Macroeconomic Effects of Household Pessimism and Optimism

Economic Brief

January 2021, No. 21-03

Survey data on households' expectations about macroeconomic outcomes reveal systematic differences from statistical (or rational) forecasts. We construct an empirical measure of these differences, which we refer to as "belief wedges." Across economic variables, such as inflation and unemployment, these belief wedges are significant and move in parallel with the business cycle. We present a theory of time-varying belief wedges that accounts for these empirical facts. Our theory provides a formal interpretation of these wedges as pessimism and optimism. Embedding the theory into a quantitative macroeconomic model, we show that belief wedges drive a substantial share of movements in macroeconomic aggregates, particularly in the labor market.

Expectations about the future are important drivers of the economy. For instance, a more pessimistic outlook can lead households to save more and firms to hire less. These individual decisions can lead to aggregate fluctuations in output, employment and prices. Survey data allow us to measure how the expectations of different economic agents fluctuate over time, providing evidence to test theories of expectation formation and allowing us to quantify their effects.

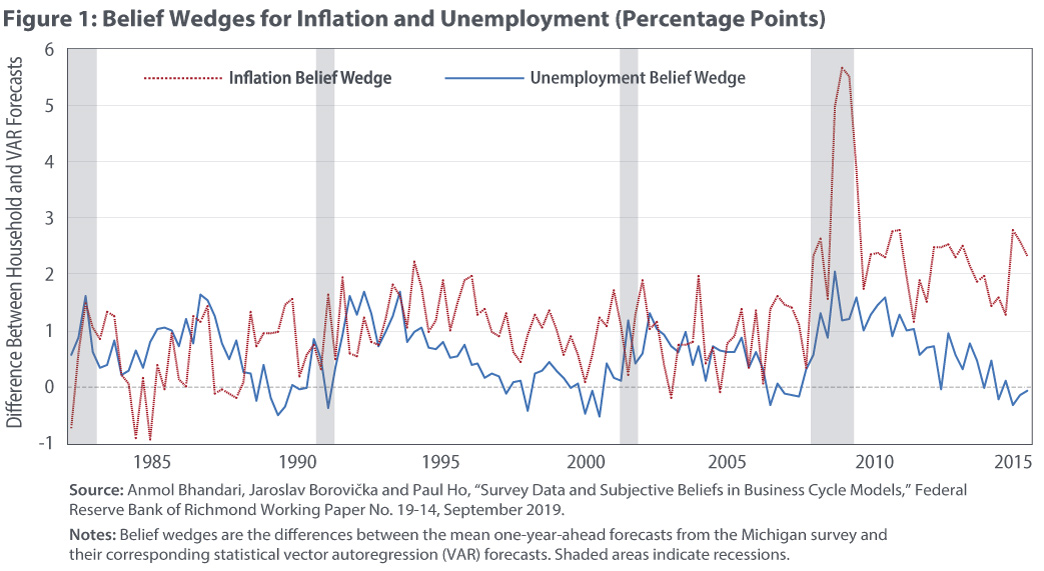

In a recent working paper, we document systematic biases in household forecasts for unemployment and inflation in both time-series and cross-sectional data.1 Using the University of Michigan Surveys of Consumers (Michigan survey), we show that household forecasts for unemployment and inflation are biased upward on average relative to a statistical forecast and that both biases increase significantly during recessions. We refer to this difference between the household and statistical (or rational) forecasts as a "belief wedge." Furthermore, in the cross section, households that expect higher inflation relative to the population also tend to expect higher unemployment. In line with evidence from the Bank of England/Kantar Inflation Attitudes Survey linking higher inflation to lower expectations of economic conditions, we interpret the forecasts of higher unemployment and inflation as pessimism.2

We develop a quantitative model of time-varying pessimism and optimism that is consistent with these facts. In contrast to the rational-expectations framework, in which the expectations of economic agents equal the model-implied forecasts, pessimistic households in our model overestimate (and optimistic households underestimate) the probability of adverse future outcomes relative to the model-implied forecast. This time-varying pessimism and optimism provides a parsimonious way to match all our documented empirical facts. Although our theory allows for optimism, we find that household survey data are consistent with pessimism on average. This explains the average upward biases in household forecasts of unemployment and inflation. Furthermore, increases in pessimism lead to larger upward biases for both unemployment and inflation and are accompanied by an economic contraction.

The model reveals that pessimism has important effects on the aggregate economy. In particular, fluctuations in pessimism account for a large fraction of the variation in unemployment. Pessimism affects the macroeconomy through households reducing current demand and firms posting fewer job vacancies. In addition, a fear of higher future costs reduces incentives for firms to lower prices despite lower demand from households.

Key Empirical Facts

We obtain data on households' expectations from the Michigan survey, which interviews households about their views on current and future economic conditions. To derive belief wedges, we compare these household forecasts to a statistical forecast from a vector autoregression (VAR) for the first quarter of 1982 through the fourth quarter of 2015. We plot the resulting belief wedges in Figure 1 for both inflation and unemployment. Again, based on evidence from the Bank of England survey, we interpret positive values in Figure 1 as indicators of pessimism and negative values in Figure 1 as indicators of optimism.

