Are the Effects of Monetary Policy Asymmetric?

Economic Brief

March 2017, No. 17-03

The Federal Reserve uses monetary policy to stimulate the economy when unemployment is high and to rein in inflationary pressures when the economy is overheating. However, evidence suggests that these policy stances have unequal effects. Contractionary monetary shocks raise unemployment more strongly than expansionary shocks lower it.

The Federal Reserve has a "dual mandate" to maintain stable prices and maximum sustainable employment. It does so primarily by controlling its target interest rate (the federal funds rate), which influences short-term market rates. When unemployment is elevated, the Fed loosens monetary policy (lowers its target rate) to stimulate economic activity and boost output. When inflation is rising, the Fed tightens policy (raises its target rate) to slow economic activity and counteract inflationary pressure.

But are both types of policy responses equally effective? Since the Great Depression, economists have suspected that tight policy may have a stronger effect on output than loose policy because the Fed's response to the market crash of 1929 failed to avert the Great Depression. Milton Friedman and Anna Schwartz later argued in their 1963 book, A Monetary History of the United States, that this was because the Fed's policy stance during the early 1930s actually was contractionary rather than expansionary, but other examples have reinforced the view that expansionary monetary policy may be more limited than contractionary policy. Most recently, the Fed was forced to turn to unconventional policies during the Great Recession after reducing its target rate to nearly zero seemed to have little effect on unemployment.

Monetary policy asymmetry is best described using a metaphor. Imagine a string with monetary policy at one end and the economy at the other. Employing tight monetary policy when inflation is rising is like pulling on the string to keep the economy in check — it works fairly well. But attempting to stimulate the economy with loose policy during a downturn is like trying to push on the string to move the economy — not very effective.

In addition to monetary changes having asymmetric effects based on their direction, the strength of monetary policy may also vary with the state of the economy. Previous tests for monetary policy asymmetries have had somewhat mixed results, but this Economic Brief presents new evidence to confirm the asymmetric effects of monetary policy.

Why Might Monetary Policy Be Asymmetric?

There are several theoretical reasons why monetary policy could have asymmetric effects on economic output.1 The first relates to the behavior of lenders and borrowers under different monetary conditions. When the Fed raises its policy rates, market rates tend to rise accordingly. One might expect that banks would simply pass these higher rates on to their borrowers. While this is true to an extent, raising loan rates too high could increase the likelihood that risky borrowers default. As a result, banks may choose to ration credit during a period of high interest rates, constraining credit for some consumers and leading to a bigger decline in output, thus amplifying the impact of contractionary monetary policy. On the other hand, expansionary policy will not necessarily increase borrowing and spending if economic conditions have reduced demand. Unlike tight monetary policy, it is not a binding constraint on consumers (as expressed in the old adage, you can lead a horse to water but you can't make it drink).

Another reason why expansionary monetary policy might be less effective than contractionary policy is because prices seem less likely to adjust downward — that is, they are "sticky." Firms also may be reluctant to lower wages for fear of damaging worker morale. Because of such downward price and wage rigidity, firms will tend to respond to contractionary monetary policy by reducing output rather than prices. Prices and wages are less upwardly sticky, however. Firms are accustomed to raising prices and wages gradually due to inflation, for example. As a result, expansionary monetary policy is more likely to prompt a change in prices rather than output.

Finally, monetary policy may have asymmetric effects during different points in the business cycle due to changes in consumer outlook. Similar to the credit-constraint argument, if consumers are pessimistic about economic conditions, then lowering rates may not do much to stimulate borrowing and spending. This explanation is not entirely compelling, however, since consumer optimism during a boom period should also weaken the effect of tight monetary policy. For contractionary policy to have a stronger effect than expansionary policy, consumers and firms would have to be more pessimistic during economic downturns than they are optimistic during booms. This is certainly possible but perhaps not realistic.

Testing for Asymmetry

If monetary policy does have asymmetric effects on output, that finding would have important implications for how the Fed conducts policy. Conclusive evidence one way or the other has proven somewhat elusive, however. A number of studies do find evidence that contractionary policy has a stronger effect on output than expansionary policy, as the theory predicts.2 But other studies find that what matters is not the direction of the monetary change but rather its size.3 And still other studies find evidence that the impact of monetary policy depends chiefly on the state of the economy.4

One problem facing economists trying to find evidence of asymmetry is that the standard models used for measuring the effects of shocks, such as changes in monetary policy, have difficulty identifying asymmetric effects. Economists have attempted to get around this problem in two ways. The first involves looking at unanticipated increases and decreases in the money supply and testing whether these changes have asymmetric effects. One challenge with this approach is correctly identifying unanticipated monetary shocks. Additionally, while these models may be able to detect asymmetry based on the direction of a monetary change, they struggle to measure other potential causes of asymmetry. Another approach makes use of regime-switching models that allow for the impact of one variable (monetary policy) to depend upon changes in another variable (the state of the economy). But while these models can identify whether the effects of monetary policy change with the business cycle, they are not able to determine if the effects of contractionary policy are inherently different from those of expansionary policy.

