Speeding Up Payments

Can payments be made to work faster, safer, and more efficiently?

Econ Focus

Fourth Quarter 2017

Businesses and individuals in the United States make more than 100 billion payments each year. Cash, credit cards, and debit cards are ubiquitous in retail transactions, the automated clearinghouse (ACH) handles recurring transfers like bill payments and payroll deposits, and consumers and businesses wrote nearly 20 billion checks in 2015.

For the most part, participants don't think twice about how any of these payments work. But as commerce has accelerated, some observers have begun to ask whether payments are stuck in slow motion. Consumers are now accustomed to receiving goods ordered online the next day or even within hours, and businesses can send information across distributed supply chains instantaneously via email or messaging systems. Over the years, advances in technology have sped up some aspects of the payment process, but for most noncash payment methods, final transfer of funds and settlement between participating financial institutions can take a day or more. Even newer options like mobile payments still rely on legacy payment networks built in a pre-Internet era.

Several other countries — including recently Singapore, Switzerland, and Mexico — have developed faster payment options that promise real-time or near-real-time transfer of funds. In 2015, the Fed expressed a desire for a faster, safer, and ubiquitous payment solution for the United States. That same year, it gathered together members of the payment industry into a Faster Payments Task Force![]() , which in July 2017 released its final recommendations and some solutions proposed by the private sector.

, which in July 2017 released its final recommendations and some solutions proposed by the private sector.

What is "Fast"?

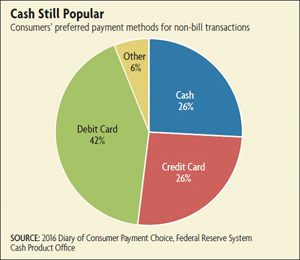

Just what is a fast payment? In many ways, physical cash is a perfect example. Every aspect of a cash transaction is settled immediately when the money physically changes hands between payer and recipient. The utility of this speed and finality may partly explain why rumors of cash's demise have been greatly exaggerated. According to preliminary findings![]() from the Fed's Diary of Consumer Payment Choice, the number of U.S. notes in circulation has grown steadily since 1980. In 2016, there were $1.43 trillion in notes in circulation. Large denomination bills are held both in the United States and abroad as a store of value, while smaller denomination notes continue to be used in over half of in-person payments under $10. Cash was generally preferred by about a quarter of consumers for non-bill payments in 2016. (See chart below.)

from the Fed's Diary of Consumer Payment Choice, the number of U.S. notes in circulation has grown steadily since 1980. In 2016, there were $1.43 trillion in notes in circulation. Large denomination bills are held both in the United States and abroad as a store of value, while smaller denomination notes continue to be used in over half of in-person payments under $10. Cash was generally preferred by about a quarter of consumers for non-bill payments in 2016. (See chart below.)

The Need for Speed

For individuals, faster settlement would provide a more accurate picture of the funds in their account. This could reduce the need for overdraft protection, as consumers could see fund availability in real time before making purchases. Faster payment settlement would also give individuals more flexibility with time-sensitive payments such as bills.

Faster settlement would allow funds from direct deposited paychecks to clear faster. (Some banks already credit recipients with funds from recurring payments before the transaction is fully settled, though this is not required.) This could benefit temporary workers in particular, allowing them to receive payment immediately upon completion of a job. Lastly, demand for a cash-like mobile payment method for person-to-person payments seems evident by the growth of third-party solutions such as Venmo and the recently launched Apple Pay Cash. Many of these solutions allow users to add funds to a digital wallet using a traditional payment method such as a payment card. They can then send those funds to other users' digital wallets instantly. But depositing funds into and withdrawing funds out of the digital wallet is still subject to the same settlement delays as traditional payment options.

A faster payment solution could hold a number of benefits for businesses as well. While check use has continued to decline since the mid-1990s, businesses still write an average of 24 checks a month, according to findings from the Fed's 2016 Payments Study![]() . One driver of this is the need for recordkeeping. Current noncash payment options do not have robust messaging capabilities that allow businesses to send both payments and detailed invoice information together electronically. A new payments platform could offer better e-invoicing options. Additionally, adopting a messaging standard like ISO 20022, which is used in faster payment systems in other countries, could facilitate cheaper, more efficient global transactions.

. One driver of this is the need for recordkeeping. Current noncash payment options do not have robust messaging capabilities that allow businesses to send both payments and detailed invoice information together electronically. A new payments platform could offer better e-invoicing options. Additionally, adopting a messaging standard like ISO 20022, which is used in faster payment systems in other countries, could facilitate cheaper, more efficient global transactions.

With faster settlement, businesses would also face less risk that a transaction might be canceled or withdrawn after the business has already delivered goods or services to a customer. To be sure, to some parties and in some instances, the ability to reverse noncash transactions can be a feature rather than a bug. This raises an important question about faster payment design: How closely should noncash payments emulate the immediacy and irrevocability of cash?

