The Unconventional Oil and Gas Boom

A dramatic shift is taking place in the U.S. energy sector. For decades, analysts and policymakers assumed that as U.S. reserves of oil and natural gas dwindled, domestic production would decrease gradually and imports would increase steadily. But technological advances in extracting oil and natural gas along with higher energy prices have changed those assumptions. U.S. energy production has risen sharply in recent years and is expected to continue to grow at remarkable rates in coming decades — with benefits for the U.S. economy overall as well as within the Fifth District.

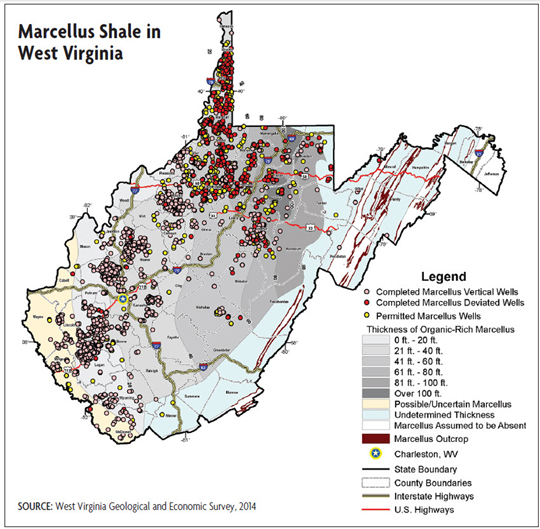

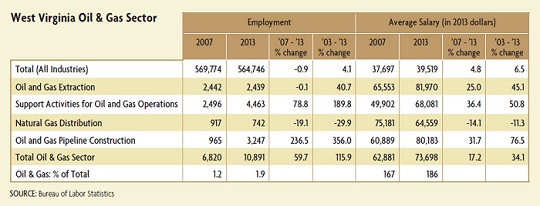

One of the most active regions is the Marcellus Shale, which underlies most of West Virginia, western Maryland, and parts of Ohio, Pennsylvania, and New York. The Marcellus Shale is a rock formation located deep beneath the earth's surface that contains vast amounts of natural gas. West Virginia and Pennsylvania have been actively encouraging the development of this resource in recent years, and the growth in production and the impact on local economies has been tremendous. In December 2013, the Marcellus region provided 18 percent of total U.S. natural gas production — a remarkable increase from almost no production just six years earlier. For the local communities at the epicenter of this production boom, the demand for workers and housing has jumped to the point where both are often in short supply. While this transformation of the energy sector is still in its early stages, the potential long-term impact on the regional and national economy is expected to be considerable.

There are a number of concerns surrounding the oil and natural gas boom, particularly its potential effects on the environment and nearby communities. The sector would face regulatory challenges if research indicated that current methods of production create substantial health or environmental risks. The potential benefit of these resources is so great, however, that additional regulations would likely only slow development in the sector.

Unconventional Oil and Natural Gas

The U.S. energy boom is due to the development of "unconventional" oil and natural gas. Unconventional refers to the fact that the oil and gas are trapped in rock formations with very low permeability and alternative methods are needed to extract them. Examples include "tight oil" and "tight gas," which are found in rock formations such as siltstone, sandstone, limestone, and dolostone; shale gas, which is natural gas found in shale, a fine-grained sedimentary rock with very low permeability; and coalbed methane, which is natural gas found in coalbeds. All of these hydrocarbons are extracted in ways that differ from "conventional" wells where the oil and natural gas naturally flow or can be pumped from an underground reservoir to the surface.

Three factors came together to make production of unconventional oil and natural gas economically viable: horizontal drilling, hydraulic fracturing, and increases in oil and gas prices. While horizontal drilling and hydraulic fracturing are not new, significant technological advances in recent decades have allowed developers to better target and more efficiently extract the oil and natural gas. The process of horizontal drilling and hydraulic fracturing (commonly referred to as "fracking") is more expensive than drilling a conventional vertical well, but higher prices for natural gas have made these techniques economically viable. At some of the early unconventional formations (or "plays"), such as the Barnett Shale in Texas or the Bakken formation in Montana and North Dakota, it wasn't until the mid-2000s, after energy prices rose sharply, that there was more widespread usage of horizontal wells and hydraulic fracking. In the Barnett Shale, one of the nation's most developed shale plays, the number of producing horizontal wells rose from less than 400 in 2004 to more than 10,000 in 2010.

