Should We Worry about Trade Imbalances?

Economic Brief

October 2017, No. 17-10

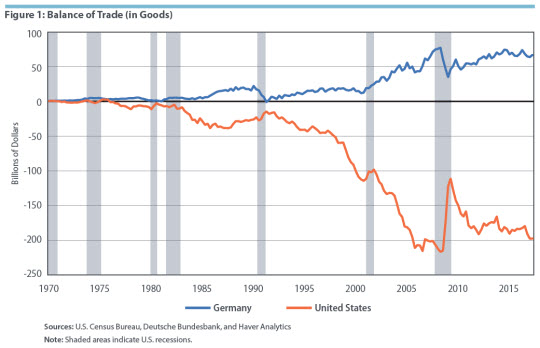

Trade imbalances are a perennial concern for policymakers and the public. But what does it mean for a country to have a trade surplus or deficit? The United States has run persistent trade deficits since the late 1970s, while Germany has had trade surpluses since the 1990s. Is either position inherently good or bad? The answer to this fundamental question of economic policy is a resounding "no" — up to a point.

Trade imbalances have been the focus of recent policy discussions in a number of countries. For example, the United States has run persistent trade deficits since the late 1970s, while Germany has had trade surpluses since the 1990s. (See Figure 1 below.) In order to understand how such imbalances might matter, or not, for economic policy, it is useful to consider a closely related concept: the current account.

The current account measures the value of a country's net exchange of goods and services with the rest of the world. It also includes any income earned on capital invested abroad and net transfers of cash to other countries (typically in the form of foreign aid). For most countries, the balance of trade makes up the lion's share of the current account, and the two tend to move in tandem.

Because a country's current account balance is largely determined by trade flows, one might assume that whether it is in surplus or in deficit largely depends upon other countries. In fact, the current account reflects domestic saving and investment decisions. To see why, consider the national income identity, an accounting concept that equates gross domestic product (GDP) to the sum of consumption, investment, government spending, and net exports. According to this identity, the net exports component equals domestic production minus consumption, government spending, and investment. National saving can be thought of as the difference between production and private and public consumption. Thus, the current account is roughly equal to the difference between saving and investment. From an accounting standpoint, then, a current account surplus simply means that a country's savings exceed its investments, and vice versa for a current account deficit. This relationship holds as an identity and at the same time provides insight into the current account's determinants.

But this accounting identity does not shed any light on whether current account deficits and surpluses are "good" or "bad" from the perspective of domestic or international economic policy. In order to determine that, one needs to consider the factors that drive domestic saving and investment over time. This Economic Brief will explore these factors through the examples of the United States, which has a current account deficit, and Germany, which has a current account surplus.

What Drives National Saving and Investment?

At the individual level, saving reflects a desire to put money aside for the future. National saving reflects the same desire on an aggregate level. A country can put national aggregate savings aside either domestically or abroad. If the country has a current account surplus, it is setting money aside abroad.

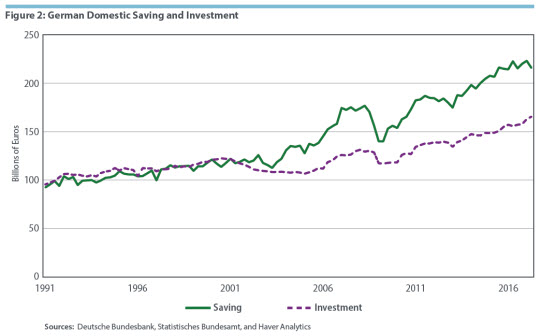

Other things being equal, a country with a current account surplus has extra savings that the domestic economy does not need or cannot absorb. This can be explained by a high private sector saving rate, by government budget surpluses, or by an underdeveloped domestic financial system. All of these elements are arguably the case for Germany (see Figure 2 below), whereas the opposite holds true for the United States. Current account surpluses and deficits therefore reflect these underlying factors and their potential imbalances. As far as policy is concerned, the current account is a symptom, not a cause.

