Introducing the Credit Market Sentiment Index

Economic Brief

August 2022, No. 22-33

In a forthcoming paper, we develop a new signal-extraction statistical model to estimate a factor summarizing conditions in U.S. credit markets. The factor provides a real-time gauge of "sentiment" in credit markets, above and beyond that attributable to contemporaneous economic conditions. Fluctuations in the credit market sentiment factor are associated with strong asymmetric and nonlinear effects on economic activity, depending not only on the magnitude and sign of a credit market sentiment shock but also on the current economic conditions.

Understanding the sources and transmission of financial distress in the economy is essential for macroeconomic stabilization policy. For example, policymakers and academics have both pointed to excesses in credit markets — including abnormally low risk premiums, misaligned incentives for risk taking, lax credit standards and excessive borrowing — as the main culprit behind the 2008-09 financial crisis.

Since then, many questions have emerged regarding the role of credit factors in business cycle fluctuations. Our forthcoming paper "Credit Market Sentiment: Estimation and Macroeconomic Implications" addresses two such questions that are especially important for policymakers:

- Do "frothy" conditions in credit markets create risks to future macroeconomic performance?

- If so, how can we measure such froth?

To provide answers, we develop a signal-extraction model of joint nonlinear dynamics that uses an array of economic activity and credit market indicators, with the latter including both price-based and quantity-based indicators. We use the model to estimate a factor that can be updated in real time and that summarizes "sentiment" in U.S. credit markets.

We call it a credit market sentiment factor because the signal is purged of its contemporaneous correlation with economic activity. That is, our factor summarizes credit market conditions beyond what can be attributed to the direct effects of economic activity on credit markets. We document that fluctuations in this factor — which we term credit market sentiment shocks — have economically and statistically significant effects on economic activity. Moreover, these effects are nonlinear and asymmetric, depending not only on the magnitude and sign of the shock but also on the current economic conditions.

Research on Credit Markets

Much of the empirical research that addresses the above questions has focused on the growth in broad credit aggregates or balance-sheet measures of leverage. It has documented that rapid and prolonged increases in credit outstanding presage economic downturns and sharp declines in the stock market.1 Another strand of this literature emphasizes time variation in sentiment on the part of investors in credit markets as an important determinant of the credit cycle and the associated business cycle dynamics.2

This latter approach — which harks back to the narrative accounts of financial crises by the 1977 paper "The Financial Instability Hypothesis: An Interpretation of Keynes and an Alternative to 'Standard' Theory" and the 1978 book Manias, Panics and Crashes — identifies periods of frothy credit market conditions as those in which the objective expected returns to bearing credit risk are driven too low because credit is being priced too aggressively. The key takeaway from these studies is that periods in which credit risk was being aggressively priced are predictably followed by a widening of credit spreads. The timing of this widening reliably precedes the downturn in economic activity.

An important behavioral perspective linking the pricing of credit risk to economic outcomes is related to the way investors in credit markets update their beliefs in light of incoming data. In particular, investors may overreact to recent news and thus overweight future outcomes that have now become a little more likely. For example, investors may become complacent about default risk after a few years of economic expansion, which can lead to:

- Compression in credit spreads

- A loosening of bank lending standards and terms

- A surge in the issuance of credit to risky borrowers

In such an environment, the arrival of unfavorable economic news — at least, unfavorable by the recent overly optimistic standards — can lead investors to revise disproportionately their assessment of default risk, precipitating a pullback in the supply of credit that triggers an economic downturn. This reasoning implies that investor psychology can itself be a cause of volatility in credit and investment, even in the absence of significant changes in economic fundamentals. Several papers formulate psychological models of investor confidence, in which investors' overly extrapolative expectations can lead to concordant credit and business cycles, even without changes in economic fundamentals.3

Understanding the role of credit market sentiment for economic activity also matters for policy. The 2013 paper "Issuer Quality and Corporate Bond Returns" emphasizes the role of investor risk appetite and beliefs in driving credit cycles. It argues that: "[A] major challenge for any countercyclical credit policy is identifying the existence of a sentiment driven credit boom in the first place."

Relatedly, the 2013 speech "Overheating in Credit Markets: Origins, Measurement and Policy Responses" argues that policymakers should pay close attention to the effects of non-fundamental factors on the economy. It notes that "[O]ne of the most difficult jobs that central banks face is in dealing with episodes of credit market overheating."

