Paying for World War I: The Creation of the Liberty Bond

Econ Focus

First Quarter 2016

LICENSED UNDER ATTRIBUTION VIA WIKIMEDIA COMMONS

Charlie Chaplin and Douglas Fairbanks at a Liberty Bond rally, 1918.

Editor’s Note: A version of this article first appeared on the Federal Reserve History website. The author is the Edward A. Dickson Distinguished Emeritus Professor of Economics at the University of California, Riverside and a visiting scholar at UC Berkeley.

World War I began in Europe in 1914, the same year the Federal Reserve System was established. During the three years it took for the United States to enter the conflict, the Fed had completed its organization and was in a position to play a key role in the war effort. Wars are expensive and, like every governmental effort, they have to be financed through some combination of taxation, borrowing, and the expedience of printing money. For this war, the federal government relied on a mix of one-third new taxes and two-thirds borrowing from the general population. Very little new money was created. The borrowing effort was called the "Liberty Loan" and was made operational through the sale of Liberty Bonds. These securities were issued by the Treasury, but the Fed and its member banks conducted the bond sales.

Generally speaking, the secretary of the Treasury proposes a funding plan for war financing and works with Congress to enact the necessary legislation, while the Fed operates with considerable independence from both the executive and legislative branches of government. But World War I was different. The Treasury and the Fed, united under one leader, worked together in both the creation of the financial war plan and its execution.

Rejecting Printing-Press Finance

When the United States entered World War I in 1917, it became immediately evident that an unprecedented effort would be required to divert the nation’s industrial capacity away from meeting consumer demand and toward fulfilling the needs of the military. At the time of the congressional declaration of war, the American economy was operating at full capacity, so the requirements of the war effort could not be met by putting underutilized resources to work. William Gibbs McAdoo, secretary of the Treasury and chairman of the Fed’s Board of Governors, understood that the wartime population would have to sacrifice to pay the bill. Shortly after war had been declared, he delivered a speech that he later recorded for posterity:

"We must be willing to give up something of personal convenience, something of personal comfort, something of our treasure — all, if necessary, and our lives in the bargain, to support our noble sons who go out to die for us."

But the question remained: How would the shift in output be arranged? How should the war be paid for? There were three possibilities: taxation, borrowing, and printing money.

For McAdoo, printing money was off the table. The experience with issuing "greenbacks" during the Civil War suggested that fiat money would generate inflation, which he thought would lower morale and damage the reputation of the newly issued paper currency, the Federal Reserve Note. McAdoo also opposed printing money because it would hide the costs of war rather than keeping the public engaged and committed. "Any great war must necessarily be a popular movement," he thought, "… a kind of crusade."

McAdoo chose a mix of taxation and the sale of war bonds. The original idea was to finance the war with an equal division between taxation and borrowing. Taxation would work directly and transparently to reduce consumption. Taxes are compulsory, and those who must pay are left with less purchasing power. Their expenditures will fall, freeing productive resources (labor, machines, factories, and raw materials) to be employed in support of the war. Another advantage of taxation was that Congress could set the rate schedule to target those they thought should bear the greatest burden. President Woodrow Wilson and the Democrats in Congress insisted on a sharply progressive schedule — taxing those with very high incomes at higher rates than the middle class and exempting the poor. The highest marginal rate eventually reached 77 percent on incomes over $1 million.

Accompanying the personal income tax was an increase in the corporate income tax, an entirely new "excess-profits tax," and excise taxes on such "luxuries" as automobiles, motorcycles, pleasure boats, musical instruments, talking machines, picture frames, jewelry, cameras, riding habits, playing cards, perfumes, cosmetics, silk stockings, proprietary medicines, candy, and chewing gum. These taxes ranged from 3 percent on chewing gum and toilet soap to 100 percent on brass knuckles and double-edged dirk knives. A graduated estate tax on the transfer of wealth at death exempted the first $50,000 and rose progressively thereafter from 1 percent to 25 percent.

