Federal Reserve MBS Purchases in Response to the COVID-19 Pandemic

Economic Brief

July 2020, No. 20-08

The Federal Reserve's purchases of agency mortgage-backed securities — launched in response to financial disruptions caused by COVID-19 — appear to have restored smooth market function supporting the continued flow of credit to mortgage borrowers. However, the amount of purchases necessary to achieve this outcome raises concerns about the resilience of private-market structures that perform this critically important function.

In the wake of the 2007–08 financial crisis and during the ensuing Great Recession, the Federal Reserve introduced a number of new, or unconventional, monetary policy tools.1 Among them were purchases of agency mortgage-backed securities (agency MBS), conducted in two waves of the Fed's large-scale asset purchase (LSAP) program.2 Similarly, in March 2020, in response to the emerging COVID-19 pandemic, the Federal Reserve launched a new agency MBS purchase program in addition to other policy actions.3 This Economic Brief provides a short overview of this purchase program, its objectives, implementation, impact on the agency MBS market, and effects on mortgage rates more broadly.

The MBS market is an important tool for mortgage funding. An MBS is a security backed by a pool of mortgage loans, where principal and interest payments made by mortgage borrowers are passed on to MBS investors. MBS issued by U.S. government-backed enterprises (Fannie Mae and Freddie Mac) or a U.S. government agency (Ginnie Mae) are enhanced by a credit guarantee, where repayment of principal and interest is guaranteed (indirectly or directly) by the federal government. Such agency MBS comprise the bulk of all MBS in the United States, and the agency MBS market is large. As of May 2020, the outstanding amount of agency MBS backed by fixed-rate residential mortgages was $6.3 trillion. Typically, the agency MBS market is also very liquid. The average trading volume in May 2020 stood at close to $320 billion per day.4

Effects of the Pandemic

In March 2020, it became apparent that the emerging COVID-19 pandemic would weigh very heavily on economic activity in the short term, with medium- and long-run impacts highly uncertain. In two policy actions, announced on March 3 and March 15, the Federal Open Market Committee (FOMC) reduced the federal funds target rate (its primary policy rate) to nearly zero.5 At the same time, very significant strains emerged in financial markets.

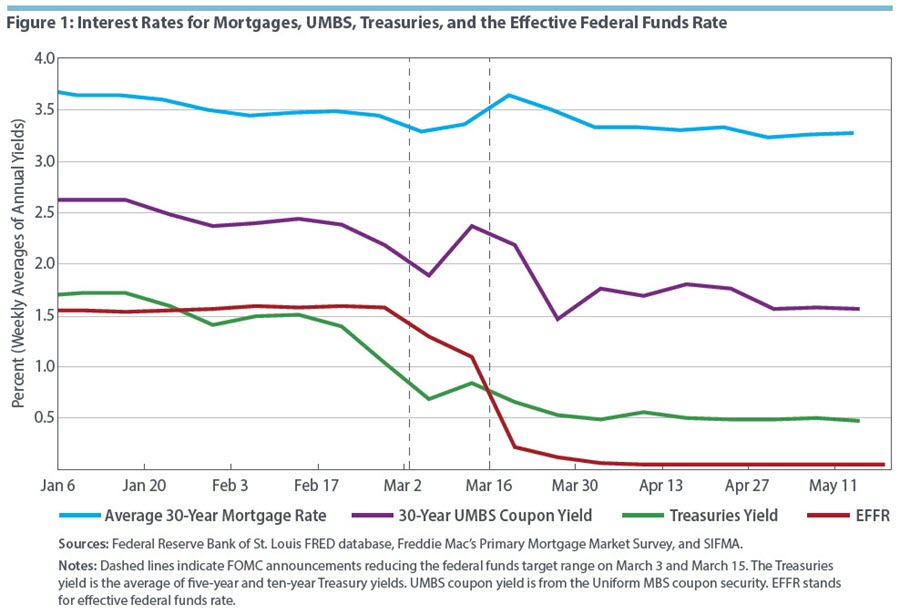

Figure 1 shows the realized path of the weekly average effective federal funds rate (EFFR) for 2020 through the week of May 18. Consistent with the two FOMC policy actions, marked by vertical dashed lines in the figure, the EFFR dropped from 1.5 percent at the end of February to nearly zero at the end of March. Figure 1 also presents the paths of three cost-of-funding rates for U.S. borrowers realized over the same period: a medium-term Treasuries yield, an MBS yield, and an average thirty-year mortgage rate quoted to retail mortgage borrowers.6 As a sign of strain in financial markets, we can observe in this figure a divergence between the direction of change in the policy rate and in the three cost-of-funding rates during the first two weeks of March.