Estimating Credit Market Sentiment

Gauging sentiment in credit markets is not easy. While brisk credit growth, loose lending standards, rising leverage and narrow risk spreads are all indicative of accommodative or even frothy credit market conditions, they also partly reflect strong borrower fundamentals and robust economic growth. The fact that credit market conditions are influenced importantly by economic fundamentals implies a need for a methodology that accounts for the effect of current economic conditions on credit markets. Moreover, to the extent that the relationship between credit market sentiment and economic conditions may differ between normal and crisis periods, the methodology should be able to accommodate possible nonlinear dynamics.

Several credit market indicators can — and indeed have been — used as proxies for credit market sentiment. Individually, however, each indicator provides only a partial approximation that contains information about sentiment embedded in a specific indicator or credit market segment.

Moreover, any credit market indicator contains information about current economic conditions. Individual indicators can also be noisy and often difficult to reconcile with the readings of other variables, making it difficult to arrive at a comprehensive assessment of how "frothy" or "tight" credit market conditions are.

To identify the role of sentiment-driven shocks in business cycle fluctuations, we need a measure that captures the underlying common signal from a variety of credit market indicators. This measure also needs to be purged of its contemporaneous correlation with real economic activity.

With this in mind, we develop a statistical model that efficiently incorporates information from key economic activity and credit market indicators to produce a credit market sentiment factor with high information content about the potential fragility of U.S. economy. The construction of this factor entails extracting information about credit market conditions from multiple credit market indicators, both price-based and quantity-based.

We consider price-based indicators such as credit spreads and associated risk premiums based on the 2012 paper "Credit Spreads and Business Cycle Fluctuations" and related studies, which point to the information content of these indicators for future economic activity. Similarly, we also use quantity-based measures such as the growth of bank balance sheets, following the 2012 paper "Credit Booms Gone Bust: Monetary Policy, Leverage Cycles and Financial Crises, 1870-2008" and others that show that rapid and sustained credit growth anticipates economic downturns.4

By considering the interaction between credit quantities and prices, our framework is consistent with the 2021 paper "Can Policy Tame the Credit Cycle?," which emphasizes that the interplay between leverage and mispricing is central to the 1977 paper "The Financial Instability Hypothesis: An Interpretation of Keynes and an Alternative to 'Standard' Theory" and in understanding the role of credit sentiment in the credit cycle and economic activity.

Our model also incorporates a range of real activity indicators, and when we extract the signal about credit market conditions, we consider the effect of real activity — as summarized by the economic activity factor — on credit market variables. The reason is that we want our credit signal to capture only information from credit markets that is not attributable to current economic conditions.

Credit market variables also exhibit a markedly nonlinear relationship with economic activity.5 Therefore, we consider a nonlinear framework that allows for the economy to move between "normal" (expansionary) and "adverse" (contractionary) states. The two states are characterized by the joint behavior of credit market sentiment and economic activity factors.6

Our model delivers three key indicators:

- The economic activity factor, which summarizes current economic conditions

- The credit market sentiment factor, a measure of how accommodative or restrictive are credit conditions in the economy beyond what can be explained by the economic activity factor

- The probability that the economy is currently in an adverse state, determined by the joint dynamics of the credit market sentiment and economic activity factors

