What Survey Measures of Inflation Expectations Tell Us

Economic Brief

January 2023, No. 23-03

Throughout this period of high inflation, people have wondered when inflation will return to the FOMC's longer-run target of 2 percent. Many models and surveys on inflation expectations exist to help answer this question. In this Economic Brief, we explore the accuracy of these measures of inflation expectations and what information can be obtained from them. While we find these popular sources of inflation are historically inaccurate, they can still gather valuable information, such as people's confidence in the ability of the Fed to get inflation back to target.

For the past year and a half, high inflation has been on many people's minds. People look to popular sources of data on inflation expectations — such as the University of Michigan's Surveys of Consumers or the Philadelphia Fed's ATSIX model — for a sense of how much longer this uncharacteristically high inflation will last. This raises the question: How accurate are measures of inflation expectations? In this article, we examine the historical accuracy of inflation expectation measures, explore what goes into these measures and discuss what they tell us.

We look at four popular surveys on inflation expectations across different time horizons and compare their expectations to the corresponding realized rate of inflation, using either CPI or PCE inflation. While CPI is the most popular measure of inflation, PCE is the Fed's preferred measure of inflation. Thus, our preference is to compare inflation expectation measures against PCE, unless the measure specifically gauges CPI inflation.

The Philadelphia Fed's ATSIX Model

The first model we examine is the Philadelphia Fed's Aruoba Term Structure of Inflation Expectations (ATSIX). This model is formed by combining surveys from professional economists and forecasters — such as the Blue Chip Economic Indicators and the Survey of Professional Forecasters — using a factor model for optimal results. The Philadelphia Fed uses the methodology described in the 2016 working paper "Term Structures of Inflation Expectations and Real Interest Rates (PDF)" to generate this model for several time horizons.

