COVID-19 and Women's (Un)Employment

Special Report

May 13, 2020

The COVID-19 pandemic is rapidly rearranging the U.S. labor market. The most current data from the Bureau of Labor Statistics' monthly surveys, which record job losses through early April, indicate that women have been disproportionately affected. (Richmond Fed president Tom Barkin has spoken before about barriers to women's labor force participation.)

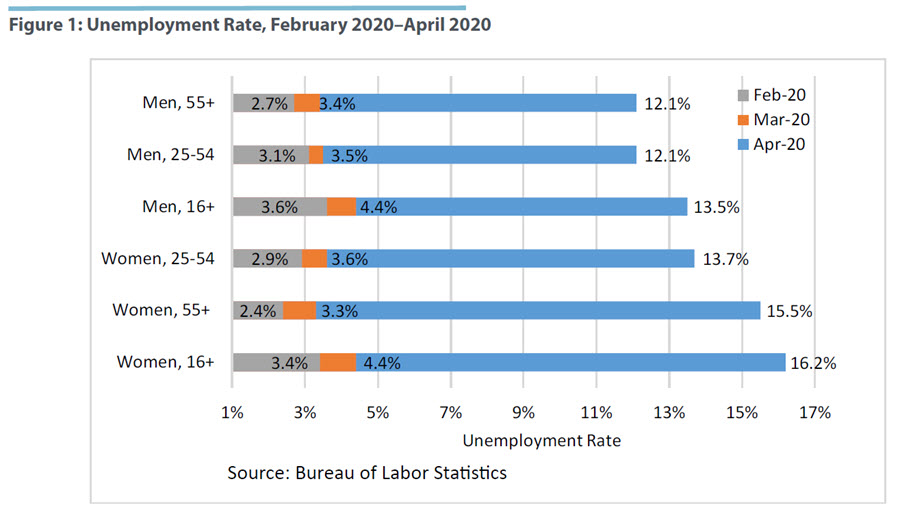

Three indicators — the unemployment rate, the labor force participation rate, and the employment-population ratio — from the bureau's survey of households (the Current Population Survey) indicate historic losses in women's employment.1 The unemployment rate for women ages 16 and over rose from 3.4 percent in February 2020 to 16.2 percent in April 2020. This is 2.7 percentage points higher than the unemployment rate for men the same age (13.5 percent). The unemployment rates for women are now higher and have risen faster than the same rates for men across all age groups. However, the unemployment rate does not tell the whole story as it may miss those on temporary layoff who were misclassified as "employed but not at work."2 Additionally, the unemployment rate does not include people who have dropped out of the labor market.

To better understand attachment to the labor market, we typically look at labor force participation rates, which measure the percentage of the population that is either working or actively looking for work. After a general decline from 2000 to 2015, the prime-age (25-54) women's labor force participation rate rose to 77 percent in February 2020, from a recent low of 73.3 percent in 2015. But labor force participation began falling again in March and, by April, had dropped to 73.6 percent. This indicates not only that many women have become unemployed, but also that many have ceased looking for work. This decline in women's labor force participation might be because many women are choosing not to look for work until after the pandemic is over. For example, perhaps they expect to return to their previous jobs, they have extra caretaking responsibilities due to school closures or sick relatives, or they are unable to look for work due to social distancing.

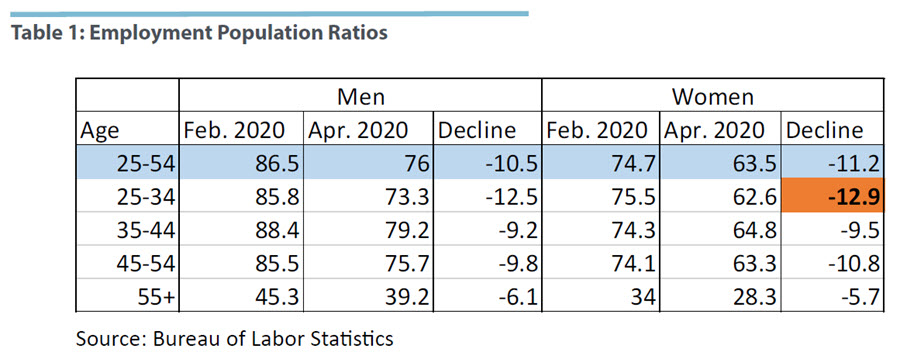

A third way to view employment among women is the employment-population ratio, which is the percentage of the population that is working. For both men and women, the April month-over-month drop in the employment-population ratio was the largest on record (records date back to 1948). Since the beginning of the crisis, the percentage of women between the ages of 25 and 54 who are working has fallen by 11.2 percentage points. The decline was largest among younger workers, ages 25 to 34. For women in this age group, the employment-population ratio declined by 12.9 percentage points between February and April. (See Table 1.)

The bureau also provides data on payroll employment through its survey of establishments (the Current Employment Survey). Since the beginning of the crisis, total nonfarm payroll employment has declined by approximately 21.4 million jobs. Nearly 55 percent of those jobs — 11.7 million — had been held by women. (On average in 2019, women held about 50 percent of total nonfarm jobs.) In 2019, women held 53.6 percent of jobs in the service sector, a broad category that includes those industries most directly exposed to the losses created by social distancing. The service-producing sector lost almost 18 million jobs in March and April, and 58.7 percent of all jobs lost were held by women. This pattern, in which women make up a higher percentage of jobs lost than they do of total jobs held in a given industry, has emerged in several of the service-producing industries. Within retail trade, for example, women accounted for 49.6 percent of total employment in 2019, but 61.2 percent of jobs lost since the crisis began were held by women. Similar disparities can be found within wholesale trade (in which women held 30.1 percent of jobs but were 37.1 percent of losses), transportation & warehousing (25.5 percent of jobs and 40 percent of losses), professional and business services (45.6 percent of jobs and 50.9 percent of losses), education and health services (77.3 percent of jobs and 83.3 percent of losses), and in the category "other services," which includes, for example, both personal care services and maintenance work (53.4 percent of jobs and 65.9 percent of losses). Other services industries that saw a similar, if much less pronounced, pattern were leisure and hospitality and information.

The full extent of the employment effects of the pandemic remains to be seen. Will employment losses continue to disproportionately affect women? When the recovery begins, will women's employment rebound more rapidly? Will increased care responsibilities, whether for children, the elderly, or at-risk family members as well as recent changes to unemployment insurance, affect women's employment and their attachment to the labor force over time?

Abigail Crockett is a research analyst and Nina Mantilla is the special assistant to the president at the Federal Reserve Bank of Richmond.

1

The bureau's Current Population Survey (CPS) is a monthly survey of approximately 60,000 households. Thus, monthly data drawn from the CPS may be subject to large sampling errors, particularly for population sub-groups. The data shown here are meant to provide a first glimpse into how women's employment has been affected by the COVID-19 pandemic. All figures are seasonally adjusted unless otherwise noted.

2

The bureau estimates that the unemployment rate would be approximately 5 percentage points higher if people classified as "employed not at work for other reasons" were instead classified as unemployed. The unemployment rate for women in April would be above 20 percent if women in this category were instead counted as unemployed (not seasonally adjusted).

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.