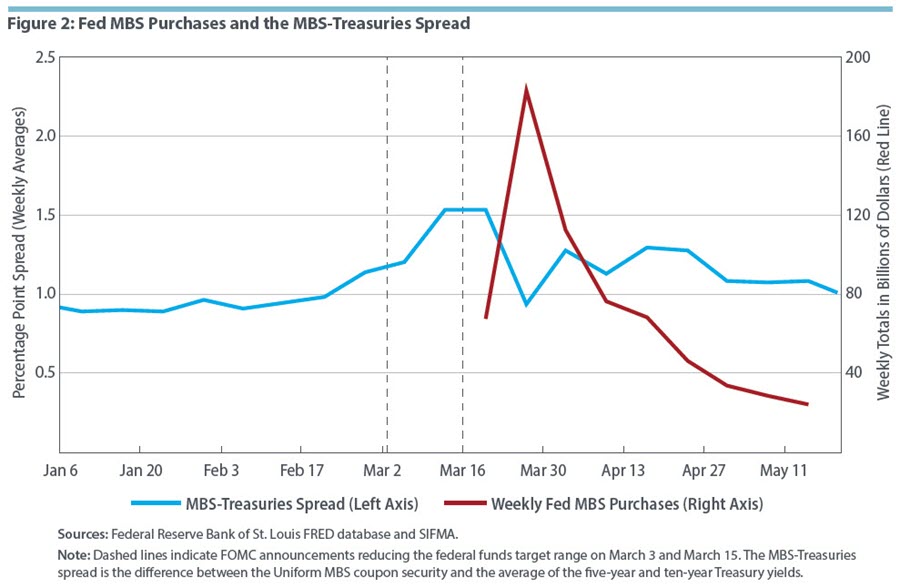

Concurrently, the Treasury-debt and MBS markets experienced significant liquidity disruptions. In March, the bid-ask spread in the Treasury-debt market increased thirteenfold.7 Focusing on the MBS market, Figure 2 plots the weekly average spread between the MBS yield and the medium-term Treasuries yield. Prior to the onset of the COVID-19 pandemic, this spread stood at about 90 basis points and was very stable. Over a four-week period spanning February and March, it grew by more than 50 percent, and by March 13, the spread had reached 165 basis points. Additionally, daily readings of this spread showed extreme volatility over the same period. Since MBS are an important funding source for retail mortgage originators, such disruptions to the smooth functioning of the MBS market are concerning, particularly during a time of monetary policy easing when high volumes of MBS issuance are expected.8

New Agency MBS Purchasing

To restore smooth function in the MBS market, the FOMC launched a new MBS purchase program in March 2020. Specifically, the March 15 FOMC statement called for the Fed to increase its holdings of agency MBS by "at least $200 billion" during the "coming months."9 Implementing this FOMC directive, the trading desk at the Federal Reserve Bank of New York was able to commence MBS purchases on Monday, March 16. During the first week of the program's operation, the trading desk purchased a total of $67.7 billion of par face value of MBS, that is, one-third of the $200 billion amount announced in the March 15 FOMC statement. This volume of purchases exceeded the pace of purchases in previous Fed MBS purchase programs. Specifically, the original Fed MBS purchase program, announced under similar market-dysfunction conditions in November 2008, operated at an average pace of about $60 billion per month.10

Despite the strong Fed intervention, signs of market dysfunction did not subside during the week of March 16. With daily volatility exceeding three standard deviations, the MBS-Treasuries spread actually increased during the week to reach 180 basis points on Friday, March 20.

On Monday, March 23, the FOMC instructed the trading desk to "continue to purchase Treasury securities and agency MBS in the amounts needed to support smooth market function and effective transmission of monetary policy to broader financial conditions," thus removing all caps on the volume of purchases to be conducted by the desk. Consequently, on the same morning, the desk announced its plan "to conduct operations totaling approximately $75 billion of Treasury securities and approximately $50 billion of agency MBS each business day this week, subject to reasonable prices."

Figure 2 shows total MBS purchases conducted in the first two months of the program's operation. During the week of the March 23 FOMC action, the purchases reached the peak of $183.3 billion. The pace of purchases was then gradually reduced. During the week of May 11, the pace of purchases settled at $22.5 billon per week.11 Figure 2 also presents the weekly average MBS-Treasuries spread. Having increased by about 60 basis points between early February and mid-March, this measure of stress in the MBS market remained flat in the first week of the Fed's new MBS purchase program. In the second week, following the March 23 FOMC announcement authorizing unlimited purchases, the spread completely reverted to its precrisis level of about 90 basis points, then increased again to about 120 basis points, and then slowly declined over the next month and a half.

