The Employment Recovery of Small and Large Employers

Special Report

November 12, 2020

Policymakers, national pundits, and researchers often point to the importance of small firms in job creation. Did small firms play a special role in the recovery of aggregate employment during the pandemic? In this article, we use company-level employment data from Ultimate Kronos Group (UKG), a workforce management software provider, to study this question. Firms use the UKG software to manage the time of hourly workers. These employees "punch-in" via the UKG timekeeping system when arriving at work (both in person and virtually). The system computes the hours worked by each employee each week, and this information is then used to pay the employee. As a result, the UKG data are a good indicator of the number of shifts worked by hourly employees in the United States. We thus interpret aggregate weekly punches in the UKG dataset as a measure of aggregate U.S. employment.

The UKG data are available at a weekly frequency from January 2020 to September 2020 and provide weekly punches aggregated to the level of the parent firm or company. There are 12,224 firms in the UKG dataset. The dataset provides an industry classification for nearly three-quarters of the firms, spanning a wide range of industries: 34.1 percent of firms are in services and distribution, 22.5 percent of firms are in manufacturing, 12.6 percent are in retail, 17.2 percent are in health care, and the rest are in the public sector. In the analysis that follows, we focus on the number of weekly punches across time for firms that were active (e.g., reporting a positive number of punches) during at least one week during the months of January and February.

Aggregate Statistics

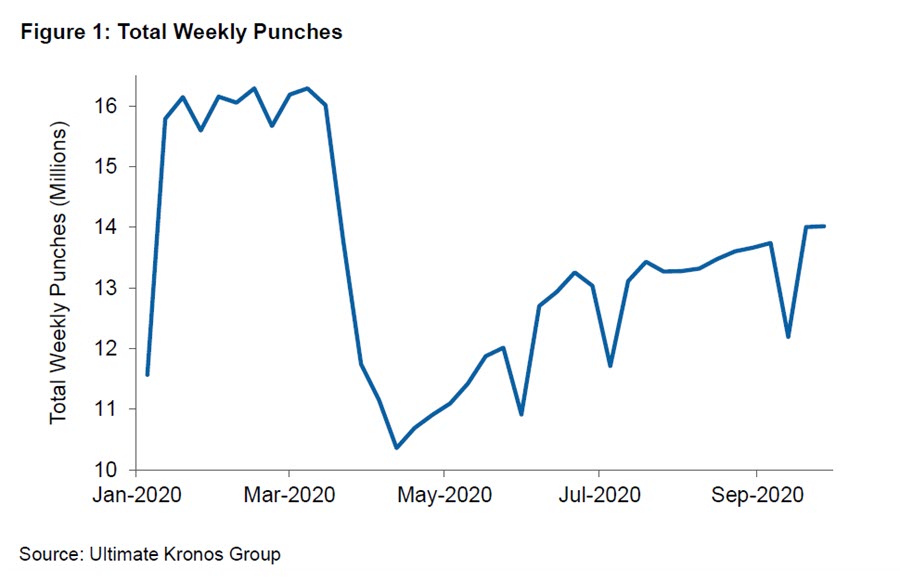

Figure 1 shows the time series of total weekly punches. Before the pandemic, there were around 15.4 million punches logged in the UKG system each week. By the middle of April, total weekly punches fell to 10.7 million, a 31 percent decrease. As states opened, the number of weekly punches gradually increased to 14 million. This implies that, as of the last week of September, aggregate hourly employment had recovered to around 9 percent below the pre-pandemic level. Notice the temporary drops in employment during Memorial Day week, the week around July 4, and the week around Labor Day.

