How Well Do Firms Retain Customers After Price Increases?

Economic Brief

May 2023, No. 23-16

Economists at the Federal Reserve Bank of Richmond and the Einaudi Institute for Economics and Finance developed a model that studies the optimal price setting of a firm. Using microdata from the U.S. retail industry, we document that customer turnover responds to price changes. Therefore, to keep customers, firms do not completely pass productivity shocks through to their prices. The price pass-through is heterogeneous across firms, with the most productive firms passing through more.

This article explores the trade-off that firms face when pricing their products in settings with "sticky" customer bases. Customer bases are sticky if customers face research costs when finding new suppliers and opting out from their previous suppliers. My (Nicholas') paper "Price Dynamics with Customer Markets" — co-authored with Luigi Paciello and Andrea Pozzi — investigates this trade-off and provides a model that matches two important features: price setting and demand dynamics.

The customer base of a firm is the set of individuals who buy from that firm at a particular point in time. The relationship between consumers and suppliers is subject to some degree of stickiness because it's costly for consumers to search for new suppliers. As a result, price changes can have a long-lasting impact on a firm, affecting both its current and future value. Thus, firms absorb a portion of cost shocks to retain customers, and given that firms have varying demands and levels of productivity, the price pass-through after a shock will vary across firms.

Data

To examine customer retention following price increases, we use cashier register records of households that hold a loyalty card for a major U.S. supermarket chain. The data encompass all shopping trips made by each household to the chain from June 2004 to June 2006. We consider households as having exited the customer base when they have not made any purchases at the chain for at least eight consecutive weeks.

These data were then merged with detailed information on prices posted by the retailer, which helps to construct the price of the typical bundle bought by each customer. Variation of this bundle's price is what affects each customer's exit decision.

Model

In the model, the economy is populated by a set of firms producing homogenous goods and a set of customers who consume them. All customers start in the customer base of the firm they bought from in the previous period. Since the price of homogenous goods varies, customers are then incentivized to explore other options. In every period, they draw a new search cost to observe the state of another randomly selected firm, compare it to the price of their old supplier and decide where to buy from. Customers then decide the quantity of the goods they will purchase.

What the Model Tells Us

Productivity plays a key role in this dynamic between price and customer demand. If all firms had similar productivity levels, each firm's customer base would remain constant in equilibrium.

However, more productive firms are better positioned to offer lower prices, leading to greater customer loyalty. Although pricing decisions for firms with high productivity are unaffected by customer retention concerns, the remaining firms face competition for customers, resulting in incomplete price pass-through of cost shocks. As more productive firms charge lower prices, they attract more customers and grow faster. On the other hand, less productive firms are net losers of customers, despite charging lower markups.

The model shows that a price increase significantly raises the probability that customers exit the firm. This implies that the customer base is elastic to prices: A 1 percent price change generally results in increasing the yearly customer turnover rate from 14 percent to 21 percent.

Figure 1a displays the optimal price as a function of productivity. The relationship is flat for intermediate levels of productivity but becomes steep at low and high levels. This highlights two important implications of the model:

- The pass-through is incomplete, with firms passing through an average of 26 percent of cost shocks to prices.

- The pass-through depends on productivity: high for firms on the right and left tails of the productivity distribution and low for firms with average productivity.