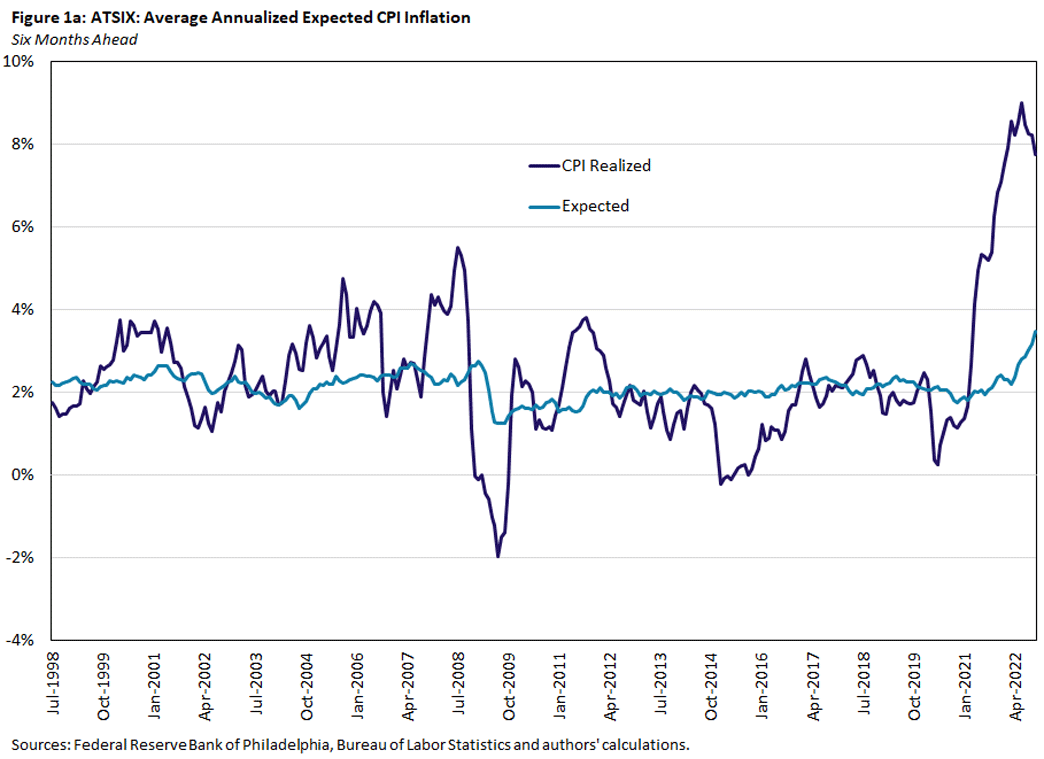

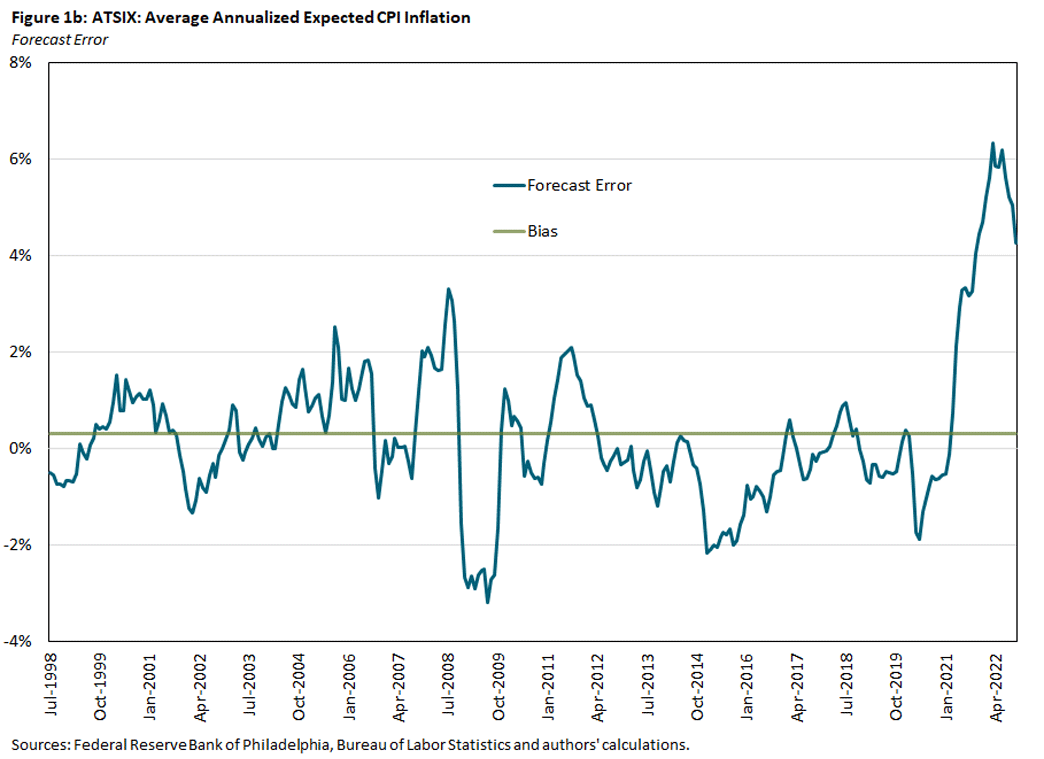

Figures 1a and 1b below examine the accuracy of the Philadelphia Fed's ATSIX six-month model. Figure 1a displays the expected inflation rate compared to realized CPI inflation. To match expected to realized inflation, we shift the inflation expectation at the time of the forecast up six months and compare it with actual inflation at that time.1 Figure 1b displays the forecast error and bias — or average difference between realized and expected inflation — across the period.

This ATSIX model of inflation expectations is the most accurate in our sample, with the smallest absolute bias of 0.3. However, it should be noted that, of the four survey measures we consider, the ATSIX model is the only measure that contains both survey-based and professional forecaster-based measures. We also notice a pattern of inflation expectations reflecting the rate of inflation at the time of the prediction. While not as pronounced in this model, this lag of inflation expectations will become clearer in the figures below.

