of Next Quarter's Unemployment Rate," Federal Reserve Bank of St. Louis On the Economy blog, March 24, 2020.

5

In the fourth quarter of 2019, the total equity capital was $1,966 billion for commercial banks and $178.6 billion for credit unions. Therefore, the increased defaulted loans would count for 2.2 percent of equity capital for banks and 13.1 percent for credit unions. Auto lenders typically rely on vehicle repossessions to limit their losses from defaults, but used car prices are widely expected to fall due to the coronavirus crisis, which would make the loss recovery more difficult.

6

The calculation is based on the assumption that the average monthly auto loan payment is $500, and the number of total auto loans equals the total loan value outstanding in the fourth quarter of 2019 ($1.33 trillion) divided by the average loan amount in April 2019 ($22,503).

7

See Kevin Wack, "How the Coronavirus Crisis Is Upending Auto Lending,"American Banker, April 8, 2020.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.