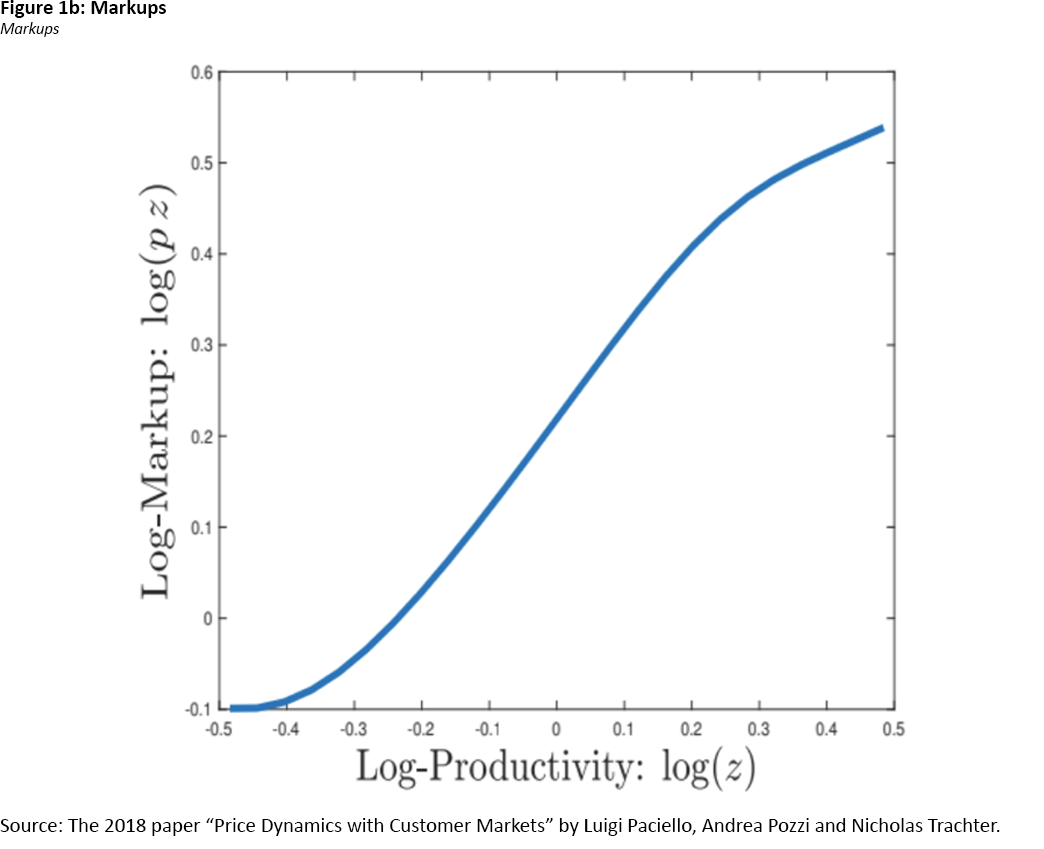

Figure 1b shows that optimal markup positively correlates with firm productivity. More productive firms that charge consistently lower prices are more appealing to customers and face lower demand elasticity. As a result, they charge higher markups.

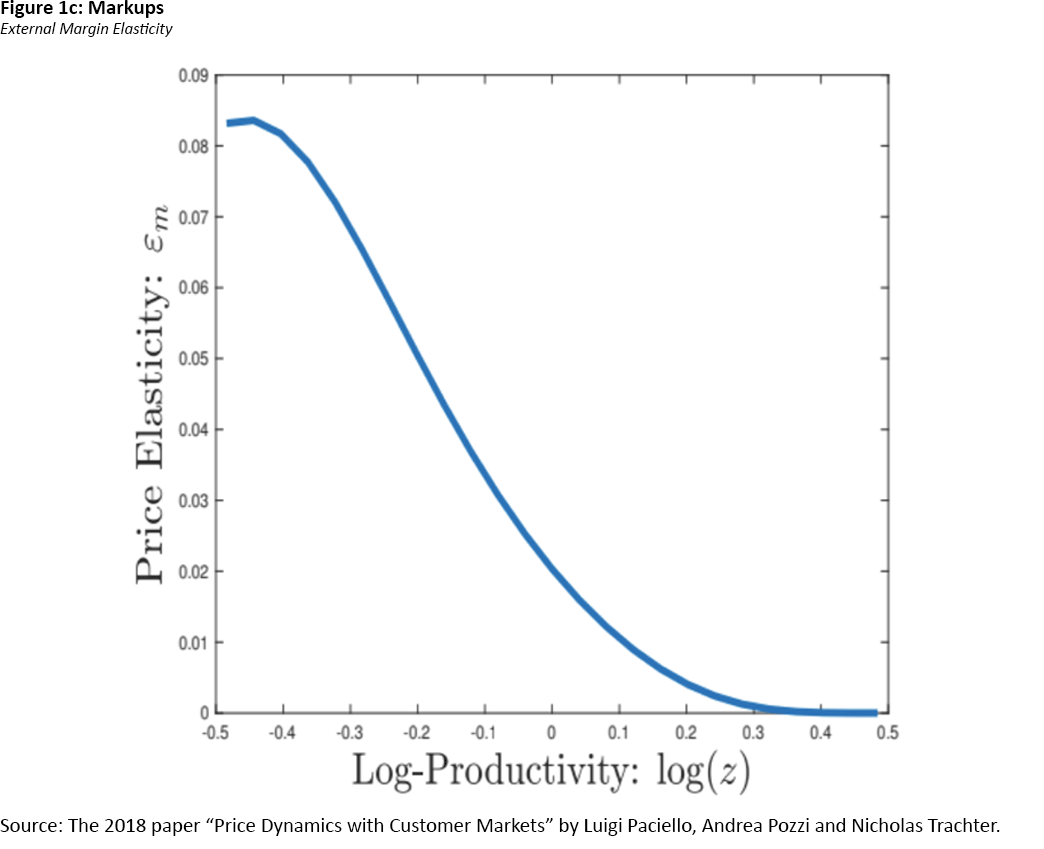

Figure 1c offers more insight into heterogeneity in pass-through. The figure shows that demand elasticity decreases as productivity increases, indicating that customers are less likely to switch to other suppliers when facing increased prices from more productive firms. In other words, the most productive firms have a lower risk of losing customers, as they offer high expected value to their customers relative to the average firms.

