Will America Get a Raise?

Economists debate why wage growth has been so sluggish during the recovery from the Great Recession

Econ Focus

First Quarter 2016

Cover Story

The persistence of slow wage growth since the Great Recession — amid a steady economic recovery and a sharp drop in unemployment — has become one of the biggest puzzles for economists in recent years. It’s not just an issue for economists; in this election cycle, weak wage growth has been used to support proposals ranging from strengthening unions to boosting the federal minimum wage. More broadly, stagnating incomes have likely fed into the broader ongoing economic pessimism among Americans. One recent Pew Research survey, for example, found that 73 percent of those polled described economic conditions as fair or poor, while only 27 percent considered them excellent or good.

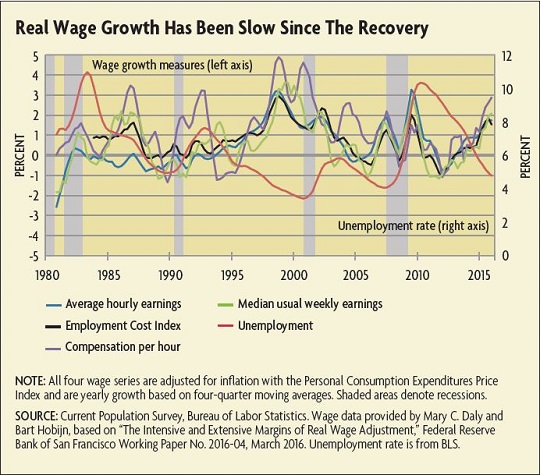

Numerous measures indicate that wage growth has indeed been sluggish since the Great Recession compared to the decade before. For example, in a working paper released earlier this year, economists Mary Daly of the Federal Reserve Bank of San Francisco and Bart Hobijn of Arizona State University found a general deceleration in wages across four different measures of labor compensation compared to the 2000s. These measures include average hourly earnings of private sector production and nonsupervisory workers, as well as compensation per hour in the nonfarm business sector; they also include the quarterly median usual weekly earnings of full-time wage and salary workers, which captures overtime pay and trends in the average workweek, and the broader quarterly Employment Compensation Index, which tracks both wages and benefits. Even though these series cover disparate forms of labor compensation, they are quite closely correlated. (See chart below.)

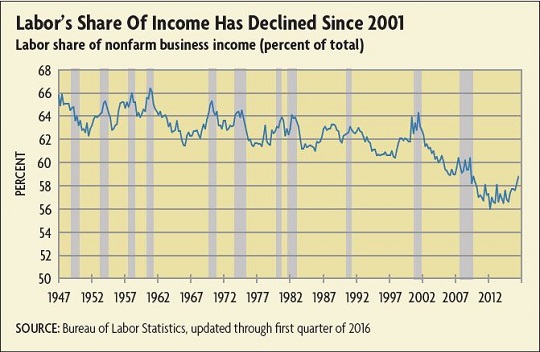

One especially curious feature of the drop in labor share is that it appears to be global. To be sure, there is international variation in how much of each economy's output is split between labor and capital, and how income is measured. That said, economists do think a variety of common structural changes in the global economy may be at play. Some of the more popular explanations include "capital deepening" (a substitution of capital for labor in the production process), globalization, and rising inequality. But economists are divided over the power of any one explanation.

Hobijn, joined by Şahin and University of Edinburgh economist Michael Elsby, analyzed some potential explanations in a 2013 article from the Brookings Papers on Economic Activity. Technology and equipment have become relatively cheaper, and far more sophisticated, over the decades, so to the extent that capital has replaced labor, it could be redistributing income from labor to capital. The problem with this theory is that the rate of growth in capital intensity has actually slowed down since the decline in labor share began. The authors also address the argument that the drop in labor share has occurred because the wealthy may be accruing more of their income through capital. Recent increases in income inequality, they point out, have been largely driven by wage divergence, not investment income. Higher wages at the top would, in fact, help to keep the labor share high, which means the decline in labor share has occurred despite rising inequality, not because of it. In short, these two explanations — capital deepening and inequality — don't quite succeed in getting to the heart of this puzzle.

What about globalization-based explanations? U.S. firms, like firms across the world, typically offshore the more labor-intensive functions of their production chain to countries where wages are cheaper, while leaving the capital-intensive functions at home — in turn, lifting the capital side of the income share. But here, too, the problem is timing, because this shift began well before the decline in labor share. Elsby, Hobijn, and Şahin did point to an interesting correlation, however: They found that industries with the most exposure to imports (predominantly manufacturing) also saw the largest declines in their labor share, possibly through the offshoring of the more labor-intensive components of the U.S. supply chain. While noting this is only a correlation, not causation, they calculated that this effect accounts for much of the drop in the labor share. The effect of import exposure on wages suggests that the workers are increasingly competing with global counterparts for jobs — through offshored production lines and trade — thus driving down wages of workers in those sectors. But the authors cautioned against reaching any firm conclusions without more evidence.

Whatever the cause, the long-term trend of the labor share is one important part of understanding weak wage growth over the long run. As Hobijn put it, "Wage growth can be explained by three things: if what you produce is valued more, if you become more productive, or, if the labor share of income increases. The fact that productivity growth is slowing and the labor share is declining suggests that we'll see more sluggish wage growth going forward."