University of Michigan and New York Fed Inflation Expectation Measures

Next, we look at a few consumer-based surveys of expected inflation coming from the University of Michigan and the Federal Reserve Bank of New York. Both surveys are meant to represent the sentiment of American households.

The University of Michigan Expected Inflation Rate for one year ahead is part of the larger Surveys of Consumers conducted by the university. Each month, at least 600 interviews are conducted, with each person asked:

- During the next 12 months, do you think that prices in general will go up, or go down, or stay where they are now?

- By about what percent do you expect prices to go (up/down), on the average, during the next 12 months?

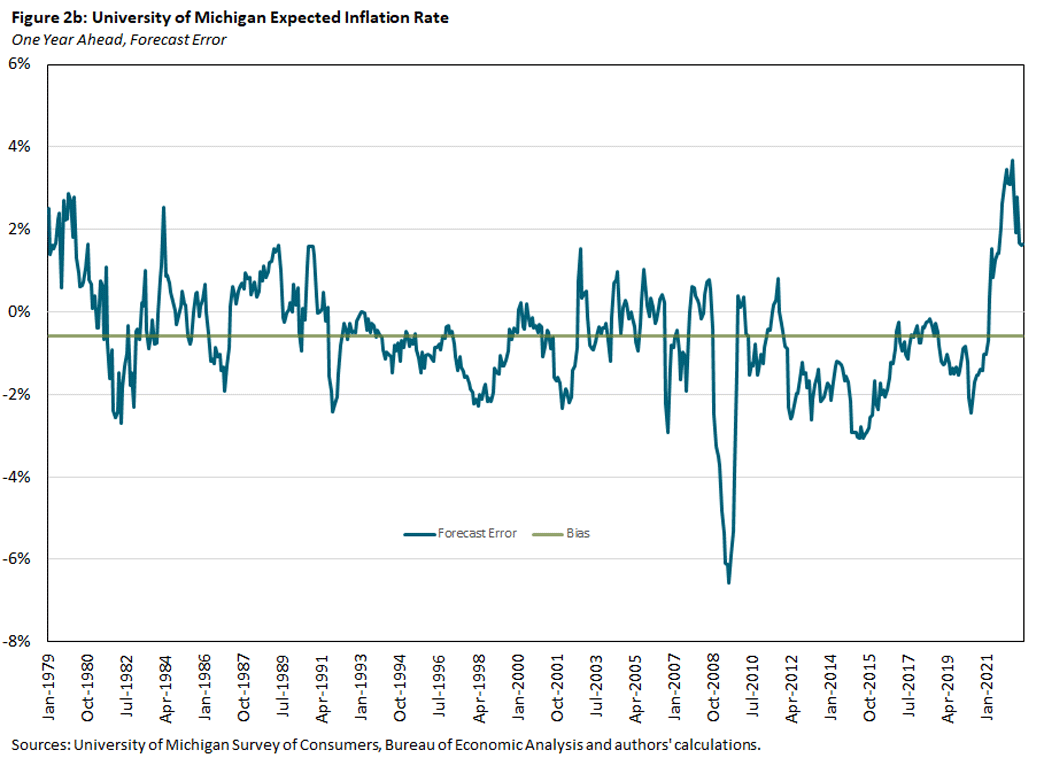

Figures 2a and 2b below show the performance of the University of Michigan rate against realized PCE inflation. As can be seen in the figures, consumer-based surveys tend to overestimate future inflation.

While not shown in any figures, the New York Fed's Median Point Prediction Inflation Rate is conducted like the University of Michigan's survey and produces similar results. As part of the Survey of Consumer Expectations, respondents are asked for a point prediction of what they think the rate of inflation over the next 12 months will be, rather than the percent of change in prices. This survey is distributed to a rotating panel of approximately 1,300 household heads designed to be nationally representative.

Both the University of Michigan and New York Fed's inflation expectations' bias are negative, supporting the notion of historical overpredictions. This bias is driven in part by inflation rates below the Fed's 2 percent target for most of the period after 2000 and inflation expectations never catching up to those lower rates. Put another way, inflation expectation errors are persistent.

