Why Do People Save During Retirement?

Economic Brief

September 2021, No. 21-32

Economic theory predicts that people will accumulate savings during their working years and deplete those savings during retirement in order to smooth consumption over their lifetime. But retired singles tend to deplete their assets very slowly, and retired couples tend to accumulate assets as they age. Research points to two reasons why households are slow to decumulate their assets: (i) the need to prepare for uncertain end-of-life medical expenses and (ii) the desire to bequeath assets to surviving family members after death. This Economic Brief shows that the interaction between these two motives is a crucial determinant of saving behavior for all retirees.

Why do households save after retirement? Previous studies — such as our 2018 working paper "End-of-Life Medical Expenses," with co-authors Elaine Kelly and Jeremy McCauley — have found that covering future medical expenses is an important reason, as end-of-life medical care is often expensive and unpredictable. Additional studies have found that the desire to leave bequests to survivors is also an important savings motive.1

Most of the research on this topic has focused on the behavior of single retirees, but much less is known about what drives retired couples to save. There are key ways couples differ from singles regarding saving needs:

- They can pool medical expense risks and potentially reduce medical spending by caring for one another rather than using paid care.

- Each member of the couple is exposed to the income loss and the high medical expenses that often accompany a spouse’s death.

- Each member of a couple cares about leaving resources to the surviving spouse in addition to bequests to other heirs.

Understanding the saving motivations of retired couples is important, as they account for roughly half of people age 70 and older. Better understanding these motivations can help policymakers predict how retirees would react to various policy changes. In this Economic Brief, we examine the effects of potential medical expenses and bequest motives on saving after retirement and discuss potential policy impacts.

Wealth Trends Among Retired Households

Starting in 1993-94 and continuing every two years after, the Asset and Health Dynamics Among the Oldest Old (AHEAD) dataset — part of the Health and Retirement Study — has collected information on individuals age 70 and older.

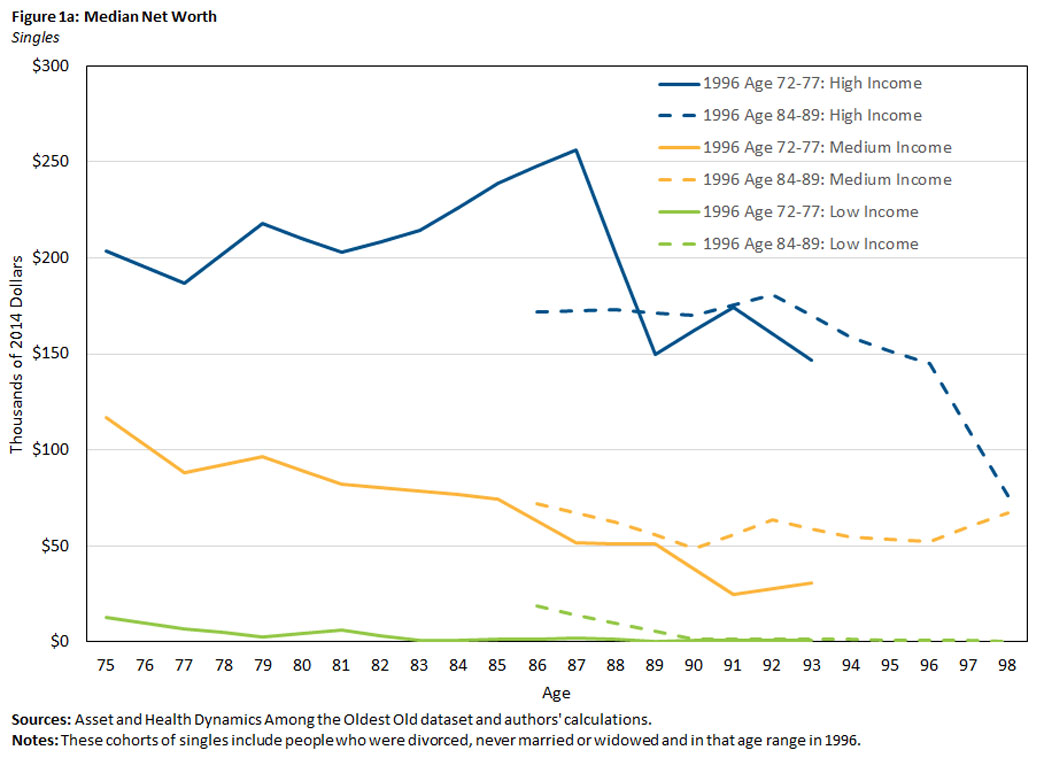

In our recent working paper "Why Do Couples and Singles Save During Retirement?," we use the AHEAD dataset to examine the spending and saving habits of retired households, distinguishing between couples and singles. Figure 1a shows results for individuals who are single throughout our sample period; this includes individuals who are divorced, never married or widowed when first observed in our data sample.2