Another way to see this is on the flip side of the current account, which is called the capital account. A country with a current account surplus exports goods and services to other countries and receives payment in their currency. Generally, the exporting country reinvests that currency either directly (building factories in the other country, for example) or indirectly by purchasing financial assets (stocks and bonds) from the other nation. These components, along with foreign cash reserves and asset holdings, make up the capital account. The current account and capital account comprise a country's balance of payments and must sum to zero. So a country with a current account surplus has a capital account deficit, since it is importing more foreign stocks and bonds than it is exporting. In this way, it is "exporting" its savings.1 These foreign savings can deliver returns in the future. At the level of a country, a current account surplus can therefore reflect a desire to prepare for the future.

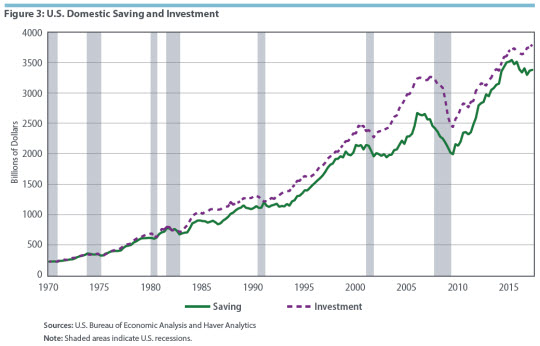

However, having a current account surplus or a capital account deficit does not necessarily mean a country has high savings. The second component of the current account is domestic investment. Other things being equal, a country tends to run a current account surplus if its domestic investment rate is low and a deficit if its domestic investment rate is high. The latter case can come about if a country has more investment opportunities than its domestic savers can finance. This imbalance also can be seen from the perspective of a country's capital account. Since the U.S. financial system is highly sophisticated, large, and liquid, it attracts more funds than it exports. Because the balance of payments must net to zero, the resulting capital account surplus has to be matched by a current account deficit. The attractiveness of the United States as an investment destination therefore helps drive its current account deficit. (See Figure 3 below.)2

Saving for the Future (the German Case)

A country with a current account surplus today can expect payments in the future from those surplus savings. In effect, the country is choosing to save today to spend more tomorrow. Why might it do this? A country's saving and spending decisions simply reflect the aggregate decisions of its residents. Individuals must decide how much to save and how much to consume over their lifetimes. In general, working individuals will save to preserve their standard of living in retirement (a pattern of behavior described by the life cycle hypothesis). And if they believe conditions in the future will be worse than the present, they will save even more today.

There are a number of factors that might lead a country's residents to be pessimistic about their economic futures. First, they may simply be extrapolating from a dismal past. In the 1990s and early 2000s, Germany was known as the "sick man of Europe." The fall of the Berlin Wall and the reunification of East Germany and West Germany imposed significant economic costs. From 1998 through 2005, Germany's annual economic growth averaged only 1.2 percent. To be sure, Germany has fared significantly better since that period. Labor market reforms in the mid-2000s and rising demand for German luxury goods and precision manufacturing (particularly from China) have helped turn the country into the economic powerhouse of Europe.3 But recent memories of less prosperous times still may be influencing Germans' expectations of the future. If they believe the good times are only transitory, they still may save more for the future than would otherwise be expected.

Other factors that can influence a country's outlook on future growth include trends in demographics and productivity. As is the case in many advanced countries, Germany's population is aging. According to the U.S. Census Bureau's international database, one in four Germans are projected to be over the age of sixty-five by 2025. Older populations work less, reducing a country's potential productivity and GDP growth. Indeed, concerns about slower productivity growth are widespread in the developed world. Some economists have argued that the productivity gains of the twentieth century will not be replicated in the twenty-first and that average growth will be much slower in the future.4 This, too, could be a reason for relative pessimism and higher savings.

Another factor that may influence a country's expectations for the future is its dependence on natural resources for economic growth. If residents expect to exhaust those resources in the near future, and there is no alternative source of growth, they might save for expected slower growth in the future. Norway is a good example. Its government uses proceeds from its oil reserves to finance a national pension fund to maintain consumption levels after its oil runs out.

All of these factors can help explain why countries run current account surpluses. But is a current account surplus necessarily a cause for concern? One could argue that a current account surplus might be a symptom of underinvestment in infrastructure necessary to promote future growth. So countries with high savings rates due to their relatively pessimistic outlooks of the future should do more to increase investment in infrastructure to boost future growth, even potentially to the point of temporary deficits.