Furthermore, inflation expectations tend to be lagged and backward-looking. That is, the rate of expected future inflation seems to be dependent on the rate of current inflation. This relationship is strong in periods of high inflation (as seen in recent months) as well as the late 1970s but is somewhat less evident in times of low inflation.

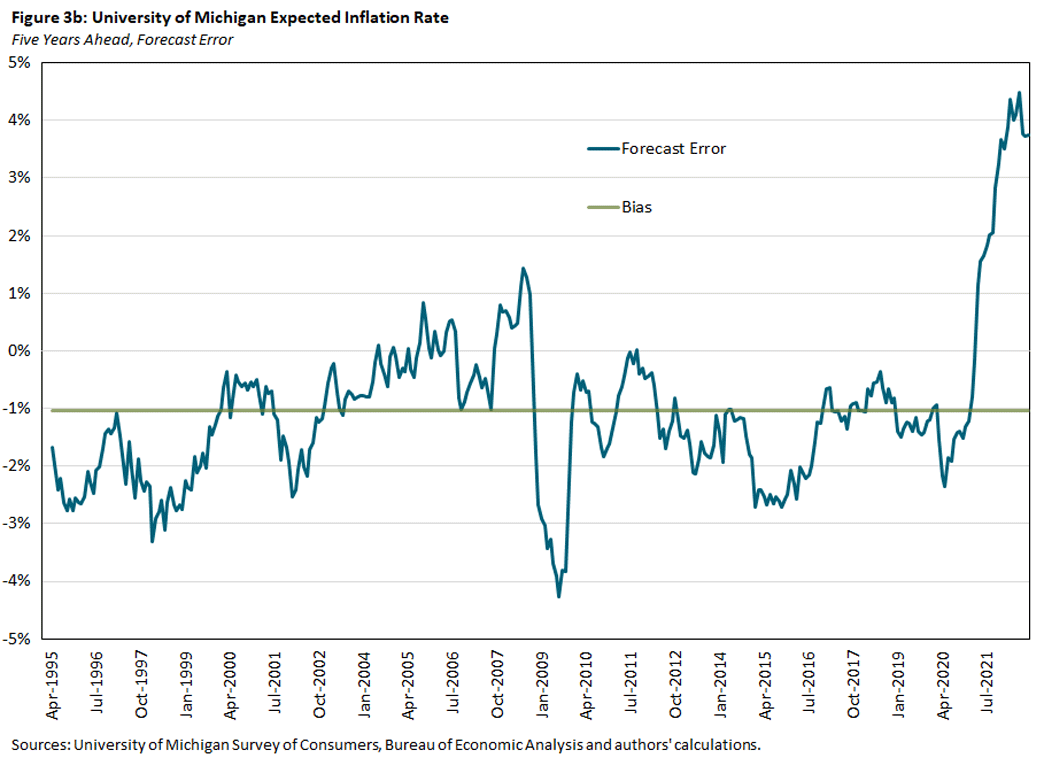

University of Michigan's Inflation Expectations Over Five Years

In addition to inflation one year ahead, the University of Michigan's Surveys of Consumers also investigates expected inflation for the next five years. Like the one-year-ahead questions, respondents are asked:

- Do you think prices will be higher, about the same, or lower, 5 to 10 years from now?

- By about what percent per year do you expect prices to go (up/down) on the average, during the next 5 to 10 years?

