Special Issue on Economics Over the Life Cycle:

- Are the Kids All Right?

- Why Aren't More

Women Working? - The Mortality Gap

- Life Cycle Hypothesis

- Do Economists Ever Really Retire?

- Interview with

Jonathan Parker

Special Issue on Economics Over the Life Cycle:

Many worry that the Great Recession and mounting student debt have stunted millennials' financial development

Generation Y. Echo boomers. Millennials. They've been called many things, but one thing for sure is that those born between the early 1980s and late 1990s will shape the economy for decades to come. According to a recent Pew Research Center report, this group overtook baby boomers as the largest living generation in America in 2015.

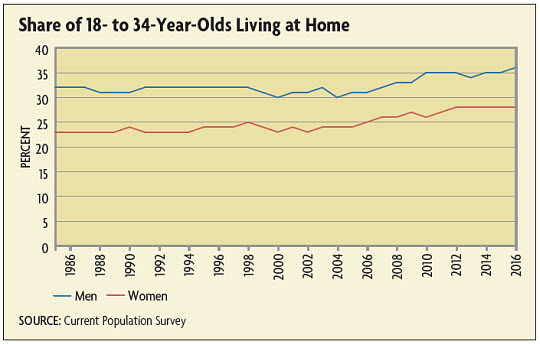

But some commentators also call them the Lost Generation, based on worries that the future doesn't look as bright for them as it did for previous generations. Many millennials graduated from college and began working just as the worst economic downturn since the Great Depression hit. They've also been called the Boomerang Generation: According to another Pew study, in 2014 roughly a third of those aged 18 to 34 lived with their parents, edging out marriage or cohabitation with a partner as the most common living arrangement for the first time in over a century. (See chart below.)

Millennials face other longer-term challenges as well. They are more likely to have student debt, and more of it, than previous generations. Since 2001 alone, the median value of student debt for those who took on loans has nearly doubled from $6,600 to $11,100, according to the 2013 Survey of Consumer Finances. And while parents have historically expected their children to be more prosperous than they were at the same age, there are signs that this may no longer be the case. A recent paper by Raj Chetty, David Grusky, and Maximilian Hell of Stanford University, Nathaniel Hendren and Robert Manduca of Harvard University, and Jimmy Narang of the University of California, Berkeley found that only half of the children born in the 1980s were earning more than their parents by age 30, compared to more than 90 percent of 30-year-olds born in 1940.

Some commentators have expressed concerns about the long-term consequences of these trends. Conventional financial wisdom holds that the earlier one starts building wealth and saving for retirement, the better. But if millennials are postponing or entirely avoiding homeownership and struggling with lower wages and higher debt burdens, it may take them much longer to achieve financial self-sufficiency — if they ever do. In addition to individual welfare implications, this would have repercussions for the economy as a whole.

But is the future as dire as it seems for millennials?

First Job, False Start

Finding a full-time job is often the first step young adults take on the path toward financial independence. This can be a challenge even in the best of times — and for millennials entering the labor market in 2008 and 2009, it was hardly the best of times. Rather than looking to hire, employers were shedding workers at a rapid pace. From the start of 2008 to the fall of 2009, the unemployment rate doubled from 5 percent to 10 percent. But while millennials faced higher unemployment rates during the Great Recession, they didn't suffer disproportionately worse job losses relative to older workers.

Still, even those millennials who managed to land their first job in the midst of the recession didn't necessarily escape the recession's curse. Several studies have documented persistent negative effects on wages for those who begin their careers during economic downturns. For example, a 2012 article by Philip Oreopoulos of the University of Toronto, Till von Wachter of the University of California, Los Angeles, and Andrew Heisz of Statistics Canada found that a 5 percentage point increase in unemployment rates translated to as much as a 9 percent initial loss in earnings for recent male college graduates in Canada.

A 2016 article by Joseph Altonji and Lisa Kahn of Yale University and Jamin Speer of the University of Memphis found a similar effect for U.S. graduates. In both cases, the authors attributed these effects to the fact that young adults graduating in a recession have fewer job options, leading them to choose less desirable and lower-paying employers than they would have in better times. Starting out on a lower rung also negatively affected their climb up the job ladder, meaning that these wage effects can persist for up to a decade. They also found that the losses for recent graduates during the Great Recession were much larger than in previous recessions going back to 1974.

And yes, one of the ways that graduates have compensated for weaker labor market opportunities is by choosing to live with parents longer. An analysis of data from the Current Population Survey and Consumer Expenditure Survey in a 2015 paper by Daiji Kawaguchi of Hitotsubashi University and Ayako Kondo of Yokohama National University found that higher unemployment rates increase the probability that recent graduates live at home with parents. The authors argued that young adults use this option as a sort of "intergenerational insurance mechanism" to smooth their consumption. As a result, recent graduates did not reduce their consumption as drastically as would be expected from the recession.

