Omicron Ominous Overseas

Macro Minute

December 28, 2021

Though it's still too early to know the full impact of the omicron variant of COVID-19 on economic activity, it undoubtedly poses risks to next year's economic outlook. Domestically, we saw the delta wave in late summer drag consumer confidence down to its lowest levels in a decade and lead people initially to cut back on spending in entertainment, lodging and air travel. Similar developments could unfold if omicron becomes a larger threat.

"If a spike in omicron cases next year causes supply disruptions that push Chinese producer prices upward, those inflationary pressures could be imported to the United States …"

But omicron risks could be even greater overseas, particularly in China, which detected its first omicron case on Dec. 14. China continues to enforce "zero-COVID" policies by clamping down on social gatherings and business activity in response to COVID-19 outbreaks. For example, authorities have restricted movement in several cities until March 2022 due to a spike in new COVID-19 cases, including in Ningbo, one of China's largest container ports.

This could create knock-on effects for U.S. inflation, as China accounts for about one fifth of U.S. imports of goods from abroad (18.5 percent in 2020). Higher factory prices in China could make Chinese imported goods more expensive for U.S. customers, while clogged ports in China could worsen delivery times and supply bottlenecks in the United States, causing further mismatches of supply and demand.

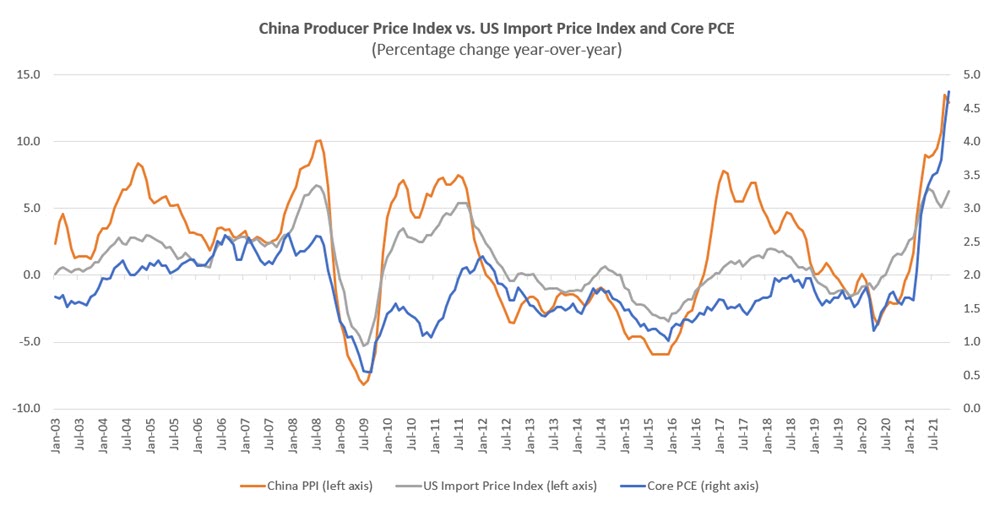

Figure 1 shows significant co-movement between producer price inflation in China and U.S. import price inflation as well as U.S. core PCE inflation. The correlation between China's PPI and U.S. import price inflation is 0.87. The correlation between China's PPI and U.S. core PCE inflation is 0.65.

If a spike in omicron cases next year causes supply disruptions that push Chinese producer prices upward, those inflationary pressures could be imported to the United States, pushing up the level of prices at home. That risk could be even greater if Chinese supply bottlenecks increase just as consumer demand rises with the Lunar New Year just around the corner. 2022 may be a new year, but the high inflation uncertainty we saw in 2021 will be a familiar theme.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us