Preparing Unemployment Insurance for a Downturn: The Carolinas

In the aftermath of the Great Recession, the United States saw unemployment rates rise to levels it had not seen since the early 1980s as employers shed workers by the millions. Workers who had lost their jobs could not find other work and flooded into unemployment offices around the nation applying for benefits to ease the shock to their household income. Unemployment insurance claims and payouts soared, straining programs from coast to coast.

Before all was said and done, 36 states were overwhelmed and saw their programs reach insolvency, requiring them to borrow money from the federal government to continue paying benefits to qualifying workers. The trauma to states' unemployment insurance trust funds prompted policymakers in several states to make significant changes to their programs in order to place them on a more sustainable footing for the next recession. Two of those states lie in the Fifth District: North Carolina and South Carolina. This article looks at the two states' unemployment insurance programs after the Great Recession and how they have changed as a result. Moreover, it looks at how well prepared each is to weather the next economic downturn and what recent changes will mean for workers when it hits.

Employment During and After the Recession

The Great Recession had an uneven impact on employment and unemployment in the nation as well as in the Fifth District. Twelve months into the downturn, employment in the District was faring better than the nation as a whole. The District of Columbia and, to a lesser extent, Maryland and Virginia were buoyed by the stabilizing presence of the federal government. Meanwhile, the nascent renaissance in energy production was benefiting West Virginia. Thus, none of these four jurisdictions saw job losses that matched those of the nation. In fact, employment in Washington, D.C., was actually higher than it had been when the recession got under way.

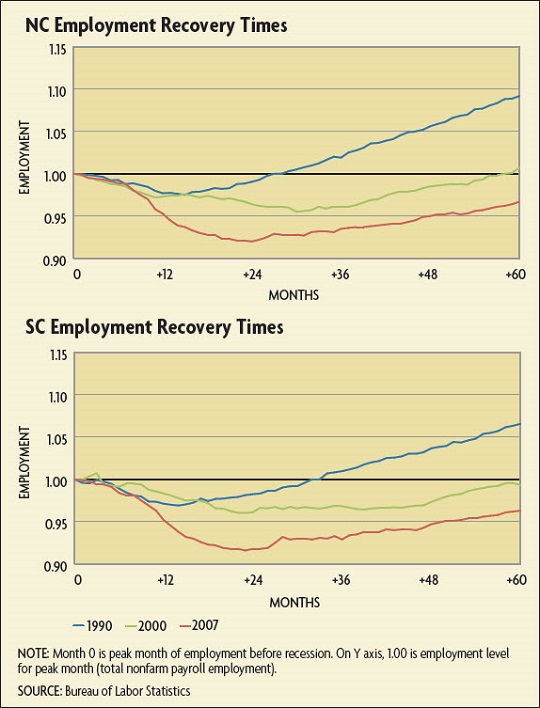

Without the omnipresence of the federal government or an energy revolution of their own, North Carolina and South Carolina felt the effects of the recession immediately and severely. And the severity of the job losses persisted there throughout. By the time employment had reached its trough in February 2010, 8.7 million jobs had been lost nationally, amounting to a 6.3 percent decline, but job losses in North Carolina and South Carolina amounted to 7.8 percent and 8.2 percent, respectively

The outsized employment reaction in the Carolinas could have been expected given the severity of the downturn and the region's economic structure. Prior to the recession, both states were much more heavily concentrated in manufacturing and construction, two sectors that were particularly hard hit and where job losses were much more acute.

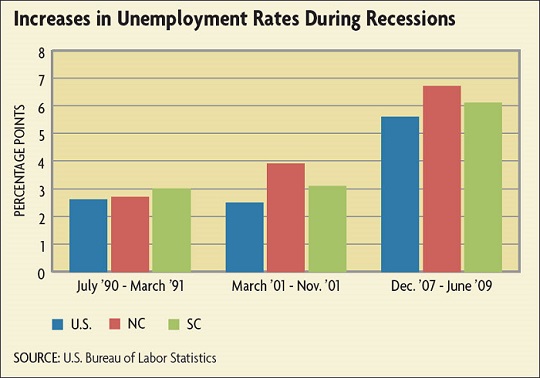

While the national rate of unemployment climbed 5.6 percentage points as a result of the Great Recession (from 4.4 percent to 10 percent), North Carolina's rate jumped by 6.7 percentage points (to 11.3 percent) and South Carolina's by 6.0 percentage points (to 11.7 percent).