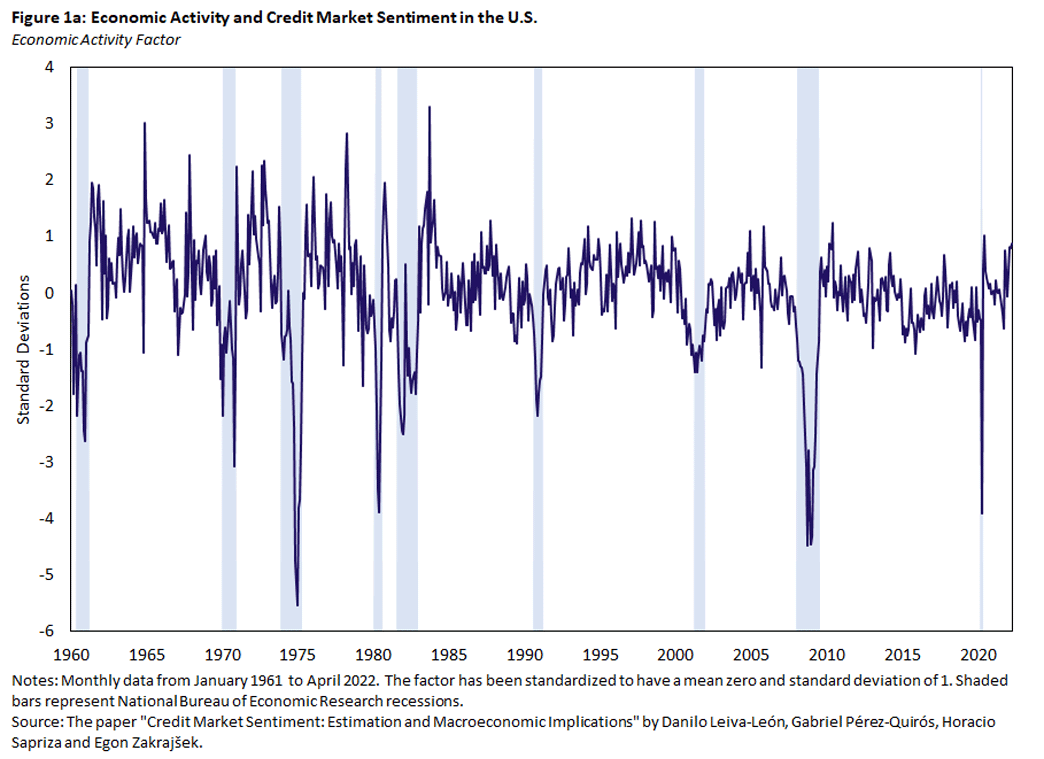

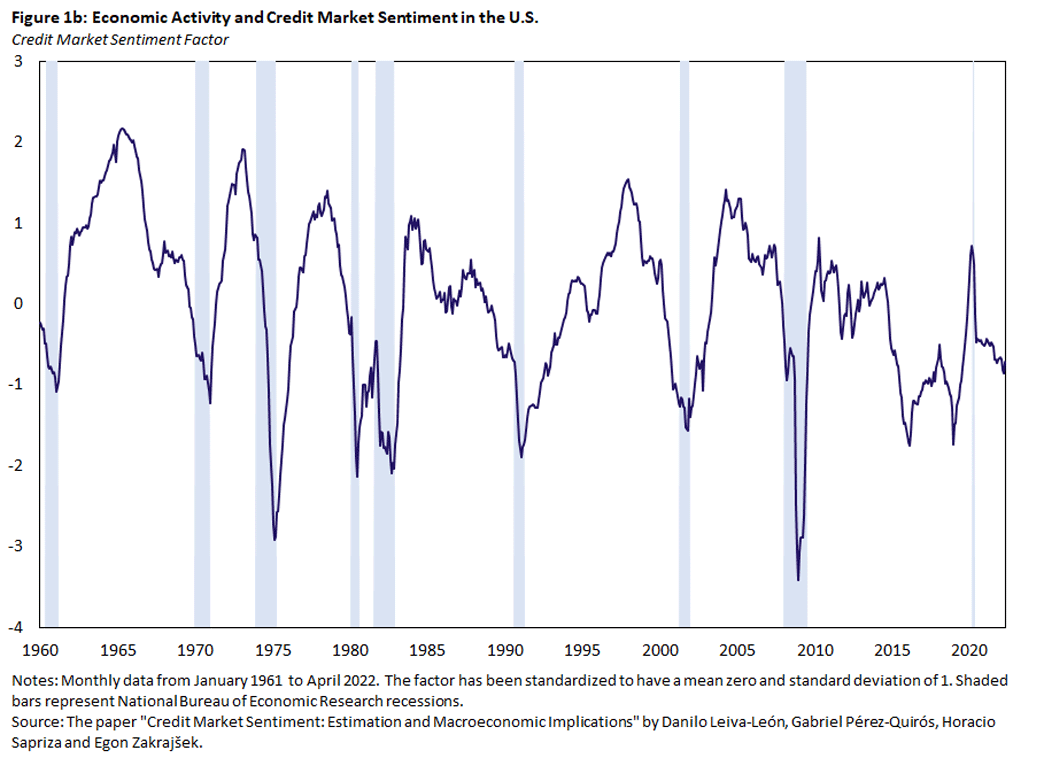

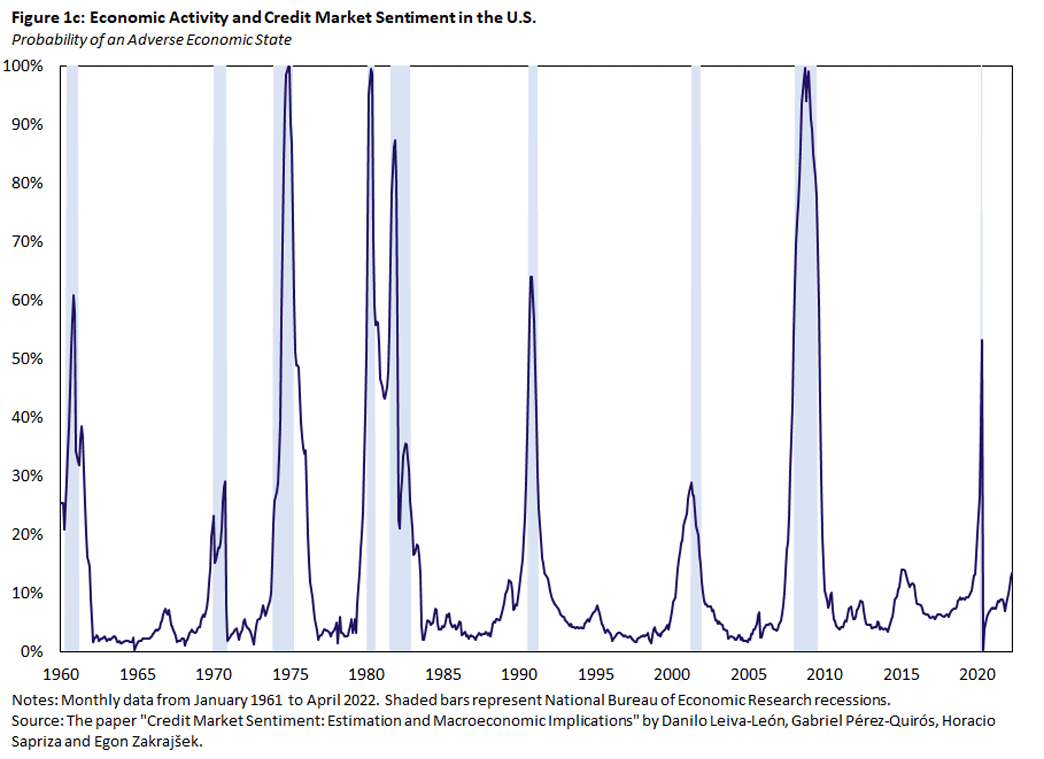

Figure 1 shows these three indicators.

As shown in Figure 1a, the economic activity factor captures well the declines in economic activity during recessions, as well as the quick rebound from the recent COVID crisis. Figure 1b shows the credit sentiment factor, which exhibits much wider swings than the economic activity factor. The low-frequency movements in the credit sentiment factor are consistent with the evidence presented by the 2012 paper "Characterizing the Financial Cycle: Don't Lose Sight of the Medium Term" and represent comovements across an array of credit market indicators, purged of the contemporaneous comovements that these indicators have with the economic activity factor.

Note that our credit market sentiment factor clearly identifies the extended period of credit market overheating leading up to the 2008-09 financial crisis and associated recession. It also picks up a marked and sudden deterioration in credit market sentiment in the summer of 2015, when concerns about global growth prospects (centered around China) sparked a widespread repricing of risky assets and a sharp increase in financial market volatility. In fact, according to our estimates, the ensuing gloom that engulfed credit markets was quite persistent and started to lift only in 2019.