We find that the singles with the lowest lifetime incomes have the lowest wealth upon retirement and draw down those savings as they age. Individuals in the middle- and top-income brackets more slowly deplete their savings as they age, and they retain some wealth into very old age.

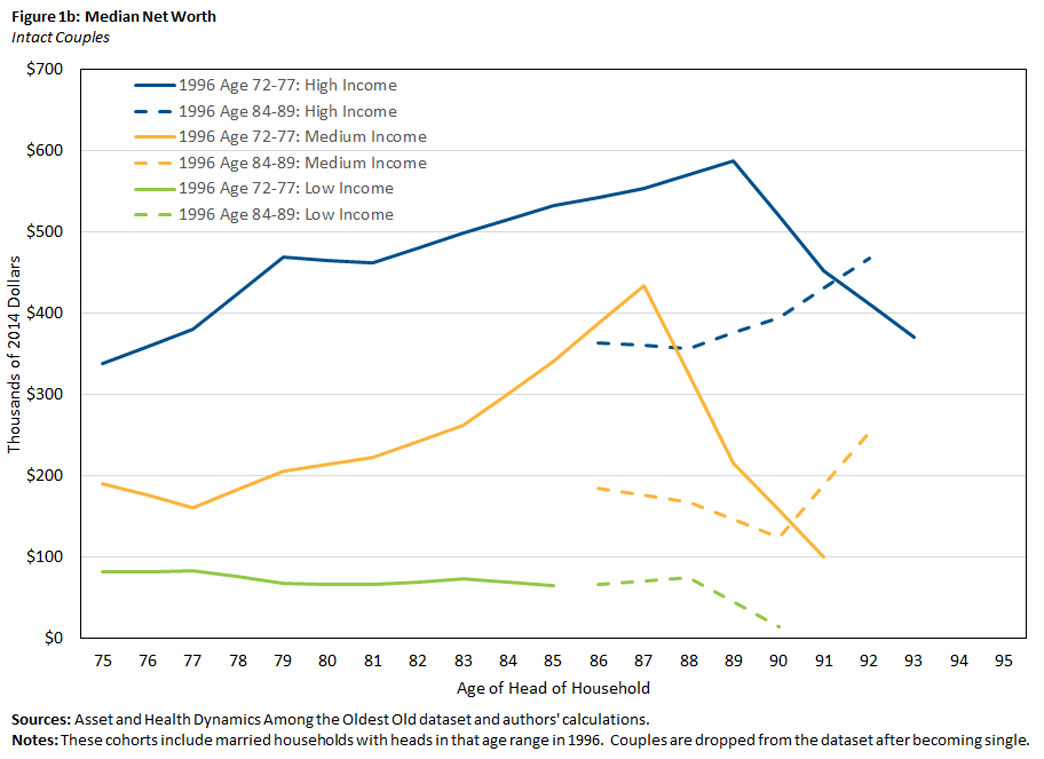

Couples across all income groups, on the other hand, enter retirement with more wealth than singles, as seen in Figure 1b. Additionally, intact middle- and high-income couples continue to accumulate savings until late in life. For example, top-earning couples continue to save until almost age 90, on average.

When constructing Figure 1b, we remove couples once one of their members dies. The AHEAD data shows that a couple's wealth drops sharply — by an average of $160,000 — in the 10 years around the time of the first spouse's death.

Part of this decline comes from medical costs in the years leading up to the first spouse's death. On average, medical spending increases by $27,000 over the six years preceding the death of the first spouse. The rest of the drop is due in large part to bequests made after the spouse dies: On average, $79,000 is transferred to non-spousal heirs.

What Motivates Saving?

