An Aging America

America's aging trend (see chart) reflects several distinct causes. The most famous of them, the baby boom, is the jump in fertility that took place following World War II and continued for 18 years. Birth rates during this period ranged from 24 to 26.5 per 1,000 people in the population, compared with 18 to 19 per 1,000 people during the Great Depression years leading up to the war. The term "baby boomer" commonly refers to people born in the United States from 1946 to 1964, when birth rates finally fell to their pre-boom levels.

The baby boom wasn't America's first postwar birth boom — a brief, shallow one took place during the two years following World War I — nor was it a historical peak in U.S. birth rates. What has made it a powerful driver of today's aging trend is partly the sheer number of baby boomers who were born in its long duration, some 72.5 million in all.

Another reason for the aging trend is the pattern of U.S. birth rates in the 50 years since the end of the baby boom. During that time, birth rates never returned to even the lowest levels of the baby-boom years. They have hovered around 15 per 1,000 people since the early 1970s, declining further with the 2007-2009 recession. In 2012, the latest year for which data is available, the rate was down to 12.6 per 1,000.

Combined with the declines in birth rates are the increases in our life expectancies, from 47.3 years in 1900 to 68.4 years in 1930 and 78.2 years in 2010.

While America is aging, it is far from alone in doing so. The other large developed countries are generally older. In 2012, the populations of Germany, Italy, and Japan were at least one-fifth seniors aged 65 or older, a level that the United States is not expected to reach for decades.

To be sure, population forecasting is not foolproof. John Maynard Keynes asserted in a 1937 speech before the Eugenics Society that Britain would soon face "a stationary or declining level" of population — a prediction he made on the eve of that country's wartime and postwar baby booms. In the case of the present-day United States, one of the variables that will affect the age structure of the population is the course of future immigration. Still, given the size of the baby-boomer pig moving through America's demographic python, there is little debate that America will be getting older.

Defanging the Fed

People's patterns of consumption and savings tend to vary in predictable ways as they get older. That's according to the "life cycle hypothesis," originated in the early 1950s by Franco Modigliani, then an economics professor at Carnegie Mellon University, and Richard Brumberg, a graduate student at Johns Hopkins University. The basic idea is simple: Individuals try to smooth out their consumption over their lifetimes by borrowing when they are young adults, building up savings as their incomes increase during their working years, and drawing down their savings after they retire.

For economists studying the effect of demographic change on financial markets, the ages 40 to 64 are often considered the asset-accumulating years. Some economists have argued that the long-term upward trends of recent decades in the stock market and housing markets have been driven in part by the rise of the baby boomers. Indeed, since the late 1980s, a number of economists, starting with Greg Mankiw of Harvard University and David Weil of Brown University, have suggested that the influence of life cycle effects may lead to declining house prices as the baby boomers leave their asset-accumulating years behind.

One aspect of the life-cycle effect with implications for monetary policy is that older households tend to hold less debt as a fraction of net worth, which could work to reduce the sensitivity of their consumption to interest rates. "A change in interest rates on a large sum of debt implies higher interest payments," International Monetary Fund (IMF) economist Patrick Imam said in an email. "Therefore, younger households have to cut their expenditure much more to pay the higher interest payments than older households, and vice versa if interest rates go down."

Another life-cycle effect that could dampen the influence of monetary policy is the assumed tendency of older individuals to be more risk-averse in their investments than younger ones, in line with the common advice of financial writers and advisers to shift assets into less risky investment categories as one ages. Such risk-aversion by a growing population of older investors could create headwinds for the Fed because its low-interest-rate policies get some of their effectiveness from a "risk-taking" channel of monetary policy: that is, the tendency of some investors in a low-interest-rate environment to reduce their holdings of safe assets such as Treasuries in favor of riskier assets such as stocks and high-yield bonds, a process sometimes known as a search for yield. But that effect works only if people actually take greater risks in response to easier monetary policy, and some economists believe that older households may be less willing to do so. In this view, the less risky the investments that investors move into in response to low Fed policy rates — if they move their money at all — the less stimulus to economic activity through the risk-taking channel of monetary policy.

"Financial entities and households have been found to take more risk by borrowing more and investing in riskier assets when interest rates fall and less when interest rates rise," Imam said. "Older people, who are more risk-averse — as they cannot easily make up for losses — may be less sensitive to the ‘search for yield' effect than younger ones. Elderly households would not want to invest as much in risky sectors, thereby not allowing those sectors to take off on a large scale."

Into The Gray Unknown

Yet a number of complicating factors leave it unclear how much the Fed's policy tools will be weakened, or even whether they will be significantly affected at all. As it turns out, households don't seem to dissave as much in retirement as the classic life-cycle hypothesis predicts. Despite the theory, moreover, households increasingly keep borrowing even in their later years.

"We have seen in the last couple of decades, as households have refinanced mortgages in midlife into their 50s and sometimes even 60s, more households reaching traditional retirement age with mortgage debt on the books," says Massachusetts Institute of Technology economist James Poterba, who has studied the effect of aging on financial markets. "The days of people borrowing when they were 32, paying off the mortgage when they were 62, and burning their mortgage have become fewer and fewer as more people have refinanced."

The risk-taking channel also doesn't seem to behave entirely in accord with the predictions of theory, Poterba notes: The Fed's Survey of Consumer Finances indicates that older households continue to hold risky assets, such as stocks, in significant amounts. "Even at the traditional retirement age of 65, the typical household has quite a number of years left that it needs to draw its resources down over," Poterba says. "There probably is some shift toward less risk appetite in those older years, but people don't hit retirement and say they don't want risky assets anymore."