But even the rise in the unemployment rates did not fully reflect the level of strain that was and would be placed on the states' unemployment insurance programs. One of the more extraordinary facets of this labor market downturn was the record high percentages of workers who were unemployed for more than 26 weeks — the long-term unemployed. Even as the number of workers entering the unemployment insurance pipeline began to wane in early 2009, still fewer were leaving it.

As a result, 36 states depleted the balance of revenues within their unemployment insurance accounts at some point during or after the recession and took out federal loans to continue paying benefits. North Carolina and South Carolina were among the most affected states. At certain points during their programs' financial crises, North Carolina had the second-highest federal loan-to-total wage bill in the country, and South Carolina was once ranked seventh.

Due to the severity of the trust fund crises, the two states took steps to reduce benefit payouts to pay down their debt to the federal government and put their programs on better-prepared footing.

Changes to Maximum Duration of Benefits

The federal-state unemployment insurance program is currently celebrating its 82nd year of existence. In the early decades of the program's history, there was quite a bit of variability in the maximum duration of unemployment insurance benefits that state legislators had written into law. And in most instances, the maximum duration was less than 26 weeks.

That began to change in the 1960s during President Johnson's "Great Society" and "War on Poverty" as states began moving toward a consensus of 26 weeks. So since the middle part of the 1960s up until the Great Recession, every state had a maximum unemployment insurance duration of at least 26 weeks.

Yet while the vast majority of state legislatures chose to set the maximum duration of unemployment insurance benefits at 26 weeks, there was (and is) nothing in federal law that mandates a maximum duration of 26 weeks.

It is somewhat surprising that this basic structure of maximum duration of benefits has held for so long. According to the National Bureau of Economic Research, prior to the Great Recession, the U.S. economy had gone through six economic downturns since the middle part of the 1960s, and state legislators across the nation made no significant adjustments. Why?

There are a variety of reasons why states choose not to undertake such reductions in maximum durations. One of the biggest lies in the spirit of the program itself — to provide some support to workers who have lost their job through no fault of their own. The unemployment insurance payments help ease the blow to households'ability to continue spending to meet basic needs while simultaneously easing the shock to the broader macroeconomy, since consumer spending is such a big part of it.

Another reason maximum durations were not reduced during those prior downturns is that none were nearly as severe as the Great Recession, nor did they have the same impact on the solvency of states' unemployment insurance programs. Reducing the maximum duration during a "regular" downturn is politically unpopular, while reducing it during an expansion is not a political priority.

The severity of the Great Recession changed the math. States that reach insolvency are still required by law to make benefits payments to qualified recipients. To do so, they borrow money from the federal government. Those funds, however, do not come without their costs — employers in affected states are assessed an additional payroll tax until the state has paid off its debt, thereby increasing effective labor costs in the state.

Following the Great Recession, policymakers in North Carolina and South Carolina were forced to balance objectives that were somewhat at odds: paying off the federal debt, providing benefits to ease the burden of unemployment on households, and keeping taxes on employers low to stimulate job creation.

In 2011, South Carolina was in the first wave of states that passed legislation to decrease the maximum number of weeks of eligibility, reducing its maximum from 26 weeks to 20 weeks effective on June 14, 2011. This change remains in effect today. South Carolina's law change was pretty straightforward, with the maximum duration simply tied to the individual claimant's eligibility to continue receiving benefits.

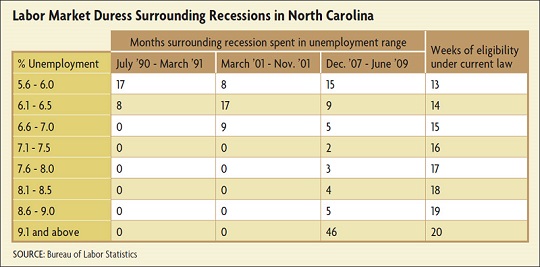

North Carolina's changes were slower in coming, more complex, and somewhat controversial. In the 2013 legislative session, North Carolina's assembly passed a law that not only reduced the maximum duration for eligibility, but also instituted a variable maximum that is dependent on the state's unemployment rate. (See table below.) The state's maximum eligibility ranges from 12 weeks (when North Carolina's unemployment rate is less than 5.5 percent) to 20 weeks (if the unemployment rate tops 9 percent). An individual's maximum benefits duration is determined by the state's seasonally adjusted unemployment rate at the beginning of a six-month "base period" in which the initial claim was filed. The six-month base periods begin in January and July each year.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us