Lastly, Figure 1c shows the estimated time series of probabilities that U.S. economy is in an adverse economic state. These probabilities accord well with recessions, an indication that our model is able to distinguish between expansionary and contractionary periods of economic activity, which (as is well known) differ notably in their macroeconomic dynamics. In our framework, this distinction is informed by the dynamic interaction of the economic activity and credit sentiment factors, an idea consistent with the extensive empirical evidence that recessions accompanied by disruptions in credit markets tend to be longer and deeper than other recessions.7

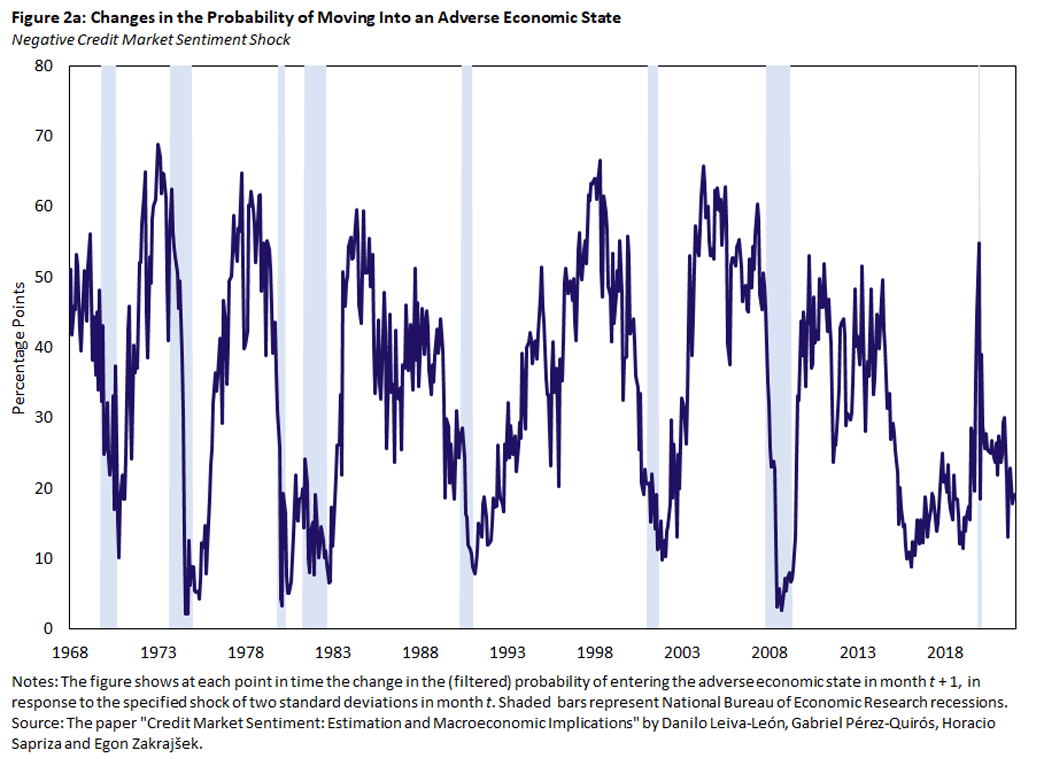

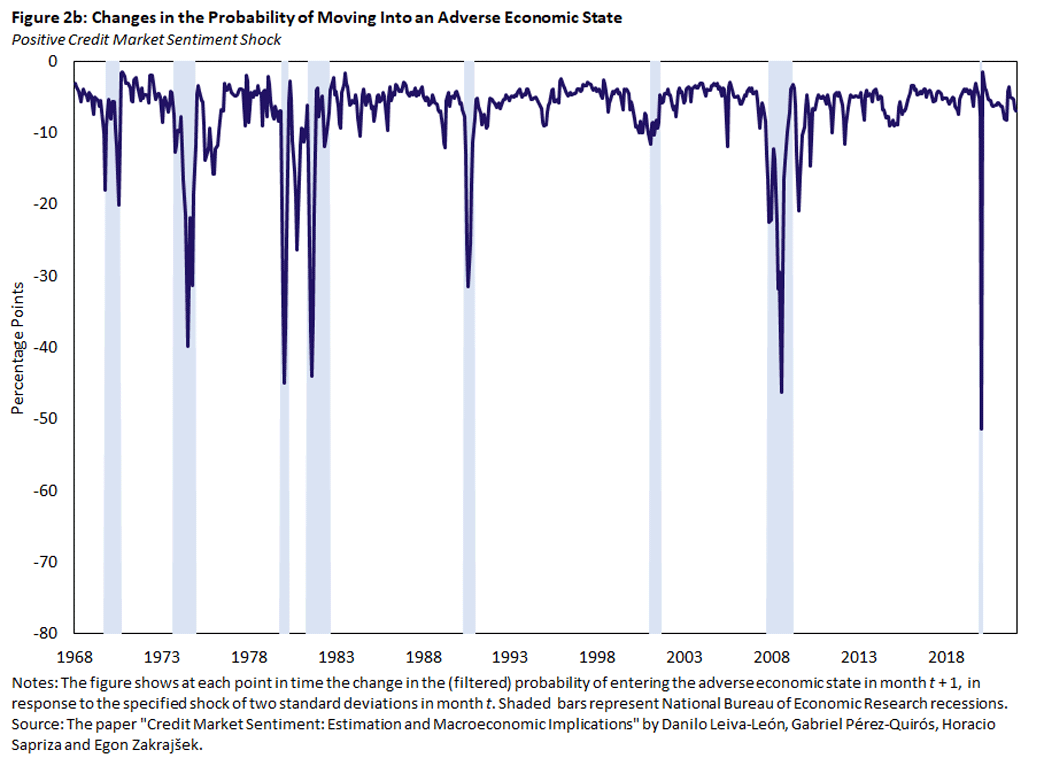

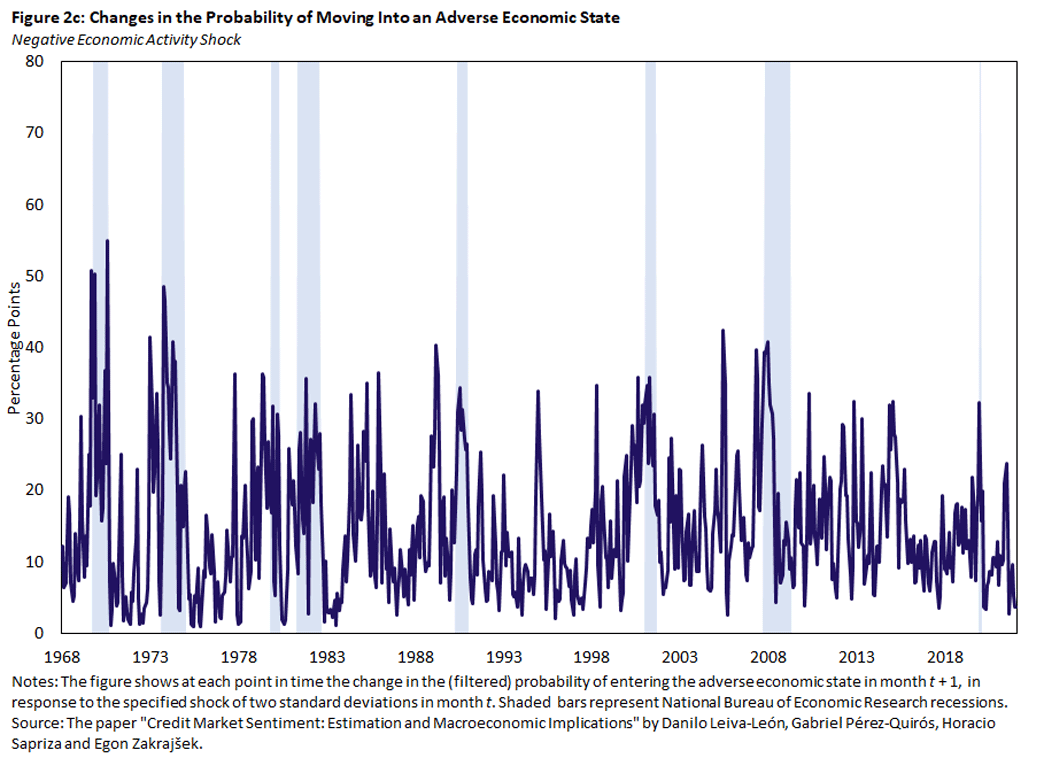

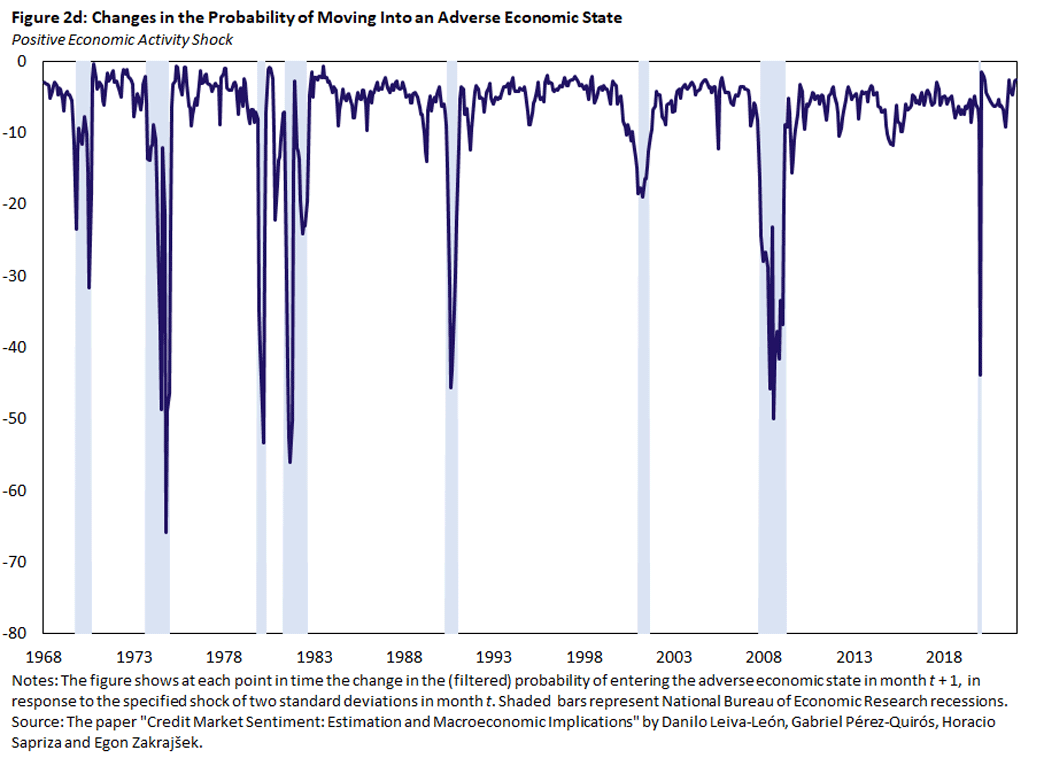

Figure 2 shows another output of the model, which can be used to gauge the vulnerability of U.S. economy to sudden changes in credit market sentiment and real shocks and which also illustrates the inherent asymmetries and nonlinearities of our framework.