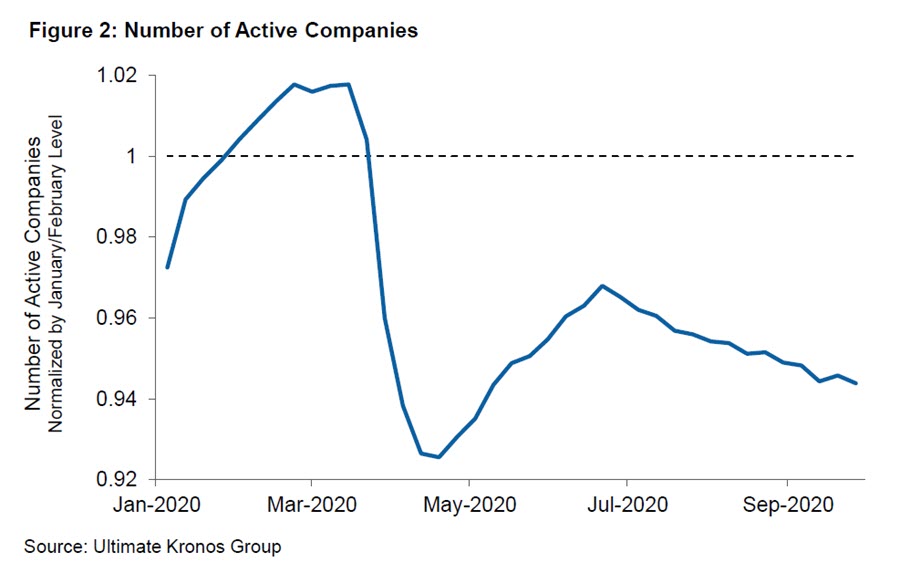

Figure 2 shows the number of active firms each week, defined as firms with at least one week of positive punches in January and February (normalized by the average number of active firms in January and February). The initial pandemic shock led to a massive drop in active firms: 10 percent of firms active in March were inactive in late April. The number of active firms increased between late April and late June but then began to decline again. Overall, 8 percent of active firms in March were inactive by late September.

Small Versus Large Firms

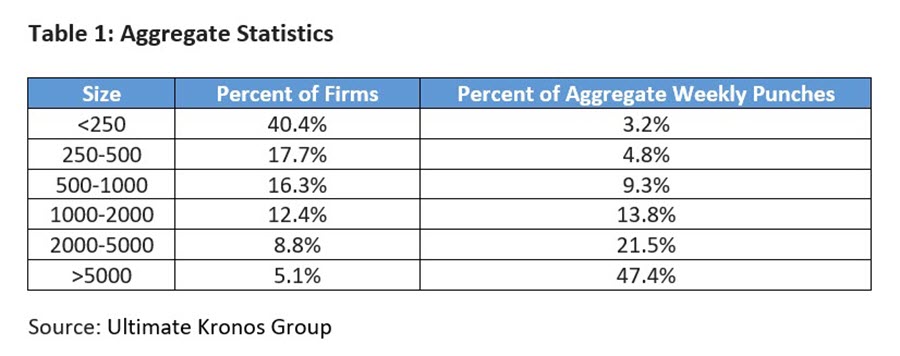

We group firms according to their average number of weekly punches between January 2020 and February 2020. The first group includes firms with fewer than 250 average weekly punches, while the last group includes firms with more than 5,000 average weekly punches. Table 1 presents some aggregate statistics across these groups. While smaller firms account for a large fraction of firms, they account for a small fraction of aggregate weekly punches: Nearly 60 percent of firms have 500 or fewer weekly punches, but they represent only about 8 percent of the total punches.