Settle Now or Later?

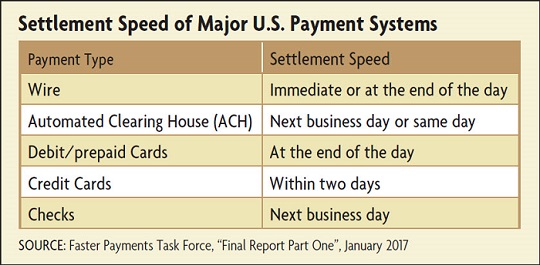

On a basic level, noncash payment settlement in the United States today functions similarly to how it did 200 years ago. In the 19th century, bank representatives would gather together at clearinghouses to settle accounts each day. This reduced the transaction costs of sending funds or representatives back and forth between numerous institutions and allowed banks to make one net deposit or withdrawal covering multiple transactions. Today, bankers may no longer have to physically gather in the same place to settle accounts, but payments are still collected and settled in batches at the end of the business day or some other predetermined period — a process referred to as deferred net settlement.

One way to speed up payments is to settle each transaction individually as it comes in, a method known as real-time gross settlement. The Fed actually pioneered the world's first real-time gross settlement payment platform in 1918: Fedwire. It is still used today to instantly transfer funds between financial institutions. But because access to Fedwire is limited and the fees associated with the service are high relative to other payment methods, it is generally used only for high-value bank-to-bank transactions.

There is nothing to say that real-time gross settlement couldn't be applied to retail payments, however. In fact, some countries, such as Switzerland and Turkey, have taken this approach with their faster payment systems. The benefit is that the entire transaction, from initiation to settlement, is completed all at once. This most closely resembles the speed and finality of physical cash. Indeed, of the final proposals presented by the Faster Payments Task Force, several of those featuring real-time gross settlement suggested using a digital currency such as a cryptocurrency.

Setting aside the practical and political questions about establishing a digital currency, there are other trade-offs to real-time gross settlement. In order to commit to settling each transaction as it occurs, payment service providers would need to keep more liquidity on hand to cover all anticipated outgoing payments throughout the day. Under deferred settlement, liquidity needs are lower since institutions only need to send a payment if they have a net negative balance with another institution at the end of the settlement period. One way that countries with real-time gross settlement payment systems have attempted to mitigate this is by limiting the total value that users can send over the system in a given period.

In an effort to get the best of both worlds, several countries have taken a hybrid approach to faster payments by separating the transfer of funds from the settlement stage. For example, the United Kingdom's Faster Payments Service clears transactions in real time and the recipient's financial institution immediately credits the recipient's account with the funds from the payment. The actual settlement whereby the payer's institution pays the recipient's institution happens later during one of three settlement windows throughout the day.

This approach delivers faster payments from the perspective of users while maintaining more efficient net settlement between payment service providers. It does expose the recipient's financial institution to some degree of credit risk, however, since it must deliver funds to the recipient before actually receiving them from the payer's institution. To minimize this risk, transactions using this type of faster payment system are generally irrevocable once initiated.

One Solution or Many?

In principle, countries are not limited to a single faster payment solution. In practice, however, economic forces may place limitations on the number of solutions that arise in the payments market.

Payment platforms are characterized by three features that may lead to market concentration: economies of scale, economies of scope, and network effects. Economies of scale exist when a producer's costs per unit fall as its production increases. Payment platforms have historically had high fixed costs but low or diminishing costs associated with each additional transaction.

Economies of scope exist when it is cheaper for one entity to produce several goods or services together. Payment platforms typically handle multiple stages of the payment process, from clearing to settlement, due to economies of scope. These forces tend to encourage market concentration, and historically this has been true of the payments market. For example, when the ACH network was first created, it had several operators; today, there are only two.

Network effects may also contribute to a concentrated payments market. Payment platforms are two-sided markets, meaning that a payment method needs to be both used and accepted by a large number of participants to be valuable as a means of exchange. For example, the more merchants who accept a particular payment card brand, the more valuable that card is to consumers because it can be used in more places. Likewise, the more consumers who carry a particular kind of payment card, the more valuable it is for merchants to accept it, since doing so increases their opportunities to make a sale.

As researchers from the Federal Reserve Board of Governors, the Kansas City Fed, and the Boston Fed discussed in a 2017 paper![]() , payment market concentration is not necessarily a bad thing. Having one or a small number of large payment operators can help ensure that payments are compatible and widely accepted across the country. Efficiency gains from economies of scale and scope can be passed on to users in the form of less costly payments. And it may be easier to enforce regulatory and security standards over a concentrated market.