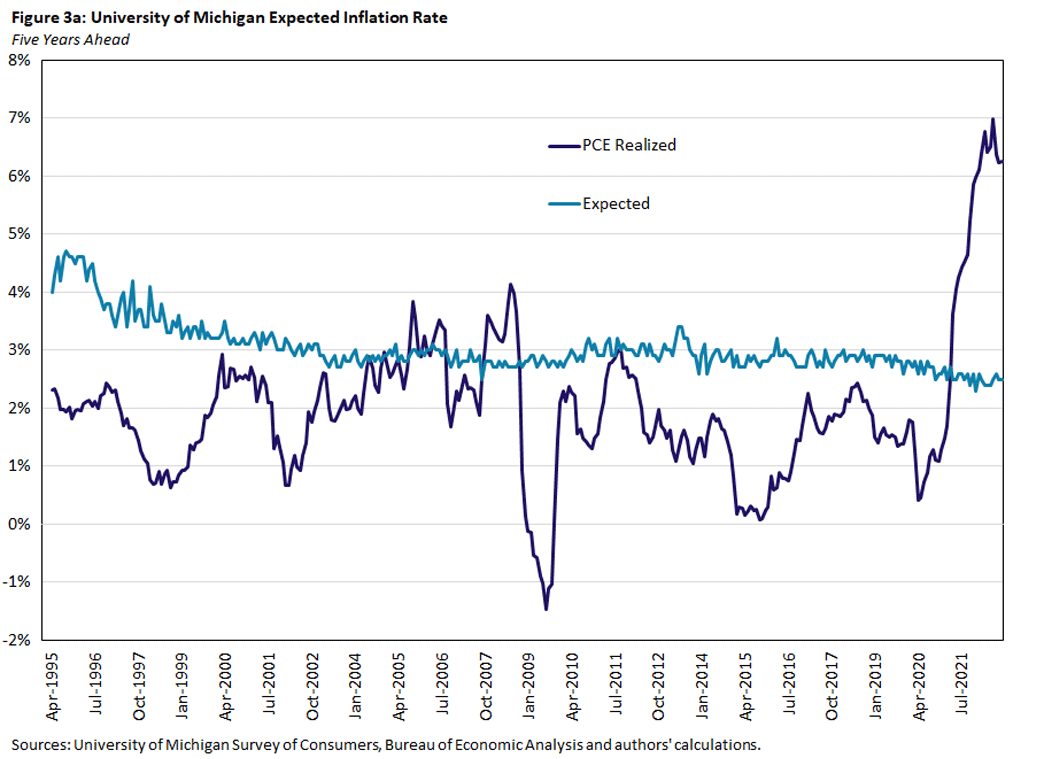

Figures 3a and 3b below show that longer-term inflation expectations have remained anchored around the Fed's long-term goal of 2 percent.

Since the early 2000s, the University of Michigan's five-year inflation expectations have remained within a 1.5 percentage point range, never falling below 2 percent or rising above 3.5 percent. Therefore, any variance in the forecast error in Figure 3b above is essentially a result of changes in inflation, rather than a change in expectations. On one level, this suggests that this longer-term measure poorly predicts future inflation. Another interpretation, though, is that it reflects substantial creditability in the Fed's inflation target despite persistent misses.

While anchored inflation expectations during this period of high inflation can be encouraging, it is also important to recognize that these expectations have been anchored for over 20 years. If these expectations were to suddenly increase, it might indicate a substantive loss of faith in the Fed and be a cause for concern. Put simply, it may mean little if these expectations do not move but may mean a lot if they do.

