High Labor Market Churn During the 2020 Recession

Economic Brief

February 2021, No. 21-06

Richmond Fed research has found that job losses during the COVID-19 recession have been concentrated in high-turnover sectors, with turnover rates in those occupations even higher than they were during the Great Recession. Workers displaced from high-turnover occupations often avoid long periods of unemployment, but they are historically less likely to develop long-term employment relationships, which limits their potential for sustained wage growth.

The original version of this brief contained a table, which was removed on March 2 to correct a coding error.

One way the current pandemic-induced recession stands apart from previous recessions is the high level of labor market churn. Loosely speaking, labor market churn refers to the pace of reallocation of workers and jobs, that is, the magnitude of job creation and job destruction flows alongside the size of hiring and separation flows. A high-churn labor market is characterized by workers cycling through different jobs and between employment and nonemployment at a high pace.1 This Economic Brief shows that the labor market in the COVID-19 recession displayed a higher level of churn than in the Great Recession of 2007–09. It also discusses the interpretation of these data and the implications for policy.

Data on labor market flows clearly show that job losses during the COVID-19 recession have been concentrated in high-turnover sectors and that turnover rates in these occupations have been even higher than during the Great Recession. The faster pace of worker reallocation across occupations is both a blessing and a curse: On one hand, workers displaced from high-turnover occupations are less likely to experience persistent nonemployment spells because they often become reemployed in sectors that use similar skills. For example, workers previously employed in the personal care services sector often transition into sales occupations and vice versa. On the other hand, workers employed in these occupations are historically less likely to develop long-term employment relationships, which limits their potential for sustained wage growth in the medium run and long run. The increased pace of separations and turnover during the COVID-19 recession may further exacerbate this limitation.

The Flow Approach to Labor Markets

Some labor market indicators are merely snapshots of what the labor market looks like at any point in time — for example, the employment-to-population ratio, the labor force participation rate or the unemployment rate. Other approaches to labor market analysis focus on changes, rather than levels, in the employment and unemployment rates with the goal of depicting labor market dynamics. This type of analysis is commonly referred to as the flow approach to labor markets. This approach captures the frequency at which U.S. workers cycle across jobs and between employment and nonemployment, providing a more nuanced perspective on employment inflows and outflows.

Current Population Survey (CPS) data allow researchers to estimate average monthly flows of individuals among employment, unemployment and the labor force, as well as between jobs. A seminal 2006 article by Steven J. Davis of the University of Chicago, R. Jason Faberman of the Chicago Fed and John C. Haltiwanger of the University of Maryland pioneered the interpretation of these flows.2 Job creation and job destruction are job flows, while hires and separations are worker flows. The sum of worker flows and job flows is called "total labor market churn." These flows are quite large: In an average month, we see 122 million employed people, 2.8 million people who change jobs, 1.4 million who become unemployed and 3 million who exit the labor force from employment. Similarly, we have 6.2 million unemployed people, 1.8 million who become employed and 1.4 million who exit the labor force from unemployment. Finally, in an average month, we have 59.3 million people who are not in the labor force, 1.4 million who join the labor force as unemployed (that is, they begin actively seeking work) and 2.8 million who join the labor force by accepting a job. These numbers indicate the high fluidity of the U.S. labor market, which has been linked to the exceptional resilience of the American economy during previous downturns.3

The scale of job flows and worker flows also varies widely by industry. For example, job-flow rates are approximately twice as large in leisure and hospitality — the industry in which most food and maintenance workers are employed — than in manufacturing. Worker flow rates are approximately three times larger for leisure and hospitality than for manufacturing.

Adding Occupational Flows to the Picture

In addition to flows among states of the labor market (employment, unemployment and out of the labor force), flows between occupations are also important. Consider, for instance, a worker who loses her job as an administrative assistant and takes a job — out of necessity — as a restaurant server. This transition to such a highly different occupation entails "starting from scratch" in developing occupation-specific human capital. Intuitively, we would expect greater earnings losses from a transition to a dissimilar occupation. This intuition is borne out by the data.4

In fact, research suggests that occupational flows can be exceptionally important in determining future earnings prospects and human capital accumulation. And during recessions, occupational transitions can account for the majority of negative displacement effects. Lisa B. Kahn of the University of Rochester examined the consequences of graduating from college in a "bad" economy in a 2010 article and found a negative effect on occupational attainment as well as on wages.5 Even after the economy improves, these workers are unable to fully shift into better jobs. Similarly, Davis and Till von Wachter of UCLA concluded in a 2011 article that individuals entering the labor market during weak economic conditions face lower earnings for many years.6 While a number of mechanisms play a role in driving these negative effects, the lack of opportunities for new labor market entrants to flow into high-prestige, high-wage occupations during recessions is an important factor.