These two factors — bequests and medical expenses — are the focus of our analysis. We construct a model in which retired households optimally balance current consumption and saving for the future, accounting for medical expenses and bequests. Retired couples also choose how to distribute their wealth upon the death of a spouse, dividing the estate between the surviving spouse and other heirs. When the last member of the household dies, any remaining wealth is bequeathed.

Regarding medical expenses, we estimate their level and volatility from the data, accounting for important factors like age, gender, marital status and health. Our medical spending measure includes Medicaid payments, which can be substantial for lower-income households. Because the AHEAD dataset lacks accurate measures of Medicaid spending, we impute Medicaid payments by combining AHEAD data with information from the Medicare Current Beneficiary Survey.

We use the model to estimate how retired households' wealth would respond to changes in the motives for saving. Because this exercise only measures changes in post-retirement savings, it provides a lower bound for how saving behavior would respond to policy changes over a longer time horizon.

Impact of Medical Expenses on Saving

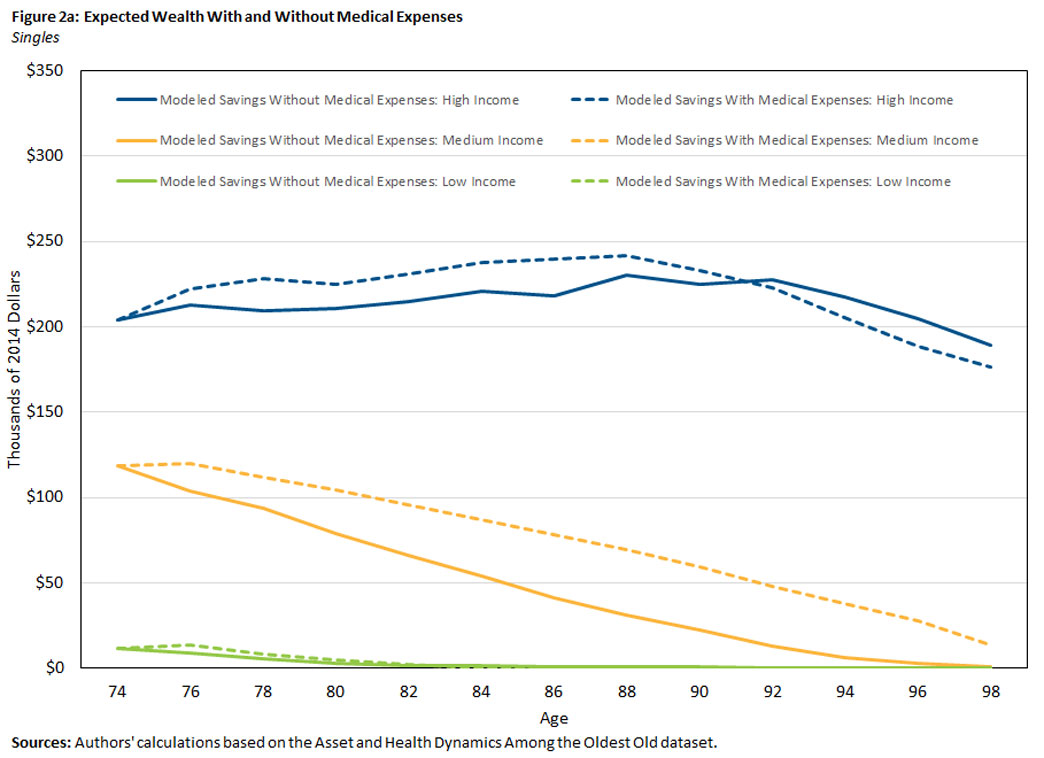

To estimate how much medical expenses motivate saving in retirement, both expected and realized medical expenses are set to zero in the model. Because the lowest-income singles save little for medical expenses and rely almost entirely on Medicaid, this change has little effect on their saving behavior, as seen in Figure 2a.

But removing medical expenses has a much bigger impact on the savings of middle-income singles. The model predicts that this group would have 40 percent less wealth at age 84 (a reduction from $87,000 to $54,000) if they did not have to pay for out-of-pocket medical expenses.

Eliminating medical expenses has a smaller impact on the saving decisions of the wealthiest singles. Their wealth would be 7 percent lower at age 84 (down from $238,000 to $221,000) and would actually increase after age 90. In the latter case, individuals save the funds that they would have otherwise spent on medical expenses.