, payment market concentration is not necessarily a bad thing. Having one or a small number of large payment operators can help ensure that payments are compatible and widely accepted across the country. Efficiency gains from economies of scale and scope can be passed on to users in the form of less costly payments. And it may be easier to enforce regulatory and security standards over a concentrated market.

On the other hand, the authors of the study also noted that user costs could be higher in a concentrated market due to a lack of competition, and some users might be underserved. Regarding innovation like faster payments, the authors found that the overall impact of market concentration is unclear. On the one hand, having market power gives a dominant payment operator incentive to innovate because it would reap all the rewards from a new offering. On the other hand, without competitive pressure, a payment operator may choose to maintain the status quo and continue profiting from existing technology.

The authors of the Fed study noted that technological advancements could reduce economies of scale and scope for payment processing, allowing a more decentralized market to emerge. This decentralization could result in more innovation driven by competition. On the other hand, it could lead to less efficient payments if the variety of systems are not compatible with one another, requiring consumers either to join multiple services or be left out — resulting in a lack of ubiquity in the new system.

Other countries have taken a centralized approach to driving faster payment innovation, with the government either building the new payment platform or mandating that the private sector develop one. The U.S. case is more complicated: There are multiple payment platforms in the country already and around 50 times more financial institutions than in some other developed countries. Additionally, the Fed is just one of several regulatory bodies with a stake in payments. So far, the Fed has tried to facilitate private action in the development of faster payments. Whether it will take a more active role would depend on the circumstances.

"We will be guided by current and potential market developments and challenges, as well as our long-established criteria for offering new products and services," then-Fed Gov., now Chairman, Jerome Powell said in an October 2017 speech![]() . "These criteria include the need to fully recover costs over the long term; the expectation that the new service will yield clear public benefit; and the expectation that other providers alone cannot be expected to provide the service with a reasonable effectiveness, scope, and equity."

. "These criteria include the need to fully recover costs over the long term; the expectation that the new service will yield clear public benefit; and the expectation that other providers alone cannot be expected to provide the service with a reasonable effectiveness, scope, and equity."

More Than Speed

In some ways, U.S. payments are already starting to speed up. The Clearing House, which is owned by the largest U.S. commercial banks, has begun rolling out a faster payments solution similar to the U.K. Faster Payments Service called Real-time Payments, or RTP. RTP makes funds available instantaneously while settling transactions on a deferred net basis multiple times per day. The payment platform had its first successful test in November 2017, and the Clearing House has said it hopes to make the service available to most of the country by 2020.

Speed isn't the only benefit to rethinking payments. New platforms can take advantage of more advanced security features as well. Noncash payment systems have historically been limited largely to debit or "pull" transactions, where the payee's institution requests funds from the payer, as opposed to credit "push" transactions, where the payer requests that funds be sent. This was due to the fact that initiating a noncash payment requires a computer, and in the past recipients tended to be larger organizations that were more likely to have computers than individuals.

Today, anyone with a smartphone has a computer in his or her pocket. Credit push transactions may be less susceptible to fraud since the payer is the one who must initiate and authorize payment. The Clearing House's RTP offers push transactions as do many other faster payment platforms in other countries. A separate Secure Payments Task Force![]() helped the Faster Payments Task Force identify payment security goals and is working to develop proposals for achieving those goals.

helped the Faster Payments Task Force identify payment security goals and is working to develop proposals for achieving those goals.

The fundamental goal of any new payment system, however, is that it works — easily and reliably.

"While payments do provide economic value, they're not what households and firms value the most," says Scott Schuh, former director of the Boston Fed's Consumer Payments Research Center. "What they value most are the goods and services that they're buying. An ideal payment system provides the least costly way of making exchanges happen."

Readings

"Fast Payments — Enhancing the Speed and Availability of Retail Payments.![]() " Bank for International Settlements Committee on Payments and Market Infrastructures, November 2016.

" Bank for International Settlements Committee on Payments and Market Infrastructures, November 2016.

Greene, Claire, Marc Rysman, Scott Schuh, and Oz Shy. "Costs and Benefits of Building Faster Payment Systems: The U.K. Experience and Implications for the United States.![]() " Federal Reserve Bank of Boston Current Policy Perspectives No. 14-5, February 2015.

" Federal Reserve Bank of Boston Current Policy Perspectives No. 14-5, February 2015.

Rosenbaum, Aaron, Garth Baughman, Mark Manuszak, Kylie Stewart, Fumiko Hayashi, and Joanna Stavins. "Faster Payments: Market Structure and Policy Considerations.![]() " Federal Reserve Board Finance and Economics Discussion Series No. 2017-100, September 2017.

" Federal Reserve Board Finance and Economics Discussion Series No. 2017-100, September 2017.

"The U.S. Path to Faster Payments." Faster Payments Task Force Final Report Parts One![]() and Two

and Two![]() , January and July 2017.

, January and July 2017.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us