These articles and other similar research suggest two main conclusions: 1) The American labor market is marked by a high pace of worker flows and occupational transitions, which results in a much lower unemployment rate than other rich countries; and 2) labor market transitions and occupational flows are key determinants of individual outcomes, such as employment stability, wage growth and human capital accumulation, especially during economic downturns.

Labor Market Flows During the Pandemic

The changes in labor markets during the pandemic have presented new challenges to researchers. Over the past year, unemployment rates have been especially turbulent, shooting up between February and April 2020 and then declining suddenly and quickly despite lockdowns and new waves of infections. Professional forecasters have consistently overestimated the unemployment rate in every month since April. In recent research, Ayşegül Şahin and Jin Yan of the University of Texas and Murat Tasci of the Cleveland Fed have shown the value of the flow approach in such conditions, developing a flow-based method for forecasting U.S. unemployment during the COVID-19 recession; their method has more accurately predicted peak unemployment at the onset of the recession and its decline throughout the year.7

Recent research at the Richmond Fed builds on the flow approach and its application to the current recession by addressing three questions:

- From which occupations are workers more likely to exit the labor force, and how likely are they to reenter it?

- How was the occupational makeup of flows into unemployment different in 2020 than during the Great Recession?

- What are the most common transitions for workers formerly employed in the hardest-hit occupations, such as personal care, maintenance and cleaning, and food preparation and service?

The data describing flows of workers across different labor market states (out of labor force, unemployed; and employed) and across the 22 major occupational groups indicate the following answers to these three questions. (Data on the COVID-19 recession incorporate all of the months currently available, namely March 2020 through November 2020. For detailed results, see the data appendix.)

From which occupations are workers more likely to exit the labor force, and how likely are they to reenter it?

The pace of transitions in and out of the labor force is somewhat unusual in the current recession. However, this is not because individuals who are not in the labor force are less likely to reenter it — indeed, the percentage of people who stay out of the labor force in any two consecutive months is very similar to previous periods. In terms of flows into the labor force, the three top occupations are office/administration (0.9 percent), sales (0.7 percent) and food (0.7 percent). These numbers are very similar to the Great Recession.