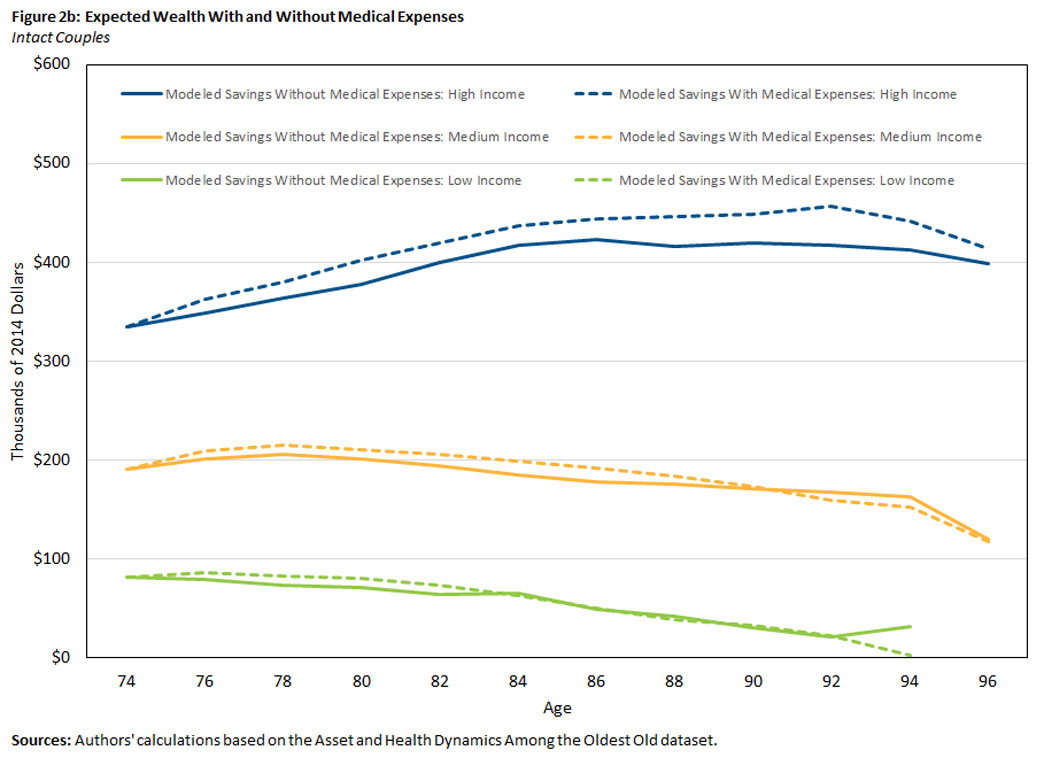

Similar to lower-income singles, the saving behavior of lower-income couples also changes very little in response to removing medical expenses, as seen in Figure 2b. Couples in the middle-income group also do not change their saving decisions by much. The wealthiest couples would reduce their wealth by 5 percent at age 84 (from $437,000 to $417,000) if they did not have to save for medical expenses. Altogether, this suggests that medical expenses play a small part in why couples save after retirement. Our results suggest that bequest motives play a much larger role.