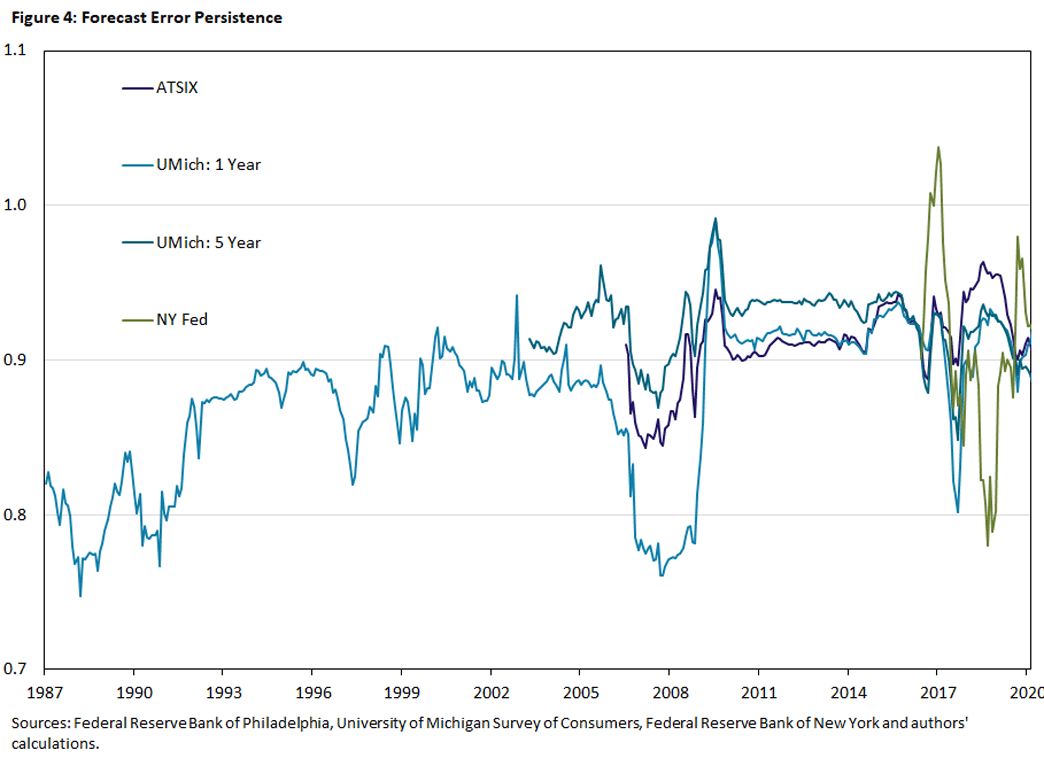

Persistence of Inflation Forecast Errors

As hinted above, another way to assess inflation expectations is to examine the persistence of these expectation errors, or the approximate percentage of a past expectation error carried over to the next period's expectation error. The method and calculations below directly follow the previous work of the 2022 article "How Persistent is Inflation?," which gives a more in-depth look into the persistence of inflation. Figure 4 below displays the forecast error persistence for our four survey-based sources of inflation expectations.

Figure 4 above tells us that each of these forecast errors are highly persistent. A persistence of 0.9 implies that 90 percent of a past forecast error transfers over to the next period. With such large levels of persistence, it can take a long time for a single period's error to fully disappear.

This is potentially worrisome in times of extreme unexpected inflation such as the present period, especially as the degree of persistence appears uniformly high irrespective of the time period under consideration. As we have seen, none of these measures of inflation expectations foresaw the recent rapid climb in inflation, generating above average forecast errors. Combined with high levels of persistence, these errors may be difficult to reverse.

Conclusion

We have seen that these survey measures of inflation expectations are not always reliable predictors of inflation. For example, excluding the post-COVID period of high inflation, the University of Michigan Expected Inflation Rate for one year ahead has overpredicted future inflation every month since 2012.

However, that is not to say that these measures do not accurately reflect the views of households being surveyed. Moreover, this persistent overprediction prior to 2020 has a silver lining. Recently, we have seen elevated levels of inflation expectation in surveys. For example, the November 2022 reading of the University of Michigan one-year-ahead survey measure was 4.9 percent. Given the survey's previous bias, especially looking at the decade preceding the pandemic, it is possible the survey is still overpredicting inflation one year from now.

Regardless, it will be important in the coming months to think carefully about what each of these surveys tells us about the state of the economy, considering their historical tendencies in high and low inflationary periods.

Erin Henry and Conner Mulloy are research associates and Pierre-Daniel Sarte is a senior advisor in the Research Department at the Federal Reserve Bank of Richmond.

1

This process is then repeated in a similar manner for each of our observed surveys and their corresponding time horizon.

To cite this Economic Brief, please use the following format: Henry, Erin; Mulloy, Conner; and Sarte, Pierre-Daniel. (January 2023) "What Survey Measures of Inflation Expectations Tell Us." Federal Reserve Bank of Richmond Economic Brief, No. 23-03.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us