How Did Short-Term Market Rates React to Liftoff?

Economic Brief

September 2016, No. 16-09

The implementation of monetary policy has changed significantly since 2008. In particular, very large excess reserves in the financial system have led to the creation of new tools to manage the federal funds rate. Given these changes, some observers have wondered how money market interest rates would respond to "liftoff," the Fed's first interest rate increase from effectively zero. Since liftoff in December 2015, it appears that the Fed's influence over short-term interest rates remains intact.

On December 16, 2015, the Federal Open Market Committee (FOMC) raised the target federal funds rate for the first time in nearly 10 years after keeping it at effectively zero for seven years.

A notable facet of this event was that the Fed raised rates despite having a very large balance sheet with substantial excess reserves in the financial system, a result of actions taken in response to the 2008 financial crisis and the Great Recession. Some observers have since questioned how markets would react to liftoff in such a scenario — that is, whether the Fed exerts the same degree of "control" over short-term market interest rates as it did when reserves were more scarce.

This Economic Brief will explore how liftoff would have been expected to affect markets in the old world, why some have wondered whether the Fed's influence over market rates would have changed in the new world, and how markets did, in fact, respond to liftoff.

The Fed's Influence over Market Interest Rates

In general terms, the Fed conducts monetary policy by attempting to make the market-based rates influenced by its policy settings track the economy's underlying "natural" rate of interest.1 Operationally, the Fed does this by directly influencing selected short-term rates within the financial system, which in turn influences rates paid by a wide variety of public and private parties in the broader market.

The Fed influences market rates at all ends of the maturity spectrum. Longer-term rates are what drive much economic activity — especially investment decisions and the financing of major consumer purchases such as houses and automobiles. The Fed's influence over long-term rates is limited in the short run, however. Long-term rates are a function of both the path of short-term rates and a "term premium," the nature and determinants of which are subjects of much debate.2

An episode that well demonstrated the Fed's limited control over long-term rates occurred after the Fed raised the target federal funds rate (the rate banks pay to borrow money from one another overnight) in 2004, from historically low levels, for the first time in four years. During a series of rate hikes into the following year, the ten-year Treasury yield failed to rise much. In February 2005, after dismissing several common hypotheses to explain the behavior, then-Chairman Alan Greenspan famously referred to the failed correlation as a "conundrum."

More recently, certain monetary policy initiatives — quantitative easing, Operation Twist, and forward guidance — took steps specifically to influence long-term rates. The first two, in particular, attempted to do so through very large purchases of longer-term assets. Researchers have debated how much of an effect these programs had on longer-term interest rates, as well as to what extent the effect they did have was due to the purchases themselves versus the signaling effect about the likely path of future short-term interest rates.3 Nonetheless, as a usual course of policy implementation, longer-term rates wouldn't necessarily be expected to move in lockstep with the Fed's policy rates.

Stronger Influence over Short-Term Rates

A better gauge of the degree of the Fed's influence over market rates is provided by looking at shorter-term rates. There has been some discussion about whether the Fed's degree of influence over market rates would be different in the new world of large excess reserves.

For example, some observers have argued that the Fed's large balance sheet - which ballooned from less than $1 trillion in late 2008 to roughly $4.5 trillion today — should make it inherently difficult for the Fed to control short-term rates. This notion may stem from how monetary policy has historically been conducted. In the past, the Fed set a target for the fed funds rate and achieved that rate by influencing the supply of reserves in the banking system in line with estimates of the demand for reserves. (Moreover, because the Fed had built up credibility for achieving its target rate, trading often would occur at a rate near or equal to the target fed funds rate with only small open market operations by the Fed.) Under this system, reserves were relatively scarce, and there was a low level of excess reserves in the banking system.