Building Wealth in a Recession

A weak job market was not the only effect the Great Recession had on millennials just starting out, however. The collapse of the housing and financial markets had a profound effect on the wealth of young and old households alike.

On the bright side for millennials, young adults are less likely to own assets like stocks or homes than older cohorts, which may have insulated them somewhat from turmoil in those markets. Indeed, a 2014 paper by Lisa Dettling and Joanne Hsu of the Federal Reserve Board of Governors found that, on average, young adults suffered less of a decline in net worth than older adults during the Great Recession. Still, those who owned a home or stocks did take a hit. Millennials' median net worth fell by almost 40 percent, from about $10,000 in 2004 to about $6,000 in 2013. This decline was particularly concentrated among the college educated.

Falling asset prices weren't completely bad for millennials, though. Young adults had the opportunity to benefit from lower stock and house prices by buying into markets after the crash and reaping the benefits of the recovery. But buying stocks during a financial crisis runs counter to most peoples' inclinations. In a 2011 article in the Quarterly Journal of Economics, Ulrike Malmendier of the University of California, Berkeley and Stefan Nagel of the University of Michigan found that individuals who have experienced low stock market returns are less willing to take on financial risk or participate in the stock market at all and are more pessimistic about future returns if they do participate. Young individuals are particularly influenced by recent experiences, since they have fewer lifetime experiences to draw from.

"If you look at the average experience that a millennial has had with the stock market over the past 10 to 15 years, it certainly looks different than what a young person would have seen in, say, 1998," says Nagel. "These cohorts have quite different experiences, and as such they would be less willing to take risks than these earlier cohorts."

In fact, Nagel says that young people, like many individual investors in general, tend to invest in the stock market when returns are high and pull out of the market when returns are low — the opposite of what would maximize their returns and minimize the damage from recessions.

Young adults may also face constraints building other forms of wealth. Owning a home not only provides a place for an individual or family to live, it also represents a significant asset. But purchasing a home typically require access to credit, and young adults are more credit constrained than older cohorts. Lenders might also tighten standards in response to a market crash as they did during the Great Recession.

Credit constraints like these may limit how much young adults can benefit from lower asset prices during a recession. In a 2016 paper, Sewon Hur of the University of Pittsburgh constructed a model that included borrowing constraints for young adults. Hur estimated that young adults suffered the largest overall welfare losses of any age group during the Great Recession, equivalent to a 7 percent decline in lifetime consumption.

Shouldering Student Debt

The Great Recession, while certainly a significant event in the lives of many millennials, doesn't seem to fully explain their pattern of behavior. In fact, some studies, like a 2015 article by Marianne Bitler of the University of California, Davis and Hilary Hoynes of the University of California, Berkeley, have found little relationship between changes in unemployment and young adults moving in with their parents. The bigger influence, some believe, is debt.

While it is true that student debt burdens have been rising on average for decades, it's not entirely clear what impact this is having on the decisions of young adults. The news is full of stories of recent grads struggling to pay down five- and six-figure student loans. But those cases are more the exception than the rule, according to economist Beth Akers of the Manhattan Institute, co-author of the 2016 book Game of Loans.

"The median borrower is spending about 4 percent of their monthly income on student loan repayment," says Akers. "If you look at the data on household expenditures, that's similar to the category of personal entertainment."

Calls to reduce student debt burdens also often assume other things are held constant. "Of course, most young adults would like an extra $275 or so a month," says Akers. "But if we think about debt as allowing people to make investments in higher education, then removing that debt but also taking away the degree and the earning power that comes with it would almost certainly reduce homeownership rates and retirement savings."

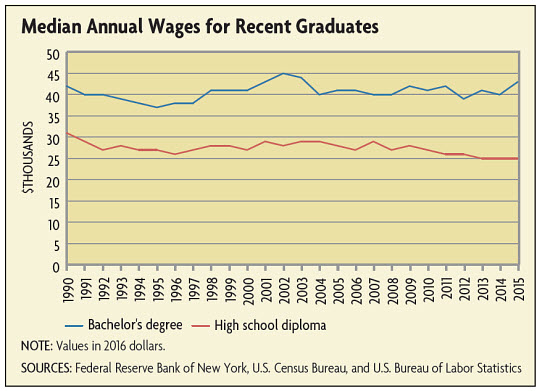

Indeed, despite rising college costs, the returns to higher education are still substantial. A 2014 New York Fed study estimated that for the last decade, the return from spending on a college degree has been about 15 percent, making it still one of the best investments an individual can make. But it is a return that depends on finishing the degree as well as the field of study, meaning that some can end up with the debt and little to show for it. Moreover, the consistent returns to higher education somewhat mask a trend of worsening outcomes for young adults who don't go to college. (See chart below.)