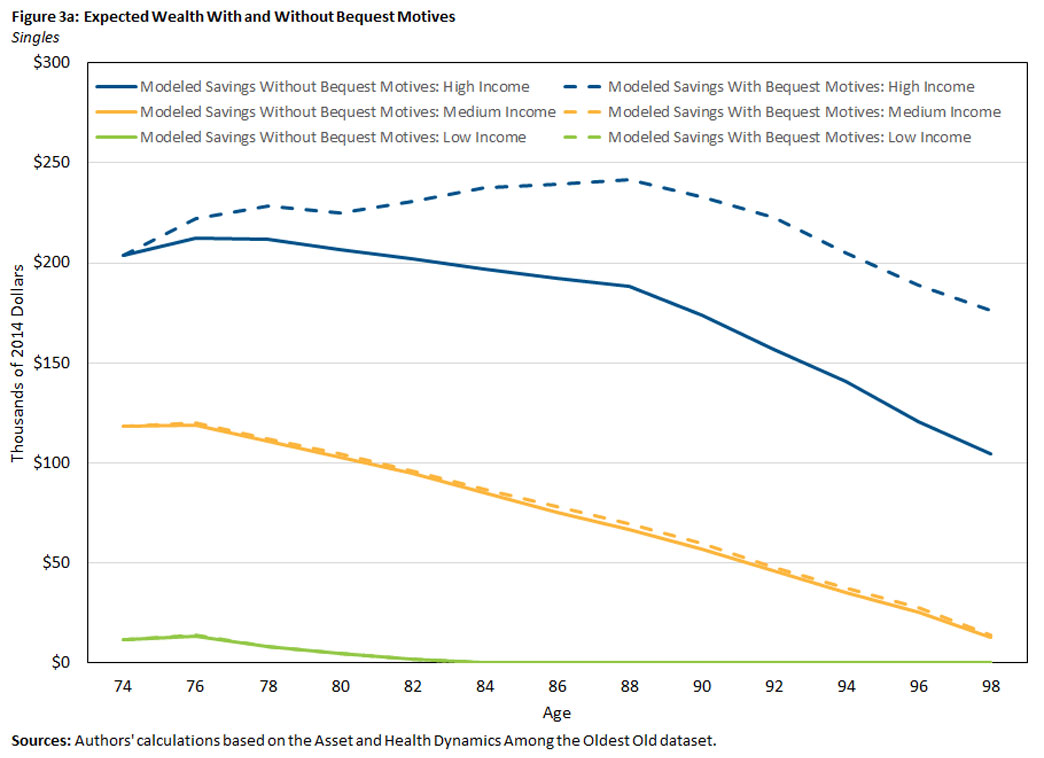

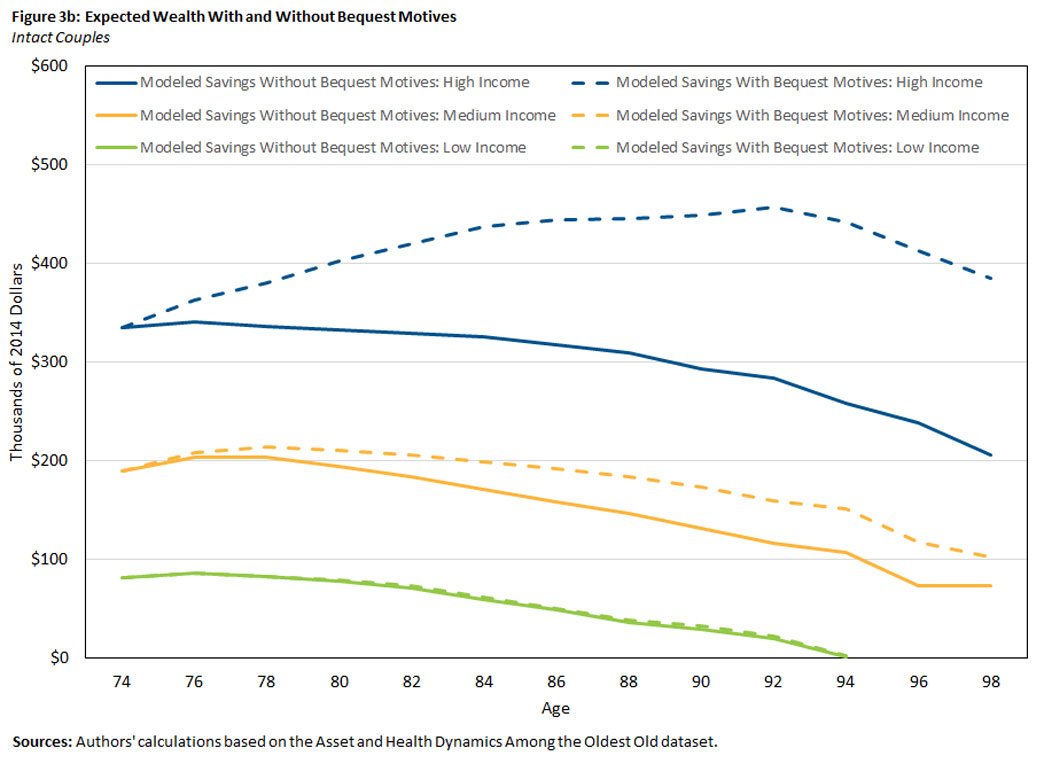

Impact of Bequest Motives on Saving

Figure 3a shows that eliminating bequest motives has a significant effect on singles only among the wealthy, reducing their median savings by 17 percent at age 84 (from $238,000 to $197,000).