Monetary policy implementation has changed, however. The Fed's response to the financial crisis and Great Recession entailed large asset purchases and thus a large expansion of the Fed's balance sheet and reserves in the banking system. The Fed received authority in October 2008 to pay banks interest on their reserve balances, which provided a tool — known as IOR, or interest on reserves — for inducing banks to maintain high levels of excess reserves. Otherwise the expansion of the Fed's balance sheet — and the corresponding increase in the supply of reserves — would hinder the Fed's ability to achieve its fed funds target. In other words, IOR provides a tool for the Fed to influence short-term market rates even with a very large balance sheet and a large quantity of excess reserves. In principle, IOR ought to do so by setting a floor on the fed funds rate.

Other observers have wondered what effect liftoff would have on short-term market rates because IOR initially failed to create the floor on the fed funds rate that it was intended to provide. One major reason is that some institutions — including the government-sponsored enterprises and some international institutions — hold reserves with the Fed but are not eligible to receive IOR. As such, these institutions would not be content to hold large excess reserves. They also tend to be net sellers in the fed funds market and may have been willing to lend in the fed funds market below the IOR rate, putting downward pressure on the fed funds rate. Banks, in turn, would be able to earn risk-free profit by borrowing at the fed funds rate and holding the borrowed funds as reserves, earning IOR. A 2011 paper by Morten L. Bech of the New York Fed and Elizabeth Klee of the Fed's Board of Governors explores such an environment of large excess reserves in which some parties are eligible for IOR and some are not.4 Their model shows how this could contribute to the effective fed funds rate falling below the IOR rate, even though raising IOR still could exert upward pressure on market rates.

When the Fed eventually decided to raise rates, there was good reason to believe that raising IOR alone would pull up short-term market rates, with a modest spread between IOR and the fed funds rate persisting. However, as an insurance policy, the Fed created an alternative investment opportunity, an overnight reverse repurchase, or repo, agreement facility (known as ON RRP) for money markets. In principle, ON RRP would complement IOR and influence money markets without requiring reserve draining. A reverse repo is a transaction in which a security is sold with the simultaneous agreement to reverse the sale at a specified price and set future date. In ON RRP, the interest rate paid by the Fed on the reverse repo is determined by the difference between the two sales' prices and the duration of the contract. As described by Simon Potter, head of the New York Fed's open market desk, in an early 2016 speech, instead of altering reserve levels directly, this facility focused on influencing market rates by intensifying competition in money markets.5 As Potter stated, "Instead of running quantity-based, term operations aimed at altering reserve levels, the Desk would run interest-rate-based overnight operations aimed directly at influencing market rates."

Even with the combination of IOR and the ON RRP facility, it was possible that liftoff would not work exactly as planned — that is, that the fed funds rate and other money market rates might not rise in lockstep with IOR. As a result, Potter noted, while the pre-liftoff testing suggested that the tools were likely to work well, it wasn't possible to determine with certainty the extent to which market rates were driven by the tools versus features of the financial system near the zero lower bound on nominal interest rates that may have helped keep the target fed funds rate within range.

How Markets Responded to Liftoff

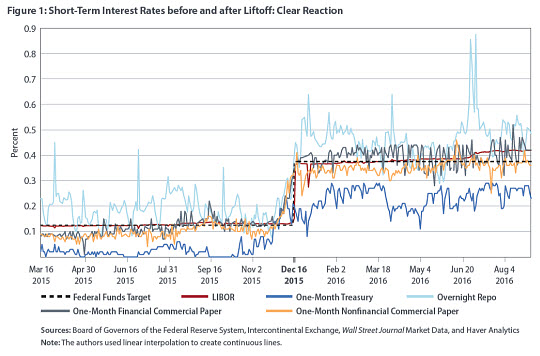

The FOMC raised its target fed funds rate at its December 16, 2015, meeting. Money market rates moved much as one would expect: they rose essentially in lockstep with liftoff. (See Figure 1 below.)

