Are the Effects of Fiscal Policy Asymmetric?

Economic Brief

September 2017, No. 17-09

Economic research on the size of the fiscal multiplier has assumed that the effects of changes in government spending are symmetric — that is, they influence economic output to the same degree whether the change is an increase or a decrease. Richmond Fed research indicates that this is not the case; the fiscal multiplier does vary according to the direction of the fiscal action and also varies with the stage of the economic cycle. This finding sheds light on likely outcomes of fiscal policies and helps account for inconsistent estimates of the multiplier in the literature.

Following the economic crisis of 2008-09, the use of fiscal stimulus in the United States and other industrialized countries led to a resurgence of interest in the size of the "multiplier" — roughly speaking, the effect on total economic output of a one-dollar increase or decrease in government spending or taxation. Interest in this question was further motivated in the 2010s by contractionary fiscal policies in continental Europe, which were implemented in response to rising levels of public debt. Estimates of the size of the multiplier have been inconsistent, with results in recent research ranging from 0.5 to 2.0. With some justice, the effect of fiscal stimulus or contraction on output has been termed "the foremost academic and policy dispute of the day."1

Economic research on this question has assumed that the effects of fiscal policy shocks are symmetric; that is, a dollar of fiscal stimulus has been assumed to have the same multiplier as a dollar of fiscal contraction. Yet in the context of monetary policy, economists have long theorized that the effects of monetary stimulus and contraction are asymmetric, with monetary contraction having a larger effect on output — a view to which recent empirical research has lent support.2 Might the same be true of fiscal policy?

Two of the authors of this brief, Barnichon and Matthes, have used a new statistical methodology to investigate whether the size of the multiplier varies on the basis of whether the fiscal shock is positive or negative. Their methodology also enables them to assess whether the multiplier is different during a recessionary stage of the business cycle or a nonrecessionary stage. The findings of this research offer a path for reconciling the inconsistent results of earlier research and provide support for the hypothesis of an asymmetric multiplier.3

Detecting Asymmetry in the Fiscal Multiplier

The research by Barnichon and Matthes employs a statistical methodology that they term "functional approximation of impulse responses," or FAIR. This approach facilitates the incorporation of nonlinearity into models, including the testing of multiple nonlinearities jointly — such as allowing for estimates to depend on whether the sign of a fiscal shock is positive or negative and at the same time allowing for estimates to depend on whether the shock takes place within an expansion or recession.4

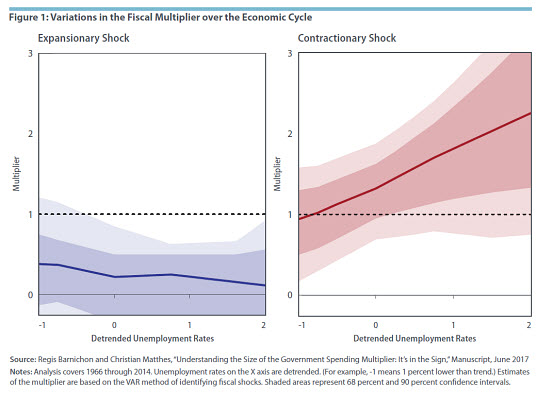

The authors assume that the fiscal policy shock is structured as a temporary, possibly deficit-financed change in government purchases. They estimate the multiplier using two of the principal approaches in the literature to identifying fiscal shocks — the Auerbach and Gorodnichenko vector autoregression (VAR) approach and Ramey's narrative approach.5 Under both approaches, they find that the multiplier for contractionary shocks to government spending, which they term m−, is greater than 1.0 throughout the business cycle and that it is at its peak during recessions. With regard to expansionary fiscal shocks, the ones most often associated with fiscal policy, they find that the multiplier m+ is around 0.5 and is not statistically different in recessions than in nonrecessionary periods. (See Figure 1 below.)

1

Òscar Jordà and Alan M. Taylor, "The Time for Austerity: Estimating the Average Treatment Effect of Fiscal Policy," Economic Journal, February 2016, vol. 126, no. 590, pp. 219–255 (article available with subscription).

2

See Regis Barnichon, Christian Matthes, and Tim Sablik, "Are the Effects of Monetary Policy Asymmetric?" Federal Reserve Bank of Richmond Economic Brief No. 17-03, March 2017; also, see Regis Barnichon and Christian Matthes, "Gaussian Mixture Approximations of Impulse Responses and the Nonlinear Effects of Monetary Shocks,” Federal Reserve Bank of Richmond Working Paper No. 16-08, July 2016.

3

Regis Barnichon and Christian Matthes, "Understanding the Size of the Government Spending Multiplier: It's in the Sign," Manuscript, June 2017.

4

The FAIR method is also employed in Barnichon and Matthes (2016).

5

Economists have used various methods to isolate unexpected changes in government spending — fiscal shocks — from expected ones. In a 2011 article, Valerie A. Ramey of the University of California, San Diego observed that much previous work had erroneously treated as "fiscal shocks" some spending changes that actually could have been forecasted by market participants using standard macroeconomic variables. Ramey thus introduced a narrative approach, one based on analysis of news texts, to capture changes in expectations about military spending. (Shocks identified in this way are sometimes called "Ramey news shocks.") Valerie A. Ramey, "Identifying Government Spending Shocks: It's All in the Timing," Quarterly Journal of Economics, February 2011, vol. 126, no. 1, pp. 1–50 (article available with subscription). In contrast, a 2012 article by Alan J. Auerbach and Yuriy Gorodnichenko of the University of California, Berkeley dealt with the issue of expected versus unexpected government spending changes by using a collection of professional forecasts of macroeconomic variables to attempt to isolate the unexpected component of spending from the expected component. Alan J. Auerbach and Yuriy Gorodnichenko, "Measuring the Output Responses to Fiscal Policy," American Economic Journal: Economic Policy, May 2012, vol. 4, no. 2, pp. 1–27.

6

Valerie A. Ramey and Sarah Zubairy, "Government Spending Multipliers in Good Times and in Bad: Evidence from U.S. Historical Data," National Bureau of Economic Research Working Paper No. 20719, November 2014 (article available with subscription).

7

Auerbach and Gorodnichenko (2012)

8

For further detail on these and related mechanisms, see Barnichon, Matthes, and Sablik (2017) and Barnichon and Matthes (2016).

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.