A further complicating factor is that in an increasingly open global economy, financial assets can cross borders. Countries are not aging in lockstep: For example, China, Japan, and continental Europe are aging faster than the United States, which, in turn, is aging faster than many emerging-market economies. In theory, to the extent that changing demographics leads to changes in asset prices and returns, investors in aging, lower-return markets can be expected to move their assets to younger economies in pursuit of higher returns, somewhat muting the effects on asset markets of demographic shifts within a country. But the extent to which such movements would offset the influence of demographics on the effectiveness of monetary policy is unclear.

"Our ability to model these cross-border macroeconomic effects is still very inadequate," says Brookings Institution economist Ralph Bryant. "There are miles and miles to go before we are in a better place to generate reliable conclusions about effects on policy."

Finally, there is another channel through which life-cycle behavior may affect the power of monetary policy — a wealth effect that pushes in the opposite direction as the effect on consumption by the young, possibly amplifying the influence of interest-rate changes. A more familiar example of a wealth effect is the effect on a household's financial behavior when it enjoys significant appreciation of its house, an increase in its wealth that may lead it to spend more. In the context of life-cycle behavior and monetary policy, the idea is that although many older households are cash-strapped, older households as a group tend to be wealthier than the young and hold more financial assets. Older households, therefore, are likely to be more exposed to the effect of interest-rate changes on financial assets through changes in their wealth. In an older society, that effect may increase the responsiveness of the household sector as a whole to monetary policy.

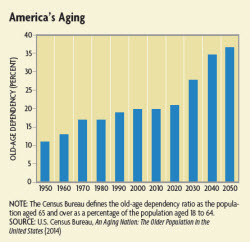

Which effects will prevail? It's challenging to reach firm empirical conclusions in this area because demographic change is slow. One such effort, by Imam of the IMF, studied the effect of monetary policy shocks on inflation and unemployment in the United States, Canada, Japan, the United Kingdom, and Germany and found that their effect has decreased over time. Imam further looked at whether this effect was associated with the timing of the aging of those societies and found "quite a strong negative long-run effect of the aging of the population on the effectiveness of monetary policy." Imam estimated the change that a 1 percentage point increase in the old-age dependency ratio — the ratio of people older than 64 to those of traditional working age — would make in the effectiveness of a 1 percentage point shock to interest rates by monetary policymakers. He determined that a 1 percentage point increase in the old-age dependency ratio reduces the effect of such an interest-rate change on inflation by 0.1 percentage point and its effect on the unemployment rate by 0.35 percentage point.

The Census Bureau estimates that the old-age dependency ratio in the United States will rise by 14 percentage points from 2010 to 2030. If Imam's estimates and the Census Bureau's estimates were to hold, they would imply a 1.4 percentage point drop in the Fed's ability to affect inflation and a 4.9 percentage point drop in its ability to affect unemployment. Over the course of a 20-year period, such a change might be perceived as modest from one year to another, but cumulatively it would amount to a strong negative effect indeed.

Higher Expectations

If such a scenario occurred, the Fed would need to use its policy tools in an increasingly aggressive way to achieve the same results. In addition, any downward push from demographics on the Fed's influence would increase the chances that it will one day have to grapple again with the zero lower bound — the assumed inability of monetary policy to reduce nominal short-term interest rates below zero. This limitation has led to the use of some unconventional monetary policy tools since the Great Recession, most notably quantitative easing. Because quantitative easing enables the Fed to add further monetary stimulus to the economy even when interest rates are at or near zero, it is possible that the ship QE would sail more often in the future.

Demographic change would also affect Fed policy in other ways. The fact that the elderly are more likely to be out of the labor market would probably have ripple effects on other features of the economy that Fed officials look at to determine monetary policy, such as the natural rate of unemployment (that is, the lowest level of unemployment that the economy can maintain in the long run).

An older society may also bring the Fed a somewhat different set of political pressures. The disproportionate absence of the elderly from the labor force would tend to lead them to be more concerned about the Fed's inflation mandate than its employment mandate. Charles Bean, former deputy governor of the Bank of England and its chief economist before then, suggested in a 2004 speech that aging may affect central banks by increasing the constituency for low inflation in another way, as well. Given the higher asset holdings of an older cohort, he predicted, with more of its wealth in bonds than stocks, an older society will tend to favor low-inflation policies (to the extent that bond holdings of seniors are not inflation-protected). At the same time, Bean said, with the decline of defined-benefit pensions, an older society will expect more from its central bank in preventing falls in asset prices.

While the effects of aging on monetary policies are uncertain for now, one prediction can be made with confidence: We won't be getting any younger.

Readings

Bean, Charles. "Global Demographic Change: Some Implications for Central Banks." Speech at the Federal Reserve Bank of Kansas City Annual Symposium, Jackson Hole, Wyo., Aug. 28, 2004.

Imam, Patrick. "Shock from Graying: Is the Demographic Shift Weakening Monetary Policy Effectiveness?" IMF Working Paper No. 13/191, September 2013.

Kara, Engin, and Leopold von Thadden. "Interest Rate Effects of Demographic Changes in a New-Keynesian Life-Cycle Framework." ECB Working Paper No. 1273, December 2010.

Miles, David. "Should Monetary Policy be Different in a Greyer World?" in Alan Auerbach and Heinz Herrman, eds., Ageing, Financial Markets and Monetary Policy. Berlin: Springer, 2002.

National Research Council. Aging and the Macroeconomy: Long-Term Implications of an Older Population. Washington, D.C.: National Academies Press, 2012.

Poterba, James, "The Impact of Population Aging on Financial Markets," in Gordon H. Sellor Jr., ed. Global Demographic Change: Economic Impact and Policy Challenges. Kansas City: Federal Reserve Bank of Kansas City, 2005, pp. 163-216. (Working paper version available online.)