Shifting into Neutral

In 1994, the Federal Reserve launched a pre-emptive strike against inflation in a series of interest rate hikes that drew controversy at the time

Econ Focus

Second Quarter 2015

How does a central bank normalize monetary policy after a long spell of unusually low interest rates? This may seem like a question very much of the present, as Fed leaders ponder interest-rate policy following the Great Recession of 2007- 2009 and the tepid U.S. recovery. But it's also a challenge the Fed confronted two decades ago. In 1994, the Federal Open Market Committee (FOMC) wrestled with a similar dilemma as it considered emerging from a sustained period of low interest rates, amid signs of a reviving economy, growing aggregate demand, and no obvious signals of inflation. At the time, a pre-emptive strike had never been done before. As then-Chairman Alan Greenspan put it in his 2007 memoir, The Age of Turbulence, such a strategy carried great risk. "Let's jump out of this sixty-story building and try to land on our feet," is how he described the feeling.

Many Americans remember the 1990s as remarkable boom years, when unemployment dropped to record lows, productivity kept climbing, and inflation barely nudged. But the early years of the 1990s were a different story. In 1990-1991, the United States suffered a recession, followed by a sluggish recovery and rising unemployment. Facing this environment, the FOMC repeatedly cut the federal funds rate until real short-term interest rates had effectively dropped to zero in the fall of 1992.

The picture improved substantially in 1993, especially by the fall, most notably in business investment and housing starts, while leading indicators of inflation — such as low inventory levels and rising inflation expectations reflected in longer-term bonds — began to appear. By year-end, the FOMC coalesced around the view that such historically low rates were no longer needed to spur spending and investment. But the good economic news also posed a new dilemma: How gradually should the FOMC dial back its accommodative stance, given that the recession and high unemployment were still recent memories? How could it take its message to the public when inflation appeared contained? And what would be the impact of making such a move given that it had been five years since the FOMC last tightened policy?

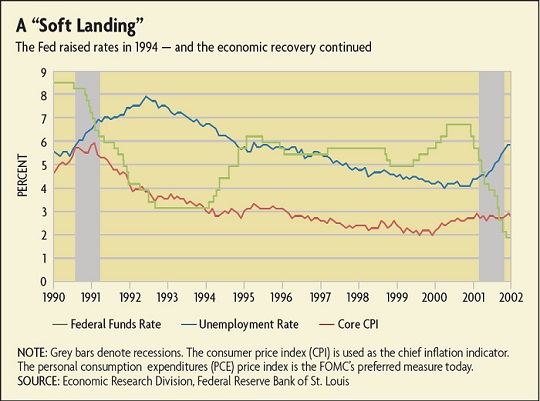

Over the course of the next year, from January 1994 to January 1995, the FOMC raised the fed funds rate seven times, from 3 percent to 6 percent, in what was later seen as a turning point. Many economists view this episode as the first major tightening action by the FOMC that was truly pre-emptive, moving ahead of concrete evidence of inflation. The 1994 cycle was also the first time that the FOMC issued a statement to announce policy changes as a way to explain its decision to the public as well as signal its anti-inflation commitment to markets. Even though the FOMC at the time did not view the statement as a sea change, it turned out to be the first in a series of moves establishing greater transparency and anchoring public expectations about monetary policy over the medium and long run.

The 1994 hikes provoked strong political resistance — especially in Congress — as well as ongoing turmoil in bond markets. But as the year went on, the fundamentals bore out the FOMC's assessment that reverting to tighter monetary policy would not stop the recovery in its tracks. The economy continued to expand, rising from 2.7 percent real GDP growth in 1993 to 4 percent in 1994. Growth did eventually decelerate in 1995 — as Fed forecasts had expected — but it was a "soft landing" rather than a hard fall. In fact, the economy expanded by 2.7 percent in 1995, although it slowed down in the fourth quarter to less than 1 percent. Meanwhile, inflation stayed contained, with the core consumer price index (which omits volatile food and energy prices) generally hovering around or below 3 percent in 1994 and 1995. To the surprise of many, the unemployment rate kept on falling, from 6.6 percent in January 1994 to 5.6 percent in early 1995 — more than a full percentage point below FOMC forecasts in early 1994. (See chart below.) And long-term bond rates — after rising in the spring and summer — started falling by late 1994 and eventually stabilized by early 1996. This movement indicated to the FOMC that long-term inflation expectations had been anchored by the series of hikes and the accompanying announcements. The Fed's oft-stated intention that it would contain inflation appeared at long last to be attaining credibility.