In particular, Figures 2a and 2b show the model-implied changes in the probability of being in an adverse economic state in month t + 1, conditional on a negative (Figure 2a) or positive (Figure 2b) credit market sentiment shock hitting the economy in month t. Figures 2c and 2d show the corresponding changes in the same probabilities in response to real economic shocks.8

According to Figure 2a, negative credit market sentiment shocks in normal times significantly increase the probability that the economy will subsequently find itself in an adverse state. Moreover, this sensitivity varies notably over the course of a business cycle, generally peaking in the late stages of an economic expansion. This pattern is consistent with a gradual buildup of financial excesses during economic booms that predictably end in a credit bust accompanied by a severe economic downturn. By contrast, the same-sized shock during a recession has very little effect on these probabilities because the economy is already in an adverse state. As shown in Figure 2b, the impact of positive credit market sentiment shocks is exactly the opposite: In adverse economic states, an improvement in credit market sentiment significantly lowers the likelihood that the economy will remain in that state during the following month.

Figure 2c shows the model-implied changes in the probability of moving from a normal to an adverse economic state in month t + 1 in response to a negative shock in real activity in month t. Not surprisingly, negative real activity shocks in normal times also tend to increase the likelihood that economy will enter an adverse state. However, compared with adverse credit market sentiment shocks, their effects on these probabilities are much smaller on average and do not exhibit a clear cyclical pattern. As shown in Figure 2d, positive shocks to real economic activity during recessions, as expected, significantly reduce the probability of economy remaining in an adverse state. In fact, their impact during recessions is comparable to the same-sized positive shocks in credit market sentiment.