These data suggest that the purchase program did achieve the FOMC's objective of restoring smooth function in the MBS market. As seen in Figure 1, MBS yields declined rapidly, and the spike in retail mortgage rates reverted, leading to a gradual decline in the cost of funding for purchasing or refinancing a home.

However, the data also highlight the difficulty in calibrating the policy response under market stress conditions when, due to price dislocations, market prices cannot be relied on to calibrate the strength or volume of market intervention. Figure 2 suggests that the Fed's purchase volumes initially undershot and then overshot the intervention levels consistent with a gradual return of the MBS-Treasuries spread to levels consistent with smooth market function. Among the unintended consequences of the massive swings in MBS yields observed in the second half of March were margin calls faced by mortgage originators on the derivative positions they routinely maintain to hedge their origination pipeline risk.12 Over a longer term, increased mortgage credit supply may push up house price inflation and make housing less affordable.13

Summary

The Fed's decisive policy action in the MBS market, taken in response to market disruptions caused by the COVID-19 pandemic, appears to have been effective at restoring smooth market function and ensuring the uninterrupted flow of credit to mortgage borrowers. The scale of the intervention needed to achieve this outcome, however, raises a concern about the resilience of the existing private-market structures serving the critically important function of intermediating the flow of mortgage credit in the United States. Research into potential reforms that would strengthen the resilience of this market to future shocks is needed.14

Borys Grochulski is a senior economist in the Research Department at the Federal Reserve Bank of Richmond.

1

See Glenn D. Rudebusch, "A Review of the Fed's Unconventional Monetary Policy," Federal Reserve Bank of San Francisco Economic Letter 2018-27, December 3, 2018.

2

The first wave of agency MBS purchases was announced in November 2008 and the second one in March 2012. See Simon Potter, "The Federal Reserve's Experience Purchasing and Reinvesting Agency MBS," remarks at the Bank of England, London, U.K., March 07, 2019.

3

The COVID-19 section of the Federal Reserve website provides a comprehensive list of the Fed's policy actions taken in response to COVID-19, including a detailed timeline.

4

For comparison, the U.S. corporate bond market stood at $9 trillion, with an average daily volume of $34 billion, during the same period. Data are from the Federal Reserve Bank of St. Louis FRED database and SIFMA.

5

Specifically, the target range for the federal funds rate was reduced by 0.5 percentage points, to 1–1.25 percent, on March 3 and again by 1 percentage point, to 0–0.25 percent, on March 15.

6

The Treasuries yield is the average of the five-year and ten-year Treasury yields. The UMBS yield represents the Uniform MBS coupon security. The average thirty-year mortgage rate comes from Freddie Mac's Primary Mortgage Market Survey.

7

See Figure 3 in Lorie K. Logan, "The Federal Reserve’s Recent Actions to Support the Flow of Credit to Households and Businesses," remarks before the Foreign Exchange Committee, Federal Reserve Bank of New York, April 14, 2020.

8

For more information about the structure of the MBS market, see James Vickery and Joshua Wright, "TBA Trading and Liquidity in the Agency MBS Market," Federal Reserve Bank of New York Economic Policy Review, May 2013, vol. 19, no. 1, pp. 1–18.

9

Concurrently, the FOMC initiated a program of Treasury bond purchases of "at least $500 billion" to support smooth function in that market.

10

See Figure 3 in Potter (2019).

11

This pace has been maintained through June (not shown in Figure 2).

12

See Mark Sorohan, "MBA Raises Concerns with SEC on Broker-Dealer Margin Call Volatility," Mortgage Bankers Association MBA Newslink, March 30, 2020.

13

For evidence on the impact of credit-supply expansions on housing-price inflation, see, for example, Giovanni Favara and Jean Imbs, "Credit Supply and the Price of Housing," American Economic Review, March 2015, vol. 105, no. 3, pp. 958–992; also, see Alejandro Justiniano, Giorgio E. Primiceri, and Andrea Tambalotti, "Credit Supply and the Housing Boom," Journal of Political Economy, June 2019, vol. 127, no. 3, pp. 1317–1350.

14

See, for example, You Suk Kim, Steven M. Laufer, Karen Pence, Richard Stanton, and Nancy Wallace, "Liquidity Crises in the Mortgage Market," Brookings Papers on Economic Activity, Spring 2018, pp. 347–428, for analysis of vulnerabilities in the nonbank mortgage-origination pipeline. Darrell Duffie, "Still the World's Safe Haven? Redesigning the U.S. Treasury Market after the COVID-19 Crisis," Hutchins Center Working Paper No. 62, Brookings Institution, June 2020, discusses proposals for increasing the resilience of the Treasury-debt market.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us