A Gradual Healing

A chief source of the concern to the FOMC in late 1993 and early 1994 was that the federal funds rate had been unusually low for more than a year. At 3 percent, that rate might not seem so low relative to today's near-zero levels. However, the FOMC compares the inflation-adjusted (or "real") fed funds rate to the economy's long-run "natural" real rate — the rate that will neither stimulate nor depress economic activity — and it sets the real fed funds rate relatively low to support economic activity during a recession. (See "Jargon Alert" in this issue.) Since the Great Recession, economists estimate the natural rate has fallen close to zero, but in the early 1990s, most calculations put it at 3 percent or higher. In 1994, with roughly 3 percent inflation, the 3 percent fed funds rate thus represented an "accommodative" stance rather than a neutral one.

One reason for the persistence of such low rates was the legacy of the 1990-1991 recession, which saw real GDP contract in the fourth quarter of 1990 by an annualized 3.5 percent, followed by a 2 percent drop in the next quarter. FOMC members were especially concerned over the troubled banking and thrift industry, as hundreds of financial institutions collapsed in the late 1980s and early 1990s under the weight of bad loans. Another factor was the recessionary effect of the spike in oil prices following the Iraqi invasion of Kuwait in 1990. Regional downturns in places such as New England and Texas were especially severe.

The FOMC had responded to these conditions by cutting the fed funds rate a full 3 percentage points, from 6 percent to 3 percent, from mid-1991 to late 1992. Despite the official end to the recession in March 1991, however, employers kept shedding jobs, causing unemployment to rise through June 1992, up to 7.8 percent. Absent any early signs of inflation, and with the FOMC's internal "Greenbook" forecast pointing to ongoing slack in the labor market, these conditions had convinced Greenspan and a majority of FOMC members that low real interest rates were appropriate, especially since businesses and households were struggling to repair their balance sheets.

By 1993, however, the economy had turned the corner. GDP growth rapidly picked up, while the unemployment rate fell below 7 percent by fall 1993. Meanwhile, several leading indicators caught the FOMC's notice, notably, the yield on 30-year Treasuries, which jumped by almost half a percentage point in the fourth quarter. To some members, this indicated that long-term inflation expectations were on the rise even though measured inflation was holding steady.

'A Slightly Shabby Notion'

Although the FOMC was largely united on the need for a policy shift by the winter of 1993, many on the committee, including Greenspan, were concerned about the market impact of even a modest tightening. As a way to ease the surprise, Greenspan decided to make public comments just ahead of the FOMC's first meeting of the year. "Short term rates are abnormally low," he stated in congressional testimony in January 1994. "At some point, absent an unexpected and prolonged weakening of economic activity, we will need to move them."

When the FOMC gathered for its first meeting of the year on Feb. 3-4, the discussion focused on the fourth-quarter strength of a number of indicators, including housing starts, consumer durables, business fixed investment, and a jump in the hours of an average workweek. Business inventories remained at low levels, which caused some members to worry that tight supply would not be able to keep up with growing consumer demand. More broadly, the accelerating pace of GDP growth in the fourth quarter — initially estimated at an annualized 5.9 percent, later revised to 7.0 percent — suggested to the committee that the economy was ready for a shift away from zero real interest rates.

"We have had an extraordinarily successful run in restoring balance to a disturbed economic system," Greenspan told his FOMC colleagues at the February meeting as he concluded his case for a rate hike. "We haven't raised interest rates in five years, which is in itself almost unimaginable … The presumption that inflation is quiescent is getting to be a slightly shabby notion."

Greenspan laid out two possibilities to the committee. One was to raise the federal funds rate by half a percentage point, or 50 basis points, from 3 percent to 3.5 percent. The economic fundamentals, in Greenspan's view, merited such a shift, but this risked considerable market disruption, given that it would be the first rise in five years. The other risk was that 50 basis points might be seen as a one-off measure, when in fact the FOMC expected that it would have to conduct a series of hikes through the year that were commensurate with rising output and rising demand.