The model predicts larger effects for couples. Eliminating bequest motives would reduce the savings of middle-income couples at age 84 by 14 percent (from $199,000 to $172,000) and the savings of the wealthiest couples by 26 percent (from $437,000 to $325,000), as seen in Figure 3b.

These findings suggest that leaving bequests is a higher priority for couples than singles. This could be because couples are wealthier on average than singles, and bequests are a luxury good. Additionally, couples may be more motivated to leave bequests because the money they leave to surviving spouses can be passed on to other heirs after the surviving spouses die. This suggests that bequests might provide greater utility to couples than to singles.

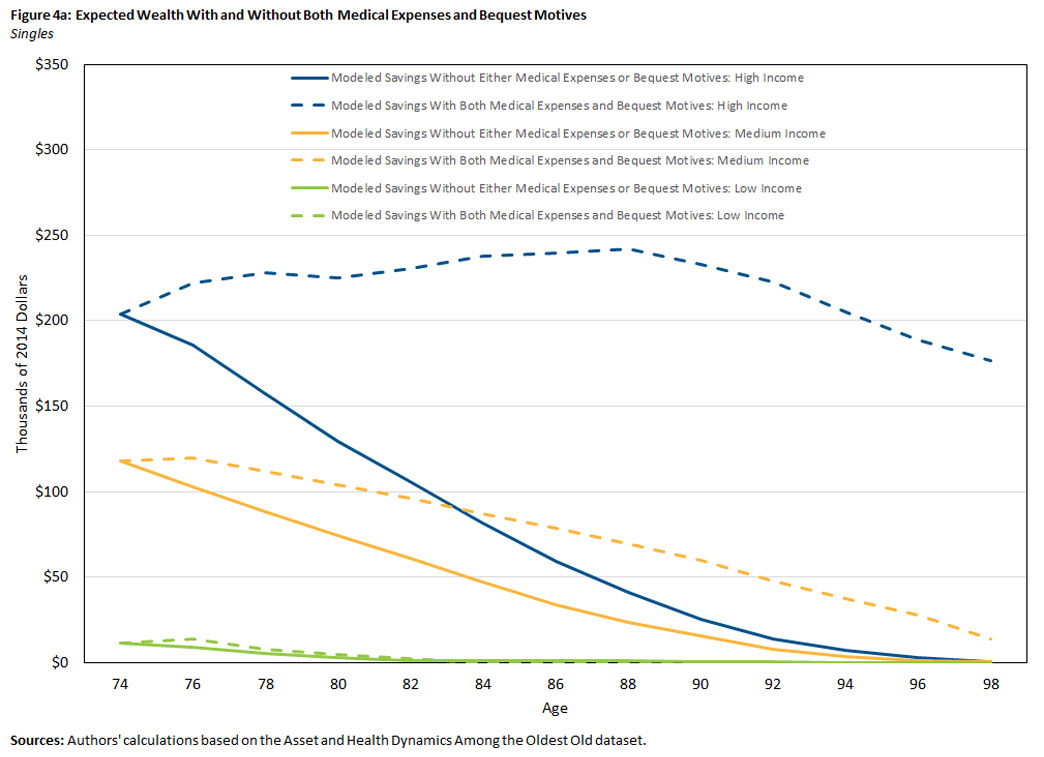

Impact of Both Medical Expenses and Bequests on Saving

It is possible that considering saving for medical expenses and saving for bequests in isolation does not tell the whole story. For example, wealth saved for bequests can also be used to insure against unexpected medical costs. And since future medical expenses are uncertain, retirees who save to cover those costs may die with unspent wealth. The ability to leave bequests gives these unspent funds value, reducing the opportunity cost of self-insuring through saving.

Furthermore, because medical spending reduces wealth, households that are particularly motivated to leave bequests may increase their saving to ensure that some money is left over to pass on to heirs after paying for any medical expenses.

To assess the magnitude of these interactions, we use our model to predict retirement savings in the absence of both medical spending and bequest motives. Because low- and middle-income singles do not have strong bequest motives, the impact of removing both motivations is similar to the impact of removing medical spending alone.

For the wealthiest singles, however, removing both medical spending and the bequest motive has a sizable impact. Savings fall by 66 percent at age 84, from $238,000 to $82,000. This decline is almost three times larger than the decline in savings predicted when either the bequest or medical expense motives are removed alone.