Yet there was a risk. Poor sales would be a sign of weak support and insufficient patriotism. To avoid a failure to sell the entire bond issue, the government arranged to sell them in a series of brief but intense campaigns by subscription. The first campaign was announced on April 28, 1917 — 22 days after the declaration of war. The first offering of bonds was to be for $2 billion and promising a 3.5 percent rate of return. That was slightly below the rate paid by savings banks on customers' deposits (which ranged between 3.5 percent and 4 percent) or the yield on high-grade municipal bonds (3.9 percent to 4.2 percent). The fear was that individuals with pre-existing savings accounts or municipal bond holdings would use those funds to purchase Liberty Bonds if the bonds' promised return was greater than what a savings account was earning. Such a rearrangement of portfolios would not have increased saving or reduced consumption. McAdoo also knew that financial institutions would resist mightily any competition for their deposits from the government.

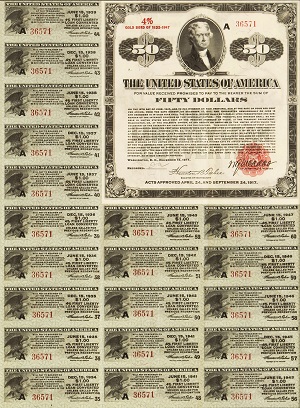

The bonds were negotiable, with coupons cashable every six months. Although their term was 30 years, they were callable after 15. The lowest denomination available was $50. This, it seemed to some, would put them out of reach for the general public. The average compensation of a production worker in manufacturing was approximately 35 cents per hour at the time. Fifty dollars would require two weeks of wages. But there was an obstacle to issuing lower denominations: The government did not want to deal with the administrative cost of tracking ownership, so it designated Liberty Bonds as "bearer bonds." These are securities that belong to whoever is holding them at the time rather than one registered owner. Had bearer bonds been issued in small denominations, they could be used like currency to purchase goods, thereby defeating McAdoo's reason for refusing to print money. They would be money.

McAdoo found another way to make the bonds affordable. He introduced an installment plan. Even the poorest could purchase "War Thrift Stamps," which cost only 25 cents. The Treasury Department called them "little baby bonds," and like the Liberty Bonds, they earned interest. The stamps were pasted on a card until 16 had been collected, at which point they were exchanged for a $5 stamp called a "War Savings Stamp." These were affixed to a "War Savings Certificate," which also earned interest. When 10 $5 stamps were collected, the certificate could be exchanged for a $50 Liberty Bond. The key to this scheme was that the certificate was registered to its owner and could be cashed only by the person whose name was inscribed on the certificate. That made the certificate non-negotiable.

Rallying the Public

Fears of inadequate demand were proved unwarranted. The first loan was oversubscribed by 50 percent, with more than 4 million subscribers accepted. Nationally, that would represent about one in every six households. Subscribers for the smallest amounts were given priority. Large subscribers were rationed. According to the New York Times, John D. Rockefeller, who pledged $15 million, was allotted only "something over $3 million." Fifty percent of the bonds sold were for the lowest face value, $50; another one-third of those sold were for the $100 bond.

In all, there were four Liberty Loan drives initiated during the war and a fifth "Victory Loan" announced after the armistice. The second Liberty Loan, for $3 billion, was open for six weeks and concluded on Nov. 15, 1917. The third and fourth drives were each about a month long in April ($3 billion) and October ($6 billion) of 1918. Because interest rates on alternative assets had risen, the rates on the subsequent loans were increased to keep them competitive, to 4 percent on the second loan and 4.25 percent on the third and fourth. All five campaigns were oversubscribed. Purchasers of the first 3.5 percent bonds could exchange their securities for the new higher-yielding bonds.

The loan drives were the subject of the greatest advertising effort ever conducted. The first drive in May 1917 used 11,000 billboards and streetcar ads in 3,200 cities, all donated. During the second drive, 60,000 women were recruited to sell bonds. This volunteer army stationed women at factory gates to distribute 7 million fliers on Liberty Day. The mail-order houses of Montgomery Ward and Sears-Roebuck mailed 2 million information sheets to farm women. "Enthusiastic" librarians inserted 4.5 million Liberty Loan reminder cards in public library books in 1,500 libraries. Celebrities were recruited. Charlie Chaplin, Mary Pickford, and Douglas Fairbanks, certainly among the most famous personalities in America, toured the country holding bond rallies attended by thousands.