A better approach, argued Greenspan, would be to lift the fed funds rate by only 25 basis points but then make an announcement after the meeting — an unprecedented move at the time — to signal that this was a first step in a broader strategy to move ahead of inflationary pressures. Furthermore, he argued, the shock to markets would be less severe than with an immediate move of 50 basis points. As the discussion unfolded, this view prevailed among the committee members, including those who thought the initial hike should be higher, and they voted unanimously in favor.

Despite its great significance in retrospect, the FOMC members generally viewed the decision to state the policy change publicly as an ad hoc move that addressed the specific conditions of their announcement. Greenspan, who had in the past opposed the idea of public announcements on grounds that they limited the Fed's flexibility, made clear to the committee he did not view this move as establishing a new practice.

"We don't have to announce our policy moves; there's nothing forcing us to do so," argued Greenspan. "The issue is not whether if we do something, we will be forced to do it again. I think we can avoid that. … I see no reason for such an announcement to be a precedent."

As it turned out, the decision to issue an announcement was the first in many steps toward greater transparency during Greenspan's tenure. It was not only the first time the FOMC offered to the public a summary and brief explanation after meetings that formalized a policy change; it was also the first year that most policy changes were made at the meetings. Previously, it was common for the FOMC to make the policy decisions during conference calls between sessions. Another major step occurred in 1999, when the FOMC decided to issue statements, in addition to more precise language on its near- and mid-term policy intentions (or "tilt") after every meeting, not just after those when a policy change occurred. And three years later, it started making the vote count and dissents public.

The 'Bond Bloodbath'

Despite Greenspan's public signals and the calming intention behind the first-ever statement, markets met the news of the rate hike with surprise, with the Dow Jones Industrial Average dropping almost 2.5 percent. A more unusual reaction, however, occurred in the bond markets. The yield on 30-year Treasuries — which had been one measure, in part, of longer-term inflation expectations and generally was not prone to sudden movements — jumped by 40 basis points, compared with only 25 for short-term Treasuries. This move was the start of a long, massive sell-off in the U.S. bond market, which wound up losing $600 billion in value from January to September of that year. (Because bond values and yields have an inverse relationship, the increase in yields corresponds to a decline in bond prices.)

To some on the committee, including Broaddus, that jump meant the FOMC's move had not been sufficient in anchoring expectations firmly on the Fed's anti-inflation commitment and, in fact, showed that the markets still believed that long-term inflation was a threat. In retrospect, what also may have been going on was an early harbinger of the dynamics at play in 2008, although on a much smaller scale. Highly leveraged institutions such as hedge funds had been borrowing short-term to buy longer-term, higher-yielding debt. As long as bond spreads were stable, these firms could offer their investors double-digit returns because they could keep on financing their debt. But once the Fed moved in February 1994, even a modest rise in short-term financing costs could upend this strategy. As a result, these bondholders were forced to sell the securities they held, including higher-yielding long bonds, to cover the borrowing costs of their short-term debt. A long-bond sell-off, in turn, drove those yields higher and steepened the yield curve. Banks and insurance companies were also badly affected. That year is still known among investors as "the bond bloodbath."

The FOMC discussed this turbulence as it weighed its options at its March meeting. Generally, the indicators that it noted in late 1993 — housing, business fixed investment — were still strong. Inflation itself remained moderate, as were wage gains. The consensus was that the FOMC should announce a further tightening, with the only question being how much.

Assessing the recent market turmoil, Greenspan said he saw an analogy to the 1987 crash, which he said "stripped out a high degree of overheating." Before the Feb. 4 decision, he said, "I don't think we were aware of the apparent underlying speculative elements involved in the markets on a worldwide basis that … our February move unearthed." But the pattern was otherwise similar. "While this capital gains bubble in all financial assets had to come down, instead of the decline being concentrated in the stock area, it shifted over into the bond area," he argued.

Given this market volatility, Greenspan concluded that the FOMC should only take another modest 25 basis point step. The committee agreed, although this time two members — Broaddus and Cleveland Fed President Jerry Jordan — dissented on grounds that a 50 basis point increase was needed to adequately pre-empt emerging inflation pressures.

Looking back today, Broaddus said he still believes his dissent was the right decision, in large part due to his concern over the movement in long bond yields. But he also notes that one tool economists today use to gauge inflation expectations — the difference between yields on a particular inflation-protected Treasury (known as TIPS) and non-indexed Treasuries — was not available yet; TIPS were not issued until 1996.

