The Coronavirus Crisis and Debt Relief

Loan forbearance and other debt relief have been part of the effort to help struggling households and businesses

Econ Focus

Second/Third Quarter 2020

The pandemic's harmful financial effects have been distributed unevenly — so much so that the headline macroeconomic numbers generally have not captured the experiences of those who have been hardest hit financially. Between February and April, for example, the U.S. personal savings rate actually increased by 25 percentage points. This macro statistic reflected the reality that the majority of U.S. workers remained employed, received tax rebates, and reduced their consumption. But the savings data did not reflect the experiences of many newly unemployed service sector workers.

And there are additional puzzles in the data. The U.S. economy is now in the midst of the worst economic downturn since World War II, yet the headline stock market indexes — such as the Dow Jones Industrial Average and the S&P 500 — are near record highs, and housing prices have generally remained firm. How can this be? Many observers agree that the Fed's expansionary monetary policy is playing a substantial role in supporting asset prices, but another part of the explanation may be that the pandemic's economic damage has been concentrated among firms that are too small to be included in the headline stock indexes and among low-wage workers, who are not a major factor in the U.S. housing market.

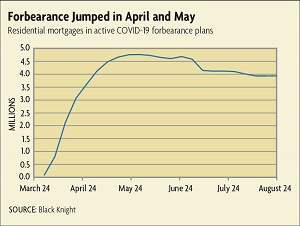

Policymakers have taken aggressive steps to mitigate the pandemic's financial fallout. Among the most prominent have been IRS tax rebates, the expansion of unemployment insurance benefits, and forgivable Payroll Protection Plan (PPP) loans for businesses. But these fiscal steps have been complemented by an array of policies specifically designed to ease private sector debt burdens. The CARES Act, for instance, mandated debt forbearance on federally backed mortgages and student loans. And the Fed — in addition to launching several new lending facilities — has coordinated with other federal bank regulators to encourage banks to work constructively with their clients in need of loan restructurings. (See "The Fed's Emergency Lending Evolves.") While less well-publicized than the fiscal steps, these debt relief measures are arguably no less consequential.

A Role for Debt Relief

The economic policies that have been adopted in response to the crisis were designed to meet multiple goals. The most immediate concerns were to provide safety net aid to those in need and to stimulate aggregate demand. But there was also a longer-term objective: to improve the foundation for future growth by helping households and firms maintain their financial health. This goal is being addressed partly by fiscal transfers to households and firms to help them avoid depleting their assets and increasing their debts. But crucially, the goal is also being advanced by policies designed to keep the supply of bank credit flowing and to prevent unnecessary loan defaults and business failures.

The CARES Act contains several important debt relief provisions. In addition to allowing for the deferment of student loan debt repayments and providing debt service forbearance and foreclosure protection for borrowers with federally backed mortgages, the legislation also mandated the relaxation of certain accounting standards — making it more attractive for banks to offer debt forbearance to households and firms affected by the pandemic. In support of the legislation's intent, federal bank regulators at the Fed and other agencies issued an interagency statement on March 22 confirming that financial institutions could make pandemic-related loan modifications without having to downgrade the loans to the category of Troubled Debt Restructurings (or TDRs). Since it is costly for banks to recategorize loans as TDRs, this interpretation helped to remove an impediment to loan restructurings.

Bank regulators followed this up by issuing a statement in June that outlined supervisory principles for assessing the safety and soundness of financial institutions during the pandemic. According to the statement, regulators "have encouraged institutions to use their capital buffers to promote lending activities." Moreover, the regulators emphasized that they "view loan modification programs as positive actions that can mitigate adverse effects on borrowers due to the pandemic." They sought to assure bankers that bank examiners "will not criticize institutions for working with borrowers as part of a risk mitigation strategy intended to improve existing loans, even if the restructured loans have or develop weaknesses that ultimately result in adverse credit classification."

This guidance has been implemented by the Fed's regional bank supervisors, including those in the Fifth District. "We want the banks to be part of the solution and to continue to lend," says Lisa White, executive vice president of the Supervision, Regulation, and Credit department at the Richmond Fed. "Overall, the banks were more resilient from a capital perspective heading into the current crisis compared to the last," she says. "The philosophy behind the interagency guidance was to convey our planned supervisory approach and clearly communicate what we will be most focused on as we assess how banks are handling the challenges associated with the pandemic."

When supervisors evaluate how well banks have performed during the crisis, she explains, "we are going to assess how well they have managed their deferral and forbearance programs, and we will put more emphasis — even more than we've had in the past — on their underwriting and risk management practices versus just the results or how they translate into a particular loan's performance."

Our Related Research

Loan Forbearance and Households

Prior to the pandemic, the household sector's credit metrics appeared to be in good shape. In 2019, the overall delinquency rate for consumer credit stood at a post-financial-crisis low of roughly 5 percent, as declining mortgage delinquencies in recent years had roughly offset increased auto loan and credit card delinquencies. Moreover, the aggregate data showed no noticeable upward trend in personal foreclosures and bankruptcies. These signs of health may have partly reflected the conservative underwriting practices that creditors had adopted after the 2007-2008 financial crisis, when they shifted toward making loans to borrowers with higher credit scores.

But these numbers may not adequately reflect the financial vulnerability of many low-income households. According to the research and consulting firm Financial Health Network, as many as 33.9 percent of those surveyed in 2019 stated that they were "unable to pay all bills on time." The same survey found that, among those who make less than $30,000, only 34.7 percent stated that they have a "manageable amount of debt." These numbers are consistent with the notion that there is a significant part of the U.S. population that lives paycheck to paycheck and is quite vulnerable to interruptions in income.

These vulnerable low-income households bore the brunt of the economy's job losses at the onset of the pandemic. Based on an analysis of ADP data presented at a recent Brookings Papers on Economic Activity conference, employment losses were disproportionately high among the quintile of employees with the lowest pre-pandemic wages. That quintile had a greater than 35 percent decline in employment by April, which contrasts sharply with the less than 10 percent decline in employment for those in the highest-wage quintile.

Readings

Brunnermeier, Markus, and Arvind Krishnamurthy. "Corporate Debt Overhang and Credit Policy." Brookings Papers on Economic Activity, Summer 2020.

Gordon, Grey, and John Bailey Jones. "Loan Delinquency Projections for COVID-19." Federal Reserve Bank of Richmond Working Paper No. 20-02, April 15, 2020.

Hudson, Michael. …and forgive them their debts: Lending, Foreclosure and Redemption From Bronze Age Finance to the Jubilee Year. Dresden: ISLET-Verlag, 2018.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us