This elaborate effort was conducted by a home-grown propaganda ministry called the "Committee on Public Information." The propaganda campaign was essential, not just to sell bonds, but to sell the war. Public sentiment before 1917 was not only against American involvement in the war, but it was not even united on which European military to root for. Running for re-election in 1916, Wilson had adopted the campaign slogan "He kept us out of war," and he pushed his argument for noninvolvement relentlessly. Wilson's Republican opponent, Charles Evans Hughes, was also for peace. So, not surprisingly, his administration needed a major campaign to convince the public of the necessity and the legitimacy of military action against Germany. This was a challenge because American involvement was not predicated on a desire for territory or revenge but on an intangible ideal. When asking for war on April 2, 1917, Wilson framed the war's objective: "The world must be made safe for democracy."

For the task of molding public opinion, Wilson turned to an investigative journalist, George Creel, who staffed the Committee on Public Information with psychologists, fellow journalists, artists, and advertising designers. The committee developed many of the techniques now associated with modern advertising. The magazine illustrator Howard Chandler Christy drew Liberty as an attractive young woman dressed in a see-through gown cheering on the troops. The man now regarded as the "father of public relations," Edward Bernays, also worked for Creel, pioneering the techniques of manipulating and managing public opinion based on the theories of mass psychology. The committee appealed to innate motives: the competitive (which city would buy the most bonds), the familial ("My daddy bought a bond. Did yours?"), guilt ("If you can't enlist, invest"), fear ("Keep German bombs out of your home"), revenge ("Swat the Brutes with Liberty Bonds"), social image ("Where is your Liberty Bond button?"), gregariousness ("Now! All together"), the impulse to follow the leader (President Wilson and Secretary McAdoo), herd instincts, maternal instincts, and — yes — sex. Bernays's uncle was Sigmund Freud.

A Gamble Pays Off

By war's end, after four drives, 20 million individuals had bought bonds — impressive given that there were only 24 million households at the time. More than $17 billion had been raised. In addition, the taxes collected amounted to $8.8 billion. Almost exactly two-thirds of the war funds came from bonds and one-third from taxes. This was a time when $17 billion was an almost unthinkably large number; an equal share of gross domestic product today would amount to $3.6 trillion. Most of McAdoo's bonds were purchased by the public, 62 percent of the value sold by one estimate. A government survey of almost 13,000 urban wage-earners conducted in 1918 and 1919 indicated that 68 percent owned Liberty Bonds. It seems undeniable that the emotional advertising campaign effectively produced a broad and strong desire to do one's part for the war effort by participating in this way. After the war, McAdoo's assistant in fiscal matters, Assistant Secretary Russell Leffingwell, described the loan campaigns "as the most magnificent economic achievement of any people. … the actual achievement of 100,000,000 united people inspired by the finest and purest patriotism."

McAdoo had taken a gamble when he depended on faith that Americans could be induced to save more heavily than they would otherwise. He won that gamble. Saving rates shot up during the war and then returned close to their prewar levels following the end of hostilities. Consumption as a percent of personal income fell during the war, by roughly 10 percentage points. McAdoo's faith in and reliance upon borrowing during a time of emergency proved the value of deficit spending and emboldened those who later advocated fiscal policy to fight business recessions and unemployment. McAdoo's belief that public opinion could be changed and mobilized to provide the will and the way to achieve great things provides a continuing foundation for an optimistic, progressive, and democratic view of our free-market capitalist economy.

Readings

Craig, Douglas B. Progressives at War: William G. McAdoo and Newton D. Baker, 1863-1941. Baltimore: Johns Hopkins University Press, 2013.

Glass, Carter. An Adventure in Constructive Finance: An Account of the Federal Reserve System. New York: Doubleday, Page and Co., 1927.

McAdoo, William G. Crowded Years: The Reminiscences of William G. McAdoo. Boston: Houghton Mifflin, 1931.

Mock, James R., and Cedric Larson. Words That Won the War: The Story of the Committee on Public Information, 1917-1919. Princeton: Princeton University Press, 1939.

Schuffman, Lawrence D. "The Liberty Loan Bond.![]() " Financial History, Spring 2007, vol. 113, pp. 18-19.

" Financial History, Spring 2007, vol. 113, pp. 18-19.

Sutch, Richard. "Financing the Great War: A Class Tax for the Wealthy, Liberty Bonds for All.![]() " Berkeley Economic History Laboratory Working Paper No. 2015-09, September 2015.

" Berkeley Economic History Laboratory Working Paper No. 2015-09, September 2015.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us