We document three key facts. First, households forecast higher unemployment and higher inflation on average, relative to the statistical forecast, with mean belief wedges of 0.58 percent and 1.25 percent, respectively, over the sample period. Second, these wedges are positively and significantly correlated. Third, the wedges tend to be higher during periods of lower GDP growth. These patterns are robust to other approaches of measuring belief wedges, such as replacing the statistical forecast with forecasts from the Survey of Professional Forecasters or replacing the household forecasts with those from the Federal Reserve Bank of New York Survey of Consumer Expectations. The positive correlation between unemployment and inflation forecasts shows up in the cross section as well — households that predict higher inflation also predict higher unemployment.

Pessimism as a Model for Belief Wedges

To better understand the belief wedges, we seek a theory that can explain all three facts. To that end, we build on work by Lars Peter Hansen of the University of Chicago and Thomas J. Sargent of New York University to develop a model of time-varying pessimism and optimism.3 Pessimism is captured by households overestimating the probability of adverse future outcomes, while optimism is captured by households underestimating the probability of adverse future outcomes. The amount of overestimation or underestimation is determined by a single variable that fluctuates over time. We refer to this variable as the “belief shock.” When the belief shock is high, households are more pessimistic and forecast higher unemployment and inflation relative to what the model predicts.

In Figure 2, we plot an average of the standardized belief wedges (that is, the principal component of the belief wedges) as a proxy for the belief shock. We find a high positive correlation with the sentiment indexes produced by the Michigan survey and the Conference Board, suggesting that our model of pessimism also provides a theory for these often-cited sentiment indexes. However, unlike the sentiment indexes, our belief wedges have quantitative counterparts in macroeconomic models, allowing us to quantify the effect of time variation in pessimism on the macroeconomy.

While numerous theories in the literature can explain parts of the belief wedge behavior, the challenge is finding a parsimonious way to capture all three of our key empirical facts. For example, we show in our paper that models of sticky or noisy information, in which households do not fully update their forecasts in the presence of news, can explain the cyclical behavior of the inflation belief wedge. But those models do not explain the cyclical behavior of the unemployment belief wedge or the average wedge. On the other hand, over-extrapolation of news by households can explain the cyclical behavior of the unemployment belief wedge but not the rest of the facts. While we cannot rule out the validity of such alternative behavioral theories, the data do suggest that there is an additional mechanism driving the belief wedges, a gap that our theory of time-varying pessimism fills.