"The rate of return on higher education has held up over time and been about constant for the past decade, but part of what's keeping that in place is that the alternative is getting worse," says Akers. "In essence, it is getting more expensive not to go to college."

Indeed, the changes in living arrangements for millennials don't necessarily point to a choking effect from student debt but rather to a growing divide between those who finish college and those who don't. According to a 2016 report by Richard Fry of Pew Research Center, 40 percent of 18- to 34-year-old high school dropouts and 39 percent of high school graduates lived with their parents in 2014, compared to just 19 percent of college graduates.

Different Dreams or Deferred Dreams?

How will millennials stack up to their older siblings and parents in the long run? It is a difficult question to answer, in large part because the story of this generation is still being written.

If changing patterns of household formation reflect a response to the Great Recession, then those patterns may reverse as that event fades into memory. Still, that process could take a long time. In terms of risk-taking and the stock market, "even things that happened 30 years ago still play some meaningful role," says Nagel.

But there is some evidence to suggest that at least in the housing market, retrenchment in response to crises won't last forever. A 2015 article by Renata Bottazzi and Matthew Wakefield of the University of Bologna and Thomas Crossley of the University of Essex studied homeownership rates in England over the past 40 years. They found that although individuals who experienced a decline in the housing market when young reduced their homeownership rates, that same cohort looked largely the same as earlier generations by the time they reached age 40. In essence, generations that exhibit historically low homeownership rates while young seem to "catch up" as they age.

Data suggest such a catch-up may be taking place among millennials in the United States. Older cohorts who were in their mid-to-late 20s when the recovery began in 2010 exhibited larger gains in homeownership by 2014 than younger millennials. Still, there's always the possibility that this generation will be different. Evidence from the Great Recession suggests that both young adults and their parents have become more accepting of living together longer. Additionally, delayed homeownership may partly be a symptom of changing trends in family formation. During the height of the nuclear family era in 1960, 62 percent of young adults were married or cohabiting with a partner by their early 30s. But nearly half as many millennials, 31.6 percent, were doing so at the same age in 2014.

What will delays in homeownership mean for millennials on an individual level and for the economy as a whole? The Survey of Consumer Finances provides a picture of young adult millennials who were living independently in 2013 and suggests that they are not doing substantially worse on average than previous cohorts. They are more likely than young adults in 1989 — members of Generation X — to own a bank account, a home, retirement accounts, and stocks. And while their student debt is much higher on average, other forms of debt like credit cards, housing, and car loans are lower than for the median young adult in 1989. And that higher student debt comes with a benefit. Millennials have received more college education than any other generation in American history. In particular, female millennials are significantly more likely to have a bachelor's degree than their Baby Boom or Gen X counterparts.

But what about those left behind? Non-college graduates and some college graduates are increasingly struggling to achieve the American dream. It may be that the data on this generation reflect this divide. While some of the kids look to be all right, for others, only time may tell.

Readings

Akers, Beth, and Matthew M. Chingos. Game of Loans: The Rhetoric and Reality of Student Debt. Princeton, N.J.: Princeton University Press, 2016.

Altonji, Joseph G., Lisa B. Kahn, and Jamin D. Speer. "Cashier or Consultant? Entry Labor Market Conditions, Field of Study, and Career Success." Journal of Labor Economics, January 2016, vol. 34, no. S1, part 2, pp. S361-S401. (Working paper version available online.)

Chetty, Raj, David Grusky, Maximilian Hell, Nathaniel Hendren, Robert Manduca, and Jimmy Narang. "The Fading American Dream: Trends in Absolute Income Mobility Since 1940." National Bureau of Economic Research Working Paper No. 22910, December 2016. (Previous version available online.)

Dettling, Lisa. "Effects of Entering Adulthood during a Recession." IZA World of Labor Article No. 242, April 2016.

Dettling, Lisa J., and Joanne W. Hsu. "The State of Young Adults' Balance Sheets: Evidence from the Survey of Consumer Finances." Federal Reserve Bank of St. Louis Review, Fourth Quarter 2014, vol. 96, no. 4, pp. 305-330.

Malmendier, Ulrike, and Stefan Nagel. "Depression Babies: Do Macroeconomic Experiences Affect Risk Taking?" Quarterly Journal of Economics, February 2011, vol. 126, no. 1, pp. 373-416. (Working paper version available online.)

Oreopoulos, Philip, Till von Wachter, and Andrew Heisz. "The Short- and Long-Term Career Effects of Graduating in a Recession." American Economic Journal: Applied Economics, January 2012, vol. 4, no. 1, pp. 1-29.

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.