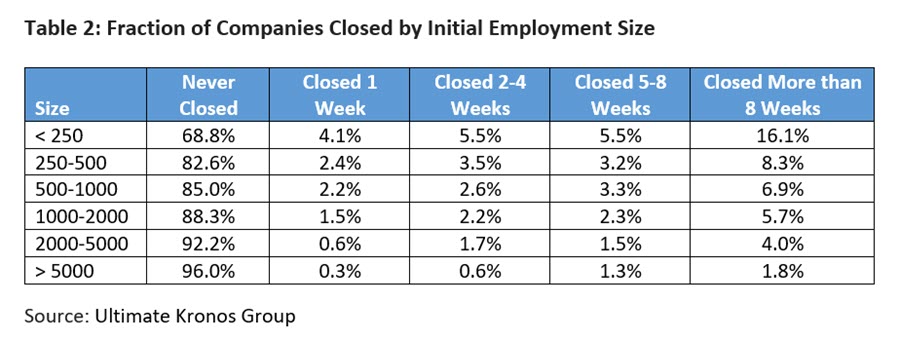

Table 2 shows firm shutdowns by size. There is substantial variation: While only 4 percent of the largest firms shut down operations for at least one week, 31.2 percent of the smallest firms (fewer than 250 weekly punches) experienced at least a one-week shutdown. Further, the incidence of a shutdown declines monotonically with firm size. Conditional on shutting down the firm for at least a week, the incidence of long, maybe permanent, shutdowns is similar across the firms of different sizes: Around half of firms that shut down did so for at least eight weeks.

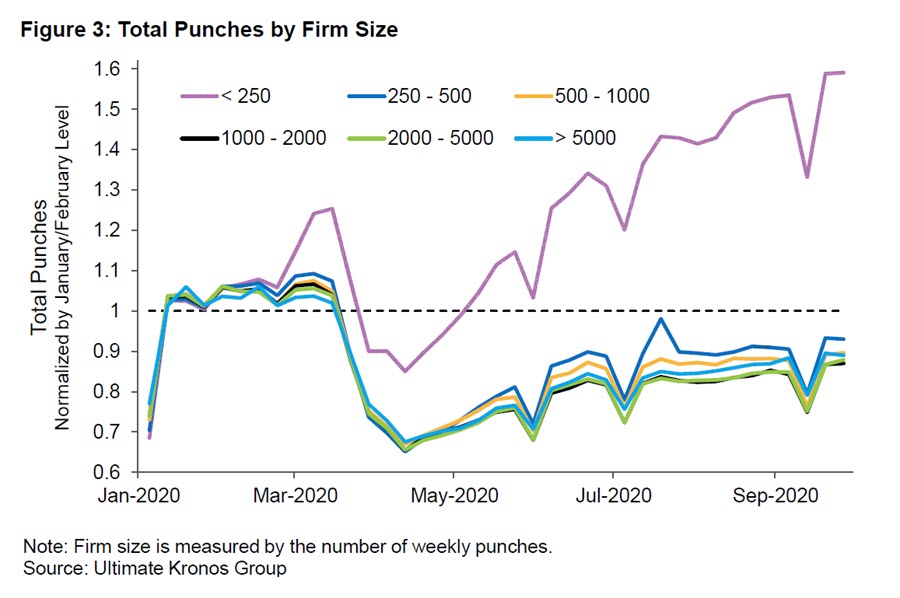

Despite being more likely to shut down, smaller firms experienced larger rebounds in terms of total weekly punches than larger firms during the recovery that followed the initial pandemic shock. Figure 3 plots the number of weekly punches across firms of different sizes, where weekly punches for each group are normalized with respect to the group's average of weekly punches during January and February. As mentioned, the figure shows that while small firms experienced more shutdowns, they grew more quickly than larger firms during the recovery.

Final Observations

We used firm-level data from UKG to analyze the path of the employment recovery for small and large firms. Small firms were more likely to experience shutdowns than large firms. However, small firms grew faster as the economy recovered.

A natural question is whether the exceptional employment recovery of small firms is persistent. For example, small firms might expand their employment in response to seasonal demand. If this is the case, we should expect the employment gains of small firms to vanish soon, negatively affecting unemployment in the next months.

Another aspect to consider is the role of government programs in aiding small firms during the pandemic. Does the large employment growth of small firms reflect to some extent their eligibility for loans through the Paycheck Protection Program?

While with our data we cannot make conclusive statements about whether the employment growth of small firms reflects seasonal or persistent trends, or whether the success of small firms is due to the recent government programs, we view our findings as a meaningful contribution to the discussion about the merits of size-dependent policies.

Marios Karabarbounis is an economist, Matthew Murphy is a research associate, and Nicholas Trachter is a senior economist in the Research Department at the Federal Reserve Bank of Richmond.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us