Quantitative Effects of Fluctuations in Pessimism

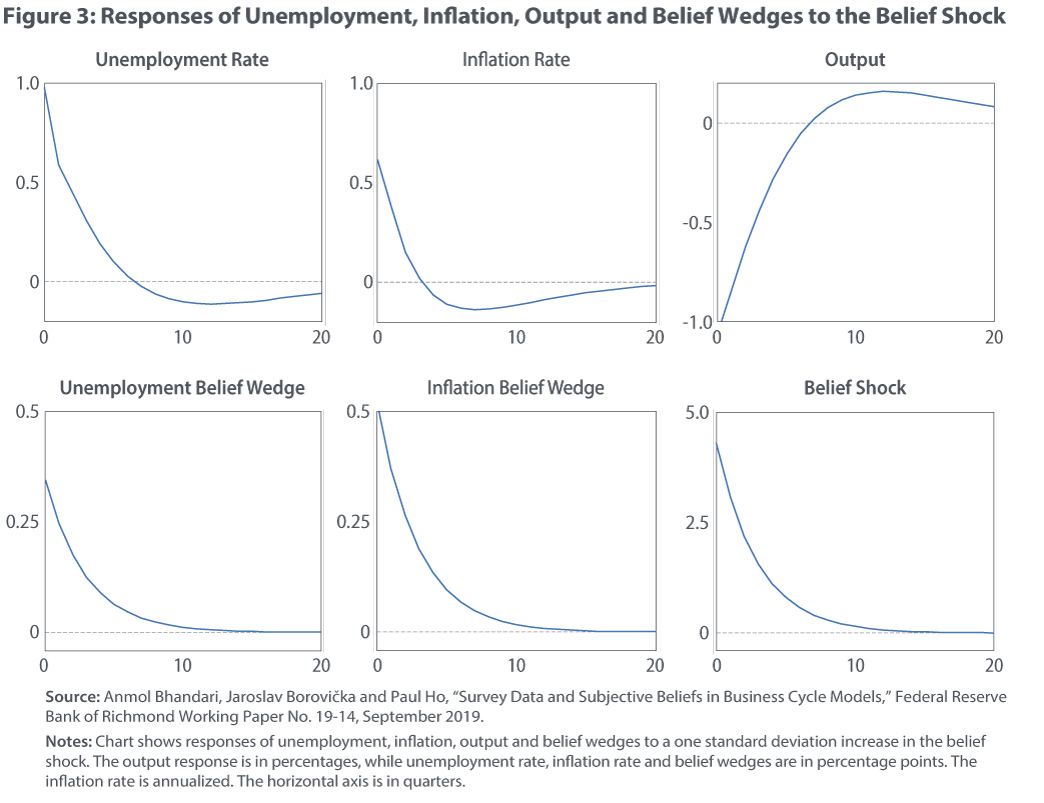

The correlation of the belief wedges with GDP growth invites the question of how much they influence macroeconomic aggregates. To answer this question, we embed time-varying pessimism into a relatively standard quantitative macroeconomic model that is consistent with the empirical evidence: An increase in pessimism is contractionary and increases the belief wedges for both inflation and unemployment forecasts, as shown in Figure 3.

Figure 3 shows that a one standard deviation increase in pessimism leads contemporaneously (at quarter zero) to a 1 percent decrease in output and a 1 percentage point increase in the unemployment rate. Inflation increases for a short period but decreases afterward, with a 10-quarter cumulative response of approximately zero. Over the sample period, the belief shock was particularly important for driving unemployment during the dot-com boom and the Great Recession, with the decrease in unemployment in the late 1990s attributed to relative optimism among households and much of the increase in unemployment around 2008–09 accounted for by an increase in pessimism.

The aggregate effects arise because pessimistic households expect a combination of negative shocks to the economy. In our model, this corresponds to a decline in productivity, a tightening of monetary policy and a further increase in pessimism, all occurring simultaneously. Households that are more pessimistic reduce their current demand to smooth consumption over time. Firms setting prices expect lower future productivity and hence higher marginal costs, a scenario that reduces their incentives to lower prices. In addition, firms’ pessimism lowers the value of hiring workers, which increases unemployment due to a reduction in posting job vacancies. In equilibrium, the decline in output and increase in unemployment due to an increase in pessimism are accompanied by a muted inflation response.

Conclusion

We document systematic differences between household and statistical forecasts and propose a theory of time-varying pessimism that accounts for these wedges. Embedding this theory into a quantitative macroeconomic model, we find that fluctuations in pessimism have economically significant effects on macroeconomic aggregates, most notably unemployment.

In the past few years, an increasing number of papers have studied the joint behavior of expectations for different economic variables. In the time series, Olivier Coibion of the University of Texas and Bernardo Candia and Yuriy Gorodnichenko of the University of California at Berkeley documented that across numerous surveys in both the United States and Europe, households tend to forecast higher inflation when they expect lower output growth, consistent with the belief wedge comovement we have documented.4 In the cross section, Rupal Kamdar of Indiana University documented similar correlations in the Michigan survey across a wide range of variables and has provided an alternative theory of optimism and pessimism.5 This body of work recognizes that theories of how households form expectations should be understood and tested in the context of a broad set of empirical facts, rather than focusing on forecasts of one variable or one statistic at a time.

Beyond households, it is crucial to acknowledge the range of beliefs in the economy. The growing plethora of surveys allows us to compare the forecasts of different groups (for example, the Survey of Professional Forecasters, CFO Survey, and Gallup Investor Survey). Our theory of pessimism predicts systematic heterogeneity in beliefs due to different economic agents perceiving different outcomes as adverse. Our framework has the flexibility to incorporate these heterogeneous beliefs.

These expectations do not exist in a vacuum. Rather, they directly influence the decisions of households and firms. Analyzing these expectations is therefore important for understanding a wide range of outcomes, including business cycles, portfolio choices and labor market behavior. Moreover, our theory introduces an "expectations-management" component to policy making, since policy decisions change the type of shocks that matter to economic agents and, as a result, affect their forecasts. The measurement and modeling of these expectations are thus crucial from both academic and policy standpoints.

Anmol Bhandari is an assistant professor of economics at the University of Minnesota, and Jaroslav Borovička is an associate professor of economics at New York University. Paul Ho is an economist in the Research Department at the Federal Reserve Bank of Richmond.

1

For a full account of our research, see Anmol Bhandari, Jaroslav Borovička and Paul Ho, "Survey Data and Subjective Beliefs in Business Cycle Models," Federal Reserve Bank of Richmond Working Paper No. 19-14, September 2019.

2

This quarterly survey, conducted by Kantar Omnibus on behalf of the Bank of England, assesses public attitudes about inflation.

3

Lars Peter Hansen and Thomas J. Sargent, "Robust Control and Model Uncertainty," American Economic Review, May 2001, vol. 91, no. 2, pp. 60–66.

4

Bernardo Candia, Olivier Coibion and Yuriy Gorodnichenko, "Communication and the Beliefs of Economic Agents," Manuscript, July 2020.

5

Rupal Kamdar, "The Inattentive Consumer: Sentiment and Expectations," Manuscript, December 2019.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us