Two of the authors of this brief, Barnichon and Matthes, have developed an alternative approach for addressing these issues.5 They start with a model of the economy in which the behavior of a system of macroeconomic variables is determined by its (possibly asymmetric) response to past and present shocks. They then use Gaussian functions to parameterize the dynamic effects of structural shocks on the economy. The advantage of this approach — dubbed Gaussian Mixture Approximation — is that it uses only a small set of free parameters, which then allows for a much more efficient estimation of models with asymmetric responses. In simulations, Barnichon and Matthes' approach not only performs as well as benchmark models in estimating linear or symmetric responses, it can also detect asymmetric responses in nonlinear models. Barnichon and Matthes use their new methodology to estimate whether monetary shocks generate asymmetric responses depending on the direction of the shock as well as the state of the economy.

Results and Implications

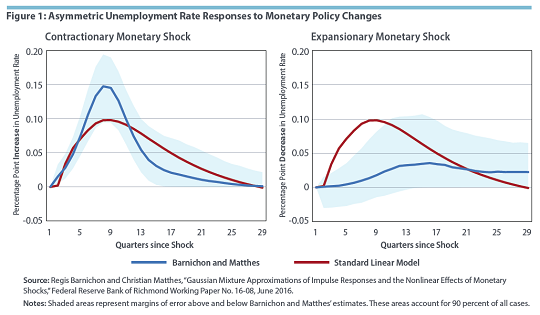

Barnichon and Matthes first test whether the direction of a monetary shock alone results in different economic responses. Applying data from 1959 through 2007 to their model, they find strong evidence of an asymmetric response in unemployment depending on the direction of the monetary change. They estimate that an increase in the federal funds rate of 0.7 percentage points results in an increase in unemployment of 0.15 percentage points, a larger effect than the 0.10 percentage points estimated by a standard linear model.6 (See Figure 1.) On the other hand, a 0.7 percentage point decrease in the federal funds rate produces only a 0.04 percentage point decrease in unemployment — an effect that is not statistically different from zero. This implies that contractionary monetary policy has a significantly stronger effect on unemployment than expansionary policy.

Barnichon and Matthes also find some, albeit inconclusive, evidence that prices respond asymmetrically to monetary changes. Prices appear stickier following monetary contractions than following monetary expansions. This provides some supporting evidence for the theory that monetary policy has asymmetric effects because firms are more reluctant to lower prices and wages than to raise them.

Next, Barnichon and Matthes expand their model to allow the effects of monetary policy to depend on both the direction of the change and the state of the economy. Again, they find that expansionary monetary policy has a weaker effect on unemployment than contractionary policy. Additionally, they find that the effect of expansionary policy depends on the state of the economy. When unemployment is low, expansionary policy generates a substantial increase in inflation but little change in unemployment. When unemployment is high, expansionary monetary policy has little effect on inflation and some positive effect on employment. This is consistent with standard macroeconomic theory and the Fed's experience during the Great Inflation.

The findings from Barnichon and Matthes' model have a number of implications for monetary policymakers. They suggest that monetary policy asymmetries may be larger than previous estimates have found. The Fed's ability to stimulate the economy through expansionary policy appears less potent than the negative effect contractionary policy has on employment. Additionally, as theory and other studies have suggested, attempting to use monetary policy to stimulate the economy beyond full employment is likely to only increase inflation with no significant reduction in unemployment.

Regis Barnichon is a research advisor at the Federal Reserve Bank of San Francisco. Christian Matthes is a senior economist and Tim Sablik is an economics writer in the Research Department at the Federal Reserve Bank of Richmond.

1

Donald P. Morgan, "Asymmetric Effects of Monetary Policy," Federal Reserve Bank of Kansas City Economic Review, Second Quarter 1993, vol. 78, no. 2, pp. 22–33.

2

For example, see James Peery Cover, "Asymmetric Effects of Positive and Negative Money-Supply Shocks," Quarterly Journal of Economics, November 1992, vol. 107, no. 4, pp. 1261–1282; and Emiliano Santoro, Ivan Petrella, Damjan Pfajfar, and Edoardo Gaffeo, "Loss Aversion and the Asymmetric Transmission of Monetary Policy," Journal of Monetary Economics, November 2014, vol. 68, pp. 19-36. A working paper version is available online.

3

For example, Morten O. Ravn and Martin Sola, "A Reconsideration of the Empirical Evidence on the Asymmetric Effects of Money-Supply Shocks: Positive vs. Negative or Big vs. Small?" Birkbeck, University of London, Archive Discussion Paper No. 9606, February 1996.

4

For example, see Silvana Tenreyro and Gregory Thwaites, "Pushing on a String: US Monetary Policy Is Less Powerful in Recessions," American Economic Journal: Macroeconomics, October 2016, vol. 8, no. 4, pp. 43–74. A working paper version is available online. Also, see Ming Chien Lo and Jeremy Piger, "Is the Response of Output to Monetary Policy Asymmetric? Evidence from a Regime-Switching Coefficients Model," Journal of Money, Credit and Banking, October 2005, vol. 37, no. 5, pp. 865–886. A working paper version is available online. Also, see Charles L. Weise, "The Asymmetric Effects of Monetary Policy: A Nonlinear Vector Autoregression Approach," Journal of Money, Credit and Banking, February 1999, vol. 31, no. 1, pp. 85–108.

5

Regis Barnichon and Christian Matthes, "Gaussian Mixture Approximations of Impulse Responses and the Nonlinear Effects of Monetary Shocks," Federal Reserve Bank of Richmond Working Paper No. 16-08, June 2016.

6

In this context, "linear" implies symmetry.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of their respective Reserve Banks or the Federal Reserve System.