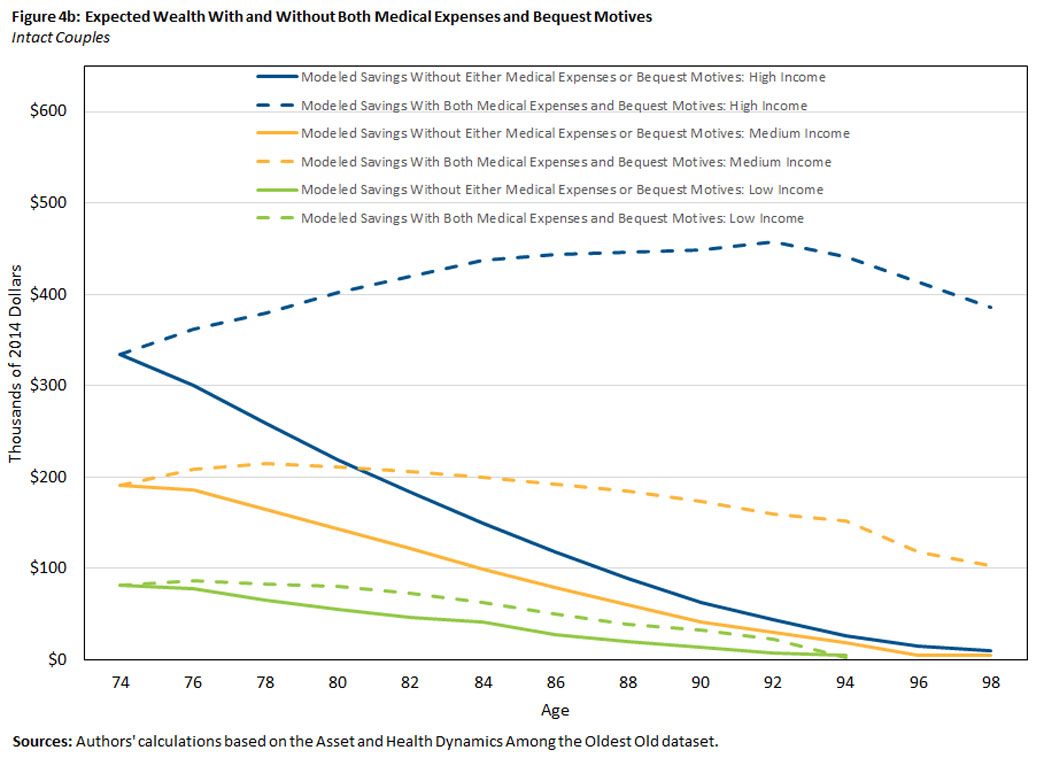

Eliminating both motivations also has a large impact on the saving decisions of couples, with saving falling across all income groups. At age 84, saving falls:

- By 34 percent (from $62,000 to $41,000) for low-income couples

- By 50 percent (from $199,000 to $99,000) for middle-income couples

- By 66 percent (from $437,000 to $150,000) for high-income couples

Conclusion

When it comes to why households save after retirement, preparing for medical expenses appears to be more important for middle-income singles, while the desire to leave bequests is more important for couples and higher-income singles. Additionally, because both motivations interact with each other, it is important to model saving for medical expenses and saving for bequests together in order to get a complete picture of why retirees save.

These findings have several policy implications. They suggest that couples and high-income singles can easily self-insure against medical risk because they save to leave bequests. Low-income singles are insured through Medicaid and do not need to save for medical expenses. Middle-income singles set aside significant amounts of wealth for precautionary purposes because they are not rich enough to prioritize bequests but too rich to qualify for Medicaid. It is this group that would respond most to changes in public health insurance.

Mariacristina De Nardi is a professor of economics at the University of Minnesota and a consultant at the Federal Reserve Bank of Minneapolis, Eric French is a professor of economics at the University of Cambridge, John Bailey Jones is vice president of microeconomic analysis in the Research Department at the Federal Reserve Bank of Richmond, Rory McGee is an assistant professor of economics at the University of Western Ontario, and Tim Sablik is an economics writer in the Research Department at the Federal Reserve Bank of Richmond.

1

For a review of these studies, see our 2016 paper "Savings After Retirement: A Survey."

2

In the working paper, we also examine current singles, where the initial singles are joined by those who become widowed over our sample period (1996-2016).

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us