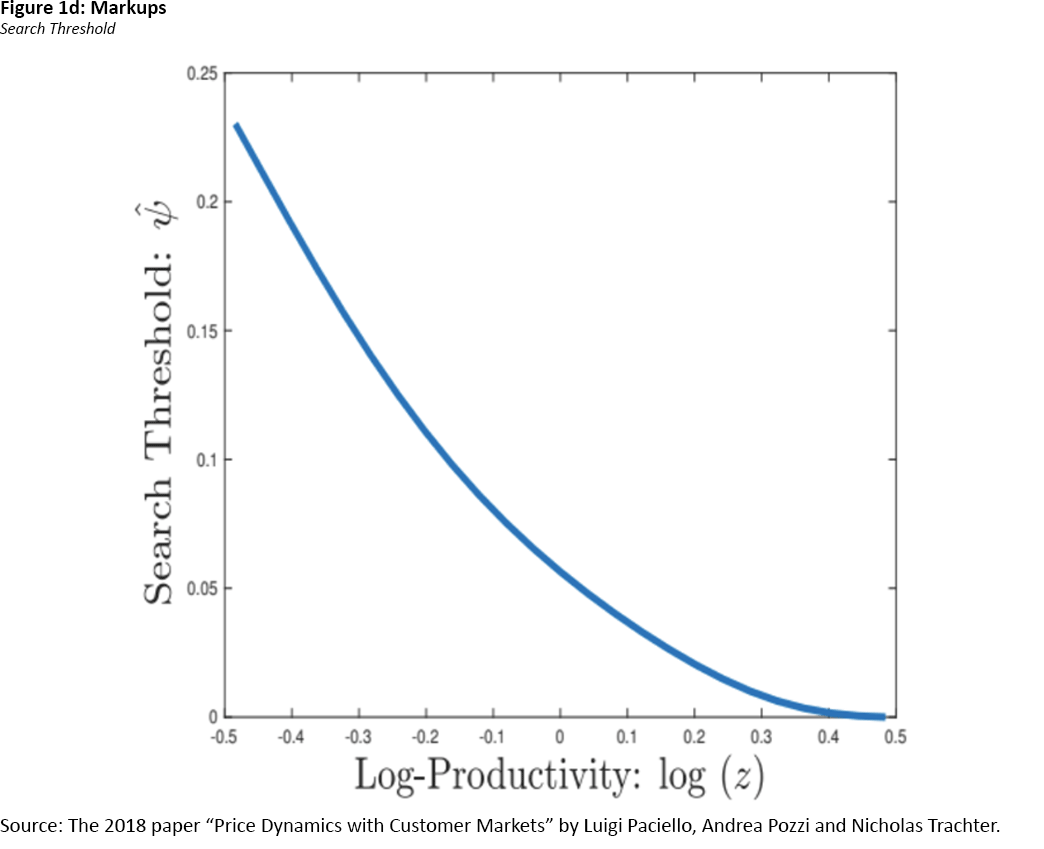

Therefore, among more productive firms, the threshold to search is lower, as seen in Figure 1d. This means a small fraction of a firm's customers searches and an even smaller fraction exits the customer base. Only those customers with small search costs will search, and among those a small fraction will find a better match.

Therefore, firms with higher productivity can afford to almost fully pass costs through, and they enjoy high markups because they are less likely to lose their customers. On the other hand, as productivity decreases, the probability that customers draw a better match and switch to another supplier increases. Firms with average productivity will offset productivity shocks with reductions in markups, which can explain the flatness in the middle of Figure 1a.

Specifically, the model shows that the pass-through is incomplete even for a high-productivity firm, meaning that not all cost shocks are passed on to prices. However, the magnitude of incomplete pass-through is more than three times higher compared to the average pass-through of firms in the top two-thirds of the cost distribution.

As discussed earlier, customers tend to remain loyal to their previous supplier due to search costs, resulting in higher persistence of firm demand compared to firm prices and productivity. If a cost shock occurs, its effects on demand will last for approximately 10 months, while its impact on price lasts for only four months.

We tested this persistence using artificial data simulated from the model. We found that monthly autoregressive coefficients are 0.98 for demand and 0.75 for prices, indicating that the model accurately predicts that firm revenue persists more than prices.

Conclusion

The impact of price on firm value can be understood through two main channels: level of profit per customer and customer base dynamics. In other words, the price influences the mass of customers buying from the firm in the current period, as well as the future customer base. Therefore, setting the optimal price requires balancing the marginal benefit of a price increase (more profit per customer) with the cost (decrease in the customer base).

Our price-setting model provides a comprehensive framework for understanding the relationship between customer and price dynamic in equilibrium, with heterogeneous production and search costs. Empirical evidence from a large U.S. supermarket chain shows that increasing the price of a good is associated with a higher customer attrition rate. If firms are concerned about customer retention, the price pass-through of cost shocks will decrease. More productive firms offer higher continuation value to customers by charging lower prices. In contrast, higher prices are associated with a higher propensity for customers to search, resulting in higher demand elasticity. An increase in demand elasticity leads to firms reducing markups, amplifying the effect of demand shocks on consumption.

Samira Gholami is a research associate and Nicholas Trachter is a senior economist and research advisor in the Research Department at the Federal Reserve Bank of Richmond.

To cite this Economic Brief, please use the following format: Gholami, Samira; and Trachter, Nicholas. (May 2023) "How Well Do Firms Retain Customers After Price Increases?" Federal Reserve Bank of Richmond Economic Brief, No. 23-16.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us