One can see short-term rates rising in the weeks before liftoff, reflecting the market's increasing expectation that liftoff would indeed happen at the December 2015 meeting. The means of short-term rates rose proportionally after liftoff: by 28 basis points for one-month financial commercial paper, 25 basis points for one-month nonfinancial commercial paper, 26 basis points for LIBOR, 28 basis points for overnight repos, and 20 basis points for one-month treasuries.6 (There are reasons to expect that Treasury bills will not rise to the same degree as other rates in a way that does not suggest the Fed has less influence over money market rates.7) The standard deviations increased only slightly.

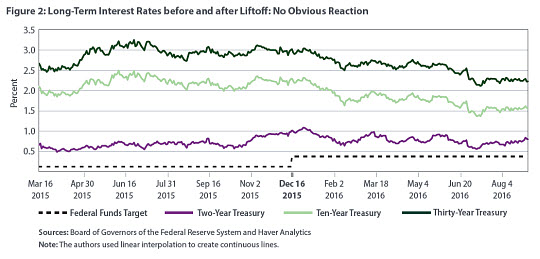

After liftoff, longer-term Treasury rates fell. (See Figure 2 below.) This can be explained partly by an increased demand for long-term treasuries that may have resulted from, among other factors, soft global growth and regulatory changes that increased interest from banks and money market mutual funds. As noted above, the reaction of long-term interest rates does not necessarily suggest the Fed's influence over markets is lacking or different in the new world given the volatile term premium that is a major determinant of longer-term interest rates.

The market's response to liftoff matters because if the Fed cannot change short-term market interest rates, then monetary policy is essentially powerless. The market's response also matters because if the Fed can change the average level of market rates, but there is high and unpredictable volatility on spreads between the IOR rate and other short-term rates, then it is possible that the Fed would have a communication problem and that its credibility would suffer. The market could interpret unintended deviations of the effective rate from the target rate as a change in the stance of policy. In the recent past, for example, the media has suspected the Fed of "stealth" monetary policy when the effective rate differed from the target rate.8

However, despite some concern that the Fed's fundamental relationship with markets has changed in a world with large excess reserves and IOR, key shortterm rates have thus far responded tightly to liftoff, with comparable increases in mean interest rates and no major change in standard deviations.

Renee Haltom is editorial content manager and Alexander L. Wolman is vice president for monetary and macroeconomic research in the Research Department at the Federal Reserve Bank of Richmond.

1

For more on the natural rate of interest and its use in monetary policy, see Thomas A. Lubik and Christian Matthes, "Calculating the Natural Rate of Interest: A Comparison of Two Alternative Approaches," Federal Reserve Bank of Richmond Economic Brief No. 15-10, October 2015.

2

For a recent, nontechnical overview, see Ben S. Bernanke, "Why Are Interest Rates So Low, Part 4: Term Premiums," Brookings blog post on April 13, 2015.

3

See Michael Woodford, "Methods of Policy Accommodation at the Interest-Rate Lower Bound," Paper presented at the Federal Reserve Bank of Kansas City's Economic Policy Symposium in Jackson Hole, Wyo., August 30, 2012.

4

See Morten L. Bech and Elizabeth Klee, "The Mechanics of a Graceful Exit: Interest on Reserves and Segmentation in the Federal Funds Market," Journal of Monetary Economics, July 2011, vol. 58, no. 5, pp. 415-431. A previous version is available online.

5

See Simon Potter, "Money Markets after Liftoff: Assessment to Date and the Road Ahead," Remarks at the 70th Anniversary Celebration of the School of International and Public Affairs at Columbia University, New York, N.Y., February 22, 2016.

6

The comparison periods for the means were nine months before liftoff and nearly nine months after liftoff, that is, through August 31, 2016. Omitting the month of observations immediately prior to liftoff in order to account for expectations of liftoff did not meaningfully change these means.

7

See Potter (2016).

8

See Huberto M. Ennis and Todd Keister, "Understanding Monetary Policy Implementation," Federal Reserve Bank of Richmond Economic Quarterly, Summer 2008, vol. 94, no. 3, pp. 235-263.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us