Wages and Normalization

The new research on recent wage behavior may provide economists with a better understanding of the dynamics that have been at play in the recovery. For the workers affected, and for policymakers seeking solutions, the ever-shifting dynamics of the labor market may offer clues on what tools can help people stay productive and steadily employed — for example, through investment in education, job training measures, or job-sharing schemes. However, economists are far from having the ideal measure of wage growth that Abraham and Haltiwanger envisioned. Or, furthermore, one that provides a reliable indicator of labor market slack for the Fed.

What does slack mean, exactly, for Fed policy? Some observers argue that stagnant wages signal that the economy still has significant room to expand without generating inflation, because there are still many part-time workers and workers who have dropped out of the labor force, who would like to work full time but cannot. These workers may be willing to take new jobs at wages well below what they used to earn if such jobs were available. This has led some to argue that the Fed should delay raising rates on the grounds that it has yet to fulfill its mandate on reaching maximum employment.

Some groups have gone a step further and argued that the Fed should formally consider a wage growth target when it makes policy. For example, the Economic Policy Institute, a liberal think tank, has argued that nominal wages need to rise an annualized 3.5 percent to 4 percent (in other words, pre-recession rates), rather than the current 2.5 percent, before the Fed should consider raising rates. The EPI reasons that this growth rate accounts for both the current trend in productivity growth and the Fed's 2 percent inflation target.

A more widespread (if not universal) interpretation on the Federal Open Market Committee, however, is that slack is diminishing, as noted recently in the committee's statement following its July meeting. Fed Chair Janet Yellen noted in June that the Fed is "beginning to see slightly faster wage growth based on [nominal] average hourly earnings … about 2.5 percent and that's up from the very low level it was." She also cited the data provided by the Atlanta Fed wage tracker, a widely used nominal-wage aggregate series based, in part, on Daly and Hobijn's methodology, showing that wage growth has modestly accelerated in the last two years. And a broader gauge, the Board of Governors' Labor Market Conditions Index, shows that most labor-market indicators are back to pre-recession levels.

Finally, even if there is a smaller amount of slack left, it means that people returning to full-time work may face a lower starting wage because there is still relatively more labor supply than labor demand, compared to the pre-recession economy. Also, workers coming back to full-time employment may well be earning discounted wages that are lagging trend productivity growth — and that may not change rapidly even as the labor market improves.

"Wage growth is really more of a lagging indicator of slack," says Daly. "Once unemployment drops down to its natural rate, it will take time to pressure wages upwards because you have more people outside the workforce waiting to get back in. In other words, labor markets adjust first through quantity — employment — and then through price — or wages."

This adjustment is part of what Yellen and other Fed officials will continue to look for as they decide how quickly to normalize monetary policy, as well as the sustainability of progress in other gauges of labor market health. But for economists more generally, the tougher challenge is in understanding the longer view — both the historical trend, and the outlook in the decades ahead — of what kind of fundamental changes might keep a lid on robust wage growth over time.

Readings

Abraham, Katharine G., and John C. Haltiwanger. "Real Wages and the Business Cycle." Journal of Economic Literature, September 1995, vol. 33, no. 3, pp. 1215-1264. (Article![]() available online with subscription.)

available online with subscription.)

Armenter, Roc. "A Bit of a Miracle No More: The Decline of the Labor Share.![]() " Federal Reserve Bank of Philadelphia Business Review, Third Quarter 2015, vol. 98, no. 3, pp. 1-9.

" Federal Reserve Bank of Philadelphia Business Review, Third Quarter 2015, vol. 98, no. 3, pp. 1-9.

Armona, Luis, Samuel Kapon, Laura Pilossoph, Ayşegül Şahin, and Giorgio Topa. "Searching for Higher Wages.![]() " Federal Reserve Bank of New York, Liberty Street Economics Blog, Sept. 2, 2015.

" Federal Reserve Bank of New York, Liberty Street Economics Blog, Sept. 2, 2015.

Daly, Mary C., and Bart Hobijn. "The Intensive and Extensive Margins of Real Wage Adjustment.![]() " Federal Reserve Bank of San Francisco Working Paper No. 2016-04, March 2016.

" Federal Reserve Bank of San Francisco Working Paper No. 2016-04, March 2016.

Daly, Mary C., Bart Hobijn, and Benjamin Pyle. "What's Up With Wage Growth?![]() " Federal Reserve Bank of San Francisco Economic Letter No. 2016-07, March 7, 2016.

" Federal Reserve Bank of San Francisco Economic Letter No. 2016-07, March 7, 2016.

Elsby, Michael W. L., Bart Hobijn, and Ayşegül Şahin. "The Decline of the U.S. Labor Share![]() ." Brookings Papers on Economic Activity, Fall 2013, pp. 1-52.

." Brookings Papers on Economic Activity, Fall 2013, pp. 1-52.

Federal Reserve Bank of Atlanta Wage Growth Tracker![]() .

.

Kudlyak, Marianna. "What We Know About Wage Adjustment During the 2007-09 Recession and Its Aftermath." Federal Reserve Bank of Richmond Economic Quarterly, Third Quarter 2015, vol. 101, no. 3, pp. 225-244.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us