So what exactly is fracking? Fracking involves injecting fluids into rock formations to create fractures in the rock that allow the oil and natural gas to flow through the well to the surface. A horizontal well that utilizes fracking techniques is dug in several stages. The well is drilled vertically to a predetermined depth, depending on the depth of the rock formation, and then the well is "kicked off' or turned at an angle until it runs parallel within the reservoir. The well can extend up to three miles through the reservoir, allowing for a greater number of access points. In drilling the well, several casings are cemented into place to provide stability and to ensure that the fracking fluids and the hydrocarbons do not escape into the surrounding soil.

There has been a lot of controversy surrounding fracking, particularly about its potential impact on the environment. There are concerns that the oil and gas could pollute the groundwater through faulty well design or construction or through migration to the surface. In addition, there are concerns about the fracking fluid used in the process. Fracking fluid is roughly 98 percent water and sand, but the chemicals it contains could pollute drinking water if released. Faulty well design or construction could result in the fluid escaping into the surrounding environment. Improper handling of the fluid that returns to the surface through the well is another issue. This fluid is injected into disposal wells that are thousands of feet underground, but there are concerns that the fluid could migrate upward into groundwater.

There are also concerns related to fracking and earthquakes. According to the U.S. Geological Survey (USGS), fracking causes earthquakes that are typically too small to be noticed. The USGS has found, however, that the injection of wastewater into disposal wells has the potential to induce larger earthquakes. Of the 40,000 disposal wells in the United States that are related to oil and gas activities, there were roughly a dozen cases where larger earthquakes were detected. The USGS is currently researching the issue to better identify induced earthquakes, understand why they occur in some places but not in others, and determine what should be done once they occur.

Another issue is the amount of stress placed on nearby towns and cities, which typically experience increased traffic, greater use of local water resources, and more air and noise pollution.

Overall, while there are risks and concerns, there does not appear to be an inherent problem with this particular method of energy extraction. In 2004, the Environmental Protection Agency (EPA) published the results of a study on hydraulic fracturing used in coalbed methane reservoirs to evaluate the potential risks to underground sources of drinking water. The study focused on coalbed methane reservoirs because they are typically closer to the surface and to underground sources of drinking water. The EPA concluded that "the injection of hydraulic fracturing fluids into [coalbed methane] wells poses little or no threat to [underground sources of drinking water]." In 2012, in response to persistent environmental concerns about the surge in fracking, the EPA began a new study to "understand the potential impacts of hydraulic fracturing on drinking water resources." The agency will release a report for peer review and comment in 2014.

The Boom in Unconventional Production

The boom in unconventional oil and natural gas production is expected to increase in coming years. U.S. tight oil production has increased from under 500,000 barrels per day in 2008 to over 2.5 million barrels in 2013. Total U.S. crude oil production increased from 5 million barrels per day in 2008 to 7.4 million barrels per day in 2013, a 49 percent increase. The U.S. Energy Information Agency (EIA) is forecasting production to reach 9.6 million barrels per day in 2015 — which would match the record U.S. production level reached in 1970. As these formations are slowly exhausted, production is anticipated to then gradually decline in subsequent decades to 7.8 million barrels per day in 2040, slightly higher than 2013 production levels. Notably, as these plays are developed, additional supplies are being found, resulting in sharp increases in proved reserves. Proved oil reserves increased from 19 billion barrels in 2008 to 26.5 billion in 2013, an increase of 39 percent.

The outlook for natural gas is even more astounding (see chart). U.S. shale gas production increased from roughly 1 trillion cubic feet (tcf) in 2006 to more than 8 tcf in 2012. The EIA expects this trend to continue. Shale gas production is expected to reach 17 tcf by 2040. As a consequence, total natural gas production is forecast to increase from roughly 24 tcf in 2013 to more than 33 tcf in 2040. And as was the case with oil reserves, proved natural gas reserves increased sharply in recent years, from 200 tcf in 2004 to 350 tcf in 2013 — an increase of 75 percent in less than a decade.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us