"Instead of TIPS, we had to look at long bond rates. But this was enough to put us on alert," he says. "That spring and summer, I still thought we needed to be more aggressive."

The Glide Path

By July 1994, the FOMC had taken the fed funds rate to 4.25 percent and decided to take a pause at its meeting that month on the grounds that the effects of its action in the spring were starting to be felt. More broadly, global currency markets had become volatile, and the committee did not want to add to those pressures. The committee also decided to hold off on issuing a public announcement this time — since there was no policy change to announce — and to revisit later the broader question of issuing statements. (It decided in January 1995 to issue public statements when it had voted for a policy change and to reserve the right to issue statements even when there was no policy change.)

Regardless of the intent of greater transparency, the move did not mitigate broader criticism from lawmakers over the change in policy. During Greenspan's semiannual Humphrey-Hawkins testimony before Congress in July, Sen. Paul Sarbanes (D-Md.) charged that the Fed had "engineered a slowdown in the economy despite the absence of an inflation problem. The domestic economy is generating less inflation than it has in three decades."

Another target was the Fed's 12 regional Reserve Bank presidents, who were brought in to testify over the course of that year and were seen by some lawmakers as excessively hawkish. Rep. Henry Gonzales (D-Texas) introduced a bill that would, among other things, remove the presidents as voting members of the FOMC. The legislation failed to gain traction, but some of its other proposals, including a broader audit of the Fed, remain in circulation today.

The FOMC went on to lift rates again in August and November as the economy looked increasingly robust. Altogether, the fed funds rate had risen to 5.5 percent by year-end, with the committee voting for one final increase in January to bring the rate to 6 percent. Unemployment was steadily dropping, while consumer spending and business fixed investment stayed at brisk levels. Despite higher mortgage interest rates (a result of rising long-term bond yields), the housing market was picking up. Reflecting the committee's ongoing concern that fall, the November hike, in fact, was the biggest of the year — a full 75 basis points.

Former Fed Vice Chairman Alan Blinder, who served on the FOMC from 1994 to 1996, describes the episode as remarkable for several reasons. One was the degree of unity in the final votes, even though the actual debates preceding them had "a lot less cohesion," in his words.

"Greenspan was very good in using the wording of the statement to tack one way or the other, making sure as many members were on board as possible," says Blinder. "He would use the 'bias' very skillfully. But there was a lot more disagreement in those debates than the final votes would suggest."

During his time on the FOMC, Blinder notes, he had his differences with Greenspan over transparency issues. But he still considers the 1994 cycle "a complete success in capping inflation.

"We held inflation at 3 percent while engineering a soft landing with the economy at full employment," he says. "That is as perfect as you could get."

Readings

Greenspan, Alan. The Age of Turbulence: Adventures in a New World. New York: Penguin Press, 2007

Goodfriend, Marvin. "The Phases of U.S Monetary Policy: 1987 to 2001." Federal Reserve Bank of Richmond Economic Quarterly, Fall 2002, vol. 88, no. 4, pp. 1-17.

Pakko, Michael. "The FOMC in 1993 and 1994: Monetary Policy in Transition![]() ." Federal Reserve Bank of St. Louis Review, March-April 1995, vol. 77, no. 2, pp. 3-26.

." Federal Reserve Bank of St. Louis Review, March-April 1995, vol. 77, no. 2, pp. 3-26.

"Minutes of the Federal Open Market Committee." Board of Governors of the Federal Reserve Sytem, Feb. 3-4, 1994![]() ; March 22, 1994

; March 22, 1994![]() .

.

Sellon, Gordon H. "Monetary Policy Transparency and Private Sector Forecasts: Evidence From Survey Data.![]() " Federal Reserve Bank of Kansas City Economic Review, Third Quarter 2008, pp. 7-34.

" Federal Reserve Bank of Kansas City Economic Review, Third Quarter 2008, pp. 7-34.

Walsh, Carl. "What Caused the 1990-1991 Recession?![]() " Federal Reserve Bank of San Francisco Economic Review, 1993, no. 2, pp. 33-48.

" Federal Reserve Bank of San Francisco Economic Review, 1993, no. 2, pp. 33-48.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us