Summary

All told, our results indicate that fluctuations in credit market sentiment — a comovement in credit market indicators above and beyond the comovement induced by the contemporaneous economic conditions — have economically and statistically significant effects on real economic outcomes. The effects of credit market sentiment shocks on economic activity are asymmetric and involve nonlinear dynamics, reflecting the slow buildup of financial imbalances during economic expansions. Once the economy is in such a vulnerable state, a negative sentiment shock can easily tip the economy into an adverse state, where the interaction of falling asset prices, high debt burdens and balance-sheet repair depresses growth for a protracted period.

Danilo Leiva-León and Gabriel Pérez-Quirós are senior economists at the Banco de España. Horacio Sapriza is a senior economist and policy advisor in the Research Department at the Federal Reserve Bank of Richmond. Francisco Vazquez-Grande is a principal economist in the Macro Finance Analysis section of the Monetary Affairs Division at the Federal Reserve Board of Governors. Egon Zakrajšek is a senior adviser at the Bank for International Settlements.

1

See, for example, the 2009 paper "The Aftermath of Financial Crises," the 2011 paper "Financial Crises, Credit Booms and External Imbalances: 140 Years of Lessons," the 2012 papers "Credit Booms and Lending Standards: Evidence From the Subprime Mortgage Market" and "Credit Booms Gone Bust: Monetary Policy, Leverage Cycles and Financial Crises, 1870-2008," the 2013 paper "When Credit Bites Back," the 2015 paper "Leveraged Bubbles," the 2016 paper "The Great Mortgaging: Housing Finance, Crises and Business Cycles," and the 2017 papers "Credit Expansion and Neglected Crash Risk" and "Household Debt and Business Cycles Worldwide."

2

See, for example, the 2012 paper "Credit Spreads and Business Cycle Fluctuations," the 2013 paper "Issuer Quality and Corporate Bond Returns," the 2017 working paper "How Credit Cycles Across a Financial Crisis," the 2017 paper "Credit-Market Sentiment and the Business Cycle," the 2018 working paper "Lending Standards and Output Growth" and the 2022 paper "Predictable Financial Crises."

3

Examples of papers include the 1998 paper "A Model of Investor Sentiment," the 2010 paper "The Gambler's and Hot-Hand Fallacies: Theory and Applications," the 2017 paper "Diagnostic Expectations and Credit Cycles" and the 2019 paper "Reflexivity in Credit Markets." For studies focused on the role of consumer sentiment in economic fluctuations, see, for instance, the 2022 paper "Sentimental Business Cycles."

4

Specifically, the quantity-based credit market indicators include the monthly growth of real bank credit and high-yield corporate bond issuance, expressed as a share of total corporate bond issuance. The price-based indicators include the Moody's Baa-Aaa corporate bond credit spread, the excess bond premium and the at-issuance spread on B-rated leveraged syndicated loans. The set of economic activity indicators is comprised of the monthly growth rates of (nonfarm) payroll employment, industrial production, real manufacturing and trade sales, and real total personal income (less transfer payments).

5

For example, see the 2013 paper "Intermediary Asset Pricing" and the 2017 paper "How Credit Cycles Across a Financial Crisis."

6

For example, see the 2012 paper "How Do Business and Financial Cycles Interact?"

7

Formally, our statistical signal-extraction model is a dynamic factor model, in which the credit market sentiment and economic activity factors follow a two-state Markov-switching vector autoregression. To identify credit market sentiment shocks, we impose restrictions on the system of measurement equations, whereby the credit market sentiment factor has no contemporaneous effect on the economic activity indicators, but the economic activity factor can have a contemporaneous effect on all the variables in the system.

8

The size of both shocks is always two standard deviations.

To cite this Economic Brief, please use the following format: Leiva-León, Danilo; Pérez-Quirós, Gabriel; Sapriza, Horacio; Vazquez-Grande, Francisco; and Zakrajšek, Egon. (August 2022) "Introducing the Credit Market Sentiment Index." Federal Reserve Bank of Richmond Economic Brief, No. 22-33.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

The views expressed in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Banco de España, Bank for International Settlements, the Federal Reserve Board of Governors, or the Federal Reserve Bank of Richmond.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us