Sunny Today, Sunnier Tomorrow (the U.S. Case)

If pessimism about the future can help explain why countries have current account surpluses, optimism about the future may help explain why countries have current account deficits. A deficit suggests a country has more investment opportunities than its domestic savers can fund. In this case, the country can borrow from other nations to finance investment. It also can borrow from other nations to finance consumption.

The factors that lead a country's populace to become more optimistic about the future are largely the reverse of the things that give rise to pessimism. If a country has historically enjoyed a dynamic, growing economy, its residents may reasonably expect this to continue in the future. Despite concerns from some observers that the United States has "run out of ideas," it is still home to many innovative firms such as Apple, Amazon, and Google. A current account deficit may in part reflect that American and foreign investors alike still believe that more innovations are on the horizon — self-driving cars, sustainable clean energy, and nanotechnology, to name a few — and that they are being driven by American firms.5

Relatively favorable demographics are another reason to be optimistic about the future. While the U.S. population is also graying, the trend is less pronounced than in some other developed nations. The Census Bureau predicts that slightly less than one in five Americans will be over the age of sixty-five in 2025. Another source of optimism is the presence of unexploited resources. In the American case, advances in horizontal drilling with hydrofracturing (or fracking) have unlocked new oil and natural gas reserves and have transformed the United States into an oil exporter. These new resources have translated into more jobs and higher wages for states with oil and natural gas reserves.6

More generally, as described previously, a country's current account deficit may be driven by its capital account surplus. For investors in many countries, U.S. Treasury bonds remain a safe investment in times of stress. If foreigners invest in more U.S. assets than Americans invest in foreign assets, the United States will run a capital account surplus. And by the accounting logic of the balance of payments, this imbalance means that the United States must run a current account deficit.

However, it should be noted that current account deficits not only originate in nations with high investment rates, but also can be driven by strong consumption (and conversely low savings rates). If an economy borrows from abroad to finance productive investment, then a current account deficit has a built-in expiration date in that the returns from higher production and productivity in the future result in future current account surpluses. But foreign borrowing to finance current consumption or a budget deficit lacks this feature. This scenario could become a cause for concern if creditors begin to doubt the borrowing nation's ability to repay debts.

What about Trade?

In the introduction of this Economic Brief, we noted that trade accounts for the largest component of the current account. But so far, we haven't talked about trade as a determinant of the current account. The reason is that while a country's exports and imports determine the composition of its current account, they do not determine the level. That, as argued above, is largely determined by domestic macroeconomic factors.

By and large, these domestic macroeconomic factors reflect a country's aggregate views about the future and are not inherently good or bad. However, there are a few extreme cases that could be concerning. A country that has a current account surplus due to low investment could arguably be doing more to invest in infrastructure and improve its future growth outlook. And a country that runs a current account deficit largely to finance consumption may face a painful financial correction in the future. Ultimately, however, these extreme cases do not change the fact that current account surpluses and deficits have little to do with trade deals and everything to do with domestic economic decisions.

Thomas A. Lubik is a senior advisor and Tim Sablik is an economics writer in the Research Department of the Federal Reserve Bank of Richmond.

1

In a sense, a country that has a capital account deficit provides funds, or capital, for the rest of the world. A country that has a capital account surplus provides investment opportunities for the rest of the world.

2

Incidentally, not all countries worry about current account deficits. For example, like the United States, Australia has run persistent current account deficits since the 1970s, but the Australian public and policymakers have never been particularly concerned about this imbalance.

3

Christian Dustmann, Bernd Fitzenberger, Uta Schönberg, and Alexandra Spitz-Oener, "From Sick Man of Europe to Economic Superstar: Germany's Resurgent Economy," Journal of Economic Perspectives, Winter 2014, vol. 28, no. 1, pp. 167–188.

4

For more on this discussion, see Aaron Steelman and John A. Weinberg, "A 'New Normal'? The Prospects for Long-Term Growth in the United States," Federal Reserve Bank of Richmond 2015 Annual Report, pp. 4–27.

5

Steelman and Weinberg (2015)

6

James Feyrer, Erin T. Mansur, and Bruce Sacerdote, "Geographic Dispersion of Economic Shocks: Evidence from the Fracking Revolution," American Economic Review, April 2017, vol. 107, no. 4, pp. 1313–1334 (article available with subscription).

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.