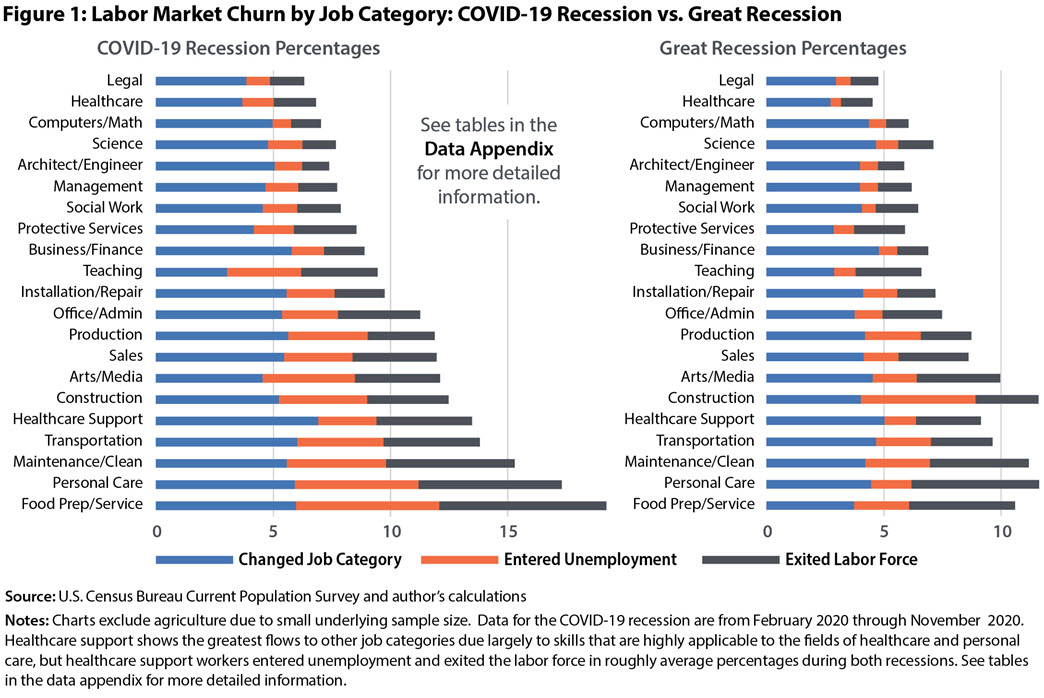

One big difference between the current downturn and the Great Recession is a much higher flow from employment into out of the labor force. (See Figure 1.) This is especially true for food (7.1 percent), personal care (6.1 percent) and maintenance/cleaning (5.5 percent). These job categories primarily employ women.8 In the Great Recession, these occupations also constituted the top "donors" to the out-of-labor-force pool but with much smaller percentages. Food was at 4.5 percent, personal care at 5.4 percent and maintenance/cleaning at 4.2 percent.

These hard-hit occupations experience higher churn rates at all times, both in and out of the labor force, but the pace of worker flows is even higher during the current downturn. In the COVID-19 recession, 3.4 percent of production workers (most of them in manufacturing) became unemployed every month, and 2.9 percent exited the labor force; in the Great Recession, these percentages were 2.4 percent and 2.1 percent, respectively.

How was the occupational makeup of flows into unemployment different in 2020 than during the Great Recession?

While persistent unemployment in the COVID-19 recession is below the level in the Great Recession, temporary (fewer than four weeks) flows into unemployment are higher.9 This highlights the short, but repeated, nature of job loss in the COVID-19 recession: The same categories of workers suffer high job loss month after month. In the current recession, most of the higher flows into unemployment are found in just three occupational groups: food, personal care and maintenance/cleaning (6.1 percent, 5.3 percent and 4.2 percent, respectively). (See Figure 1 above.) This contrasts with the Great Recession both in magnitude (flows are now about twice as high) and occupational concentration. In the Great Recession, the only sector that stood out for its contribution to unemployment was construction.

In any given month from February 2020 through November 2020, the fraction of unemployed workers who remained unemployed for two consecutive months was 50.9 percent. This number is quite a bit lower than in the Great Recession (57.9 percent). Also, flows into unemployment were lower during the Great Recession — 0.9 percent of teachers, 1.5 percent of sales workers, 1.7 percent of personal care workers and 2.3 percent of food workers became unemployed every month. These rates have been 3.2 percent, 2.9 percent, 5.3 percent and 6.1 percent, respectively, in the COVID-19 recession.

In addition to the hardest-hit job categories, it is worth noting that the level of flows into unemployment has exceeded 3 percent for several other sectors, including teaching (3.2 percent), construction (3.8 percent), transportation (3.7 percent) and production (3.4 percent). In the Great Recession, the only sector that exceeded 3 percent was construction. These figures highlight how the high rate of labor market churn during the COVID-19 recession implies both a lower probability of being unemployed for two consecutive months and a higher probability of becoming (newly) unemployed in any given month.

What are the most common transitions for workers formerly employed in the hardest-hit occupations?

Patterns of occupational transitions are mostly based on how well skills from one occupation can transfer to another: Few fry cooks become plastic surgeons and vice versa. However, the COVID-19 recession has seen increased interoccupational mobility. Among the hardest-hit sectors, the percentage of workers continuously employed in those sectors has been considerably lower during the COVID-19 recession than during the Great Recession. In addition, the reemployment rate has been generally lower than during the Great Recession — signaling again that this recession is characterized by more churn in the labor market than other periods. For example, during the Great Recession, 89.4 percent of workers employed in food occupations in any given month would still be employed in that sector in the following month. In 2020, this percentage was 80.8 percent. Similarly, personal care workers have a "staying" rate of 82.5 percent versus 88.4 percent in the Great Recession. Comparable patterns hold for maintenance/cleaning, sales, office/admin and — in a more modest fashion — for all other occupations.

Food, personal care, maintenance/cleaning and, to some extent, office/admin and sales are all occupations whose skills are similar, as evidenced by the fact that workers in these occupations regularly cycle across them. As one would expect, the pace of occupational reallocation slowed down in the Great Recession. But in the COVID-19 recession, the pace of interoccupational churn has exceeded not only the Great Recession rate, but that of the 2016–17 expansion.

Conclusion

The COVID-19 recession has featured an unusually high pace of worker flows between employment and nonemployment and across major occupational categories. Sales, food preparation/service, maintenance/cleaning and personal services are the occupational groups that account for most of the flow both into and out of nonemployment. In addition, workers in these occupations have experienced higher rates of repeated job loss and occupational change during the COVID-19 recession than during the Great Recession.

Given these patterns, it appears desirable for economic policy to pay attention to alleviating income instability from repeated displacements and occupational switches in addition to lack of income caused by long-term unemployment. Higher rates of churn challenge workers in both the short term and the long term. In the short term, workers going in and out of employment see their income fluctuate from month to month — which affects their ability to plan ahead and pay for everyday goods and services. In the medium to long term, frequent nonemployment spells and occupational switches affect a worker’s potential wage growth by interrupting the accumulation of firm-specific and sector-specific human capital. Workers in the hardest-hit occupations have historically seen lower wage-growth rates than, for example, workers in the production sector. Frequent interruptions of their career paths, in terms of both employer and occupational changes, may further depress their prospects for sustained wage growth.

Claudia Macaluso is an economist in the Research Department of the Federal Reserve Bank of Richmond. Many thanks to Alex Wolman for his encouragement and comments on an earlier version of this brief. Rosemary Coskrey provided excellent research assistance.

1

Nonemployment is a broader term than unemployment. It includes workers who are out of work and searching for jobs, those who are out of work and not searching and those who have exited the labor force. The Richmond Fed publishes a monthly measure of nonemployment, the Hornstein-Kudlyak-Lange Non-Employment Index.

2

Steven J. Davis, R. Jason Faberman and John C. Haltiwanger, "The Flow Approach to Labor Markets: New Data Sources and Micro-Macro Links," Journal of Economic Perspectives, Summer 2006, vol. 20, no. 3, pp. 3–26. See also Steven J. Davis, R. Jason Faberman and John C. Haltiwanger, "The Establishment-Level Behavior of Vacancies and Hiring," Quarterly Journal of Economics, May 2013, vol. 128, no. 2, pp. 581–622.

3

Steven J. Davis and John C. Haltiwanger, "Labor Market Fluidity and Economic Performance," National Bureau of Economic Research Working Paper No. 20479, September 2014.

4

Claudia Macaluso, "Skill Remoteness and Post-Layoff Labor Market Outcomes," Manuscript, April 10, 2019.

5

Lisa B. Kahn, "The Long-Term Labor Market Consequences of Graduating from College in a Bad Economy," Labour Economics, April 2010, vol. 17, no. 2, pp. 303–316.

6

Steven J. Davis and Till von Wachter, "Recessions and the Costs of Job Loss," Brookings Papers on Economic Activity, Fall 2011, vol. 42, no. 2, pp. 1–72. See also Hannes Schwandt and Till M. von Wachter, "Socioeconomic Decline and Death: Midlife Impacts of Graduating in a Recession," National Bureau of Economic Research Working Paper No. 26638, January 2020.

7

Ayşegül Şahin, Murat Tasci and Jin Yan, "Unemployment in the Time of COVID-19: A Flow-Based Approach to Real-Time Unemployment Projections," National Bureau of Economic Research Working Paper No. 28445, February 2021.

9

For more on long-term unemployment during and after the Great Recession, see Andreas Hornstein, Thomas A. Lubik and Jessie Romero, "Potential Causes and Implications of the Rise in Long-Term Unemployment," Federal Reserve Bank of Richmond